Matador Resources is expanding its gas processing capacity in the Delaware Basin to service third-party demand and the E&P’s own development plans as it integrates assets acquired earlier this year for $1.6 billion.

Dallas-based Matador Resources Co. plans to make investments this year to boost the flow assurance of the company’s natural gas production in the Delaware, Joseph Wm. Foran, Matador founder, chairman and CEO, said in second-quarter earnings released after markets closed on July 25.

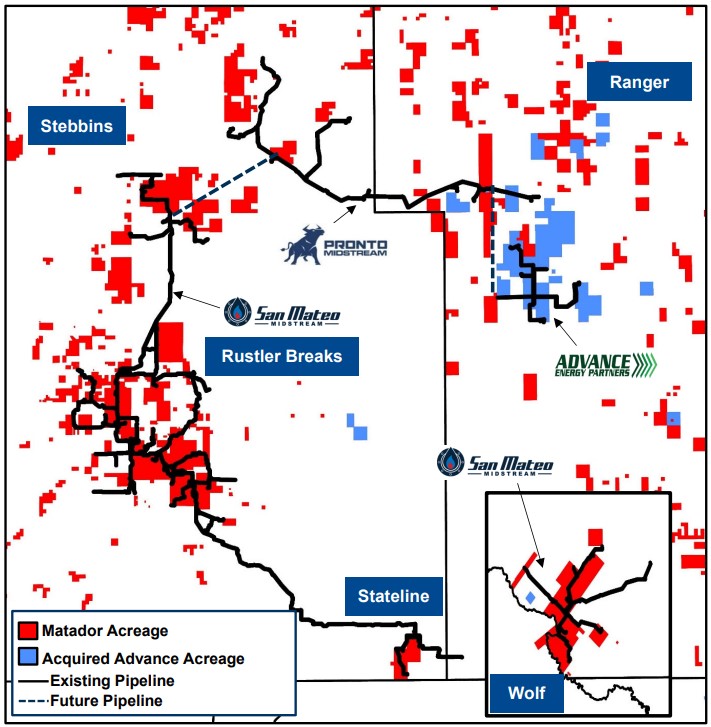

Matador acquired Delaware Basin midstream assets in a transaction with Summit Midstream Partners LP last summer.

RELATED

Summit Divests Williston Basin Gas Gathering System for $40 Million

The Summit assets—which were later rebranded as Pronto Midstream—included 45 miles of gas gathering pipelines in Lea and Eddy counties, New Mexico; a cryogenic gas processing plant with an inlet capacity of 60 MMcf/d; and three compressor stations, according to Securities and Exchange Commission filings.

The Pronto system assures additional flow capacity for Matador’s acreage in the northern Delaware Basin, Foran said. The assets also deliver flow capacity for the incremental production Matador scooped up through its acquisition of Advance Energy Partners earlier this year.

Matador has connected more than 15 of its wells in Lea County to the Pronto system to date, and the E&P expects to connect the Advance assets into the system later this year or in early 2024.

But due to the company’s outlook for developing the new Advance acreage, as well as third-party demand for gas gathering and processing in the Delaware Basin, Matador plans to expand Pronto’s processing capacity.

Matador is looking to add a larger cryogenic gas processing plant with an inlet capacity of 200 MMcf/d to the Pronto system.

“We are currently evaluating whether to include a partner in building the processing plant,” Foran said.

Matador also owns operational control of the San Mateo midstream assets in the Delaware, per regulatory filings.

In a July 26 research report, Siebert Williams Shank & Co. Managing Director Gabriele Sorbara said the new processing plant could cost in the range of $180 million to $220 million over an 18- to 24-month period.

“With our estimated maintenance capex plus a majority owned new gas plant on the Pronto assets, we model total midstream spending at $200 million for 2024,” Sorbara said.

RELATED

Matador Resources Prioritizes Reducing Debt After $1.6B Acquisition

Service costs soften

Matador, like other oil and gas E&Ps, reported seeing some relief on high drilling and completion costs during the second quarter.

The company incurred drilling, completion and equipping capital expenses of $310 million during the quarter—14% below the company’s previous budget forecast of $358 million.

Matador expects to see decreased drilling, completion and equipping costs for the rest of this year and into 2024.

“Our long-term relationships with our vendors have been beneficial as we have begun to see service costs peaking across the board,” Foran said.

“Combining these overall peaking service costs with our capital and operational efficiencies, which include faster drilling and completion times, dual-fuel fracturing fleets, simultaneous and remote fracturing operations and the use of existing facilities, should position us well to increase production while still reducing costs,” he said.

The company anticipates that service cost deflation and other capital and operation efficiencies should bring in well cost savings of between $25 million and $30 million this year, compared to Matador’s prior outlook.

RELATED

Matador Closes $1.6 Billion Delaware Basin Bolt-on

Matador production outlook

Matador brought in strong second-quarter financial results and scored beats on key metrics including free cash flow, EBITDA and capital spending, Sorbara said.

But second-quarter oil production came in light compared to Siebert Williams Shank & Co.’s expectations, he said. And, Matador lowered its oil and gas production guidance for the second half of 2023 as the company works to bring more wells to sales.

Matador’s operated wells turning to sales in the third quarter are expected to be back-half weighted and won’t fully contribute to production until the fourth quarter, the company said in an investor presentation.

Matador estimates that its total third-quarter production will come in between 129,000 boe/d and 131,500 boe/d—down from the company’s original guidance of between 133,000 boe/d and 135,000 boe/d.

Average daily oil production is anticipated to be between 75,500 bbl/d and 76,500 bbl/d, down about 6% from a previous guidance range of 80,500 bbl/d to 81,500 bbl/d.

But Matador expects fourth-quarter oil production to come in at between 85,500 bbl/d to 86,500 bbl/d, down only 1.7% from its previous outlook of 87,500 bbl/d to 88,000 bbl/d.

Analysts at Capital One Securities anticipated that bearish investors would point to Matador’s decision to cut oil production guidance for the third and fourth quarters.

“[Management] has a well-known track record of setting the bar low when it comes to production guidance, so this should be taken into context,” Capital One Securities wrote in a July 26 report.

After closing at $56.54 per share on July 25, Matador’s stock price closed down over 6% at $52.76 per share on July 26, according to Yahoo Finance data.

Recommended Reading

US Clears 2.6-GW Offshore New England Wind Project

2024-04-04 - Located south of Martha’s Vineyard off of Massachusetts, the project consists of the 791-megawatt New England Wind 1 and the 1.87-GW New England Wind 2.

First US Utility-scale Offshore Wind Farm Starts Operations

2024-03-14 - The 12-turbine, 130-megawatt South Fork Wind project is a joint venture between Denmark's Orsted and New England-based electric utility Eversource.

US Gives Final Green Light to Sunrise Wind Offshore Project

2024-03-26 - The approval by the Bureau of Ocean Energy Management solidified Ørsted and Eversource’s commitment to the project with both taking final investment decisions.

Equinor, Ørsted/Eversource Land New York Offshore Wind Awards

2024-02-29 - RWE Renewables and National Grid’s Community Offshore Wind 2 project was waitlisted and may be considered for award and contract negotiations later, NYSERDA says.

Energy Transition in Motion (Week of Feb. 23, 2024)

2024-02-23 - Here is a look at some of this week’s renewable energy news, including approval of the construction and operations plan for Empire Wind offshore New York.