BKV Corp. CEO Chris Kalnin said the Barnett Shale E&P is standing “at the ready” to launch its IPO. The problem is, he argues, the public markets aren’t yet ready for BKV.

In November 2022, Denver-based BKV filed its paperwork with the Securities and Exchange Commission. But the company has yet to price or pull the trigger on a share offering, despite a limited amount of IPO activity in the E&P and oilfield services spaces last year.

In an exclusive interview with Hart Energy, Kalnin said that volatility in natural gas prices, geopolitical instability in the Middle East and multiple U.S. bank failures were among the issues last year that soured the E&P’s appetite for an IPO.

“It just feels like ’23 was not a real stable year,” Kalnin said. “There were too many things that were spooking investors, I think, to really get a solid run at an IPO market.”

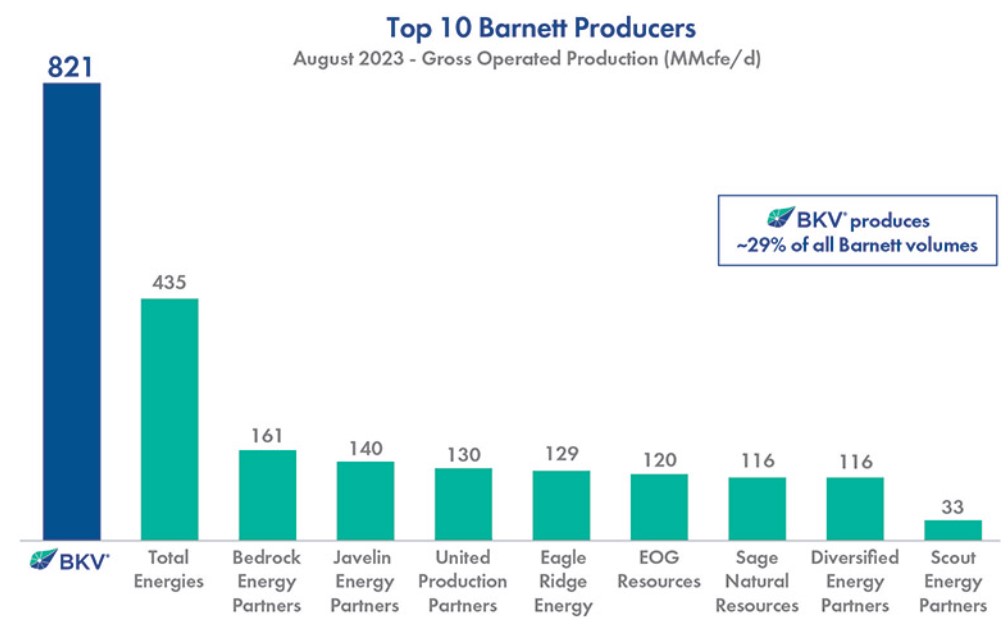

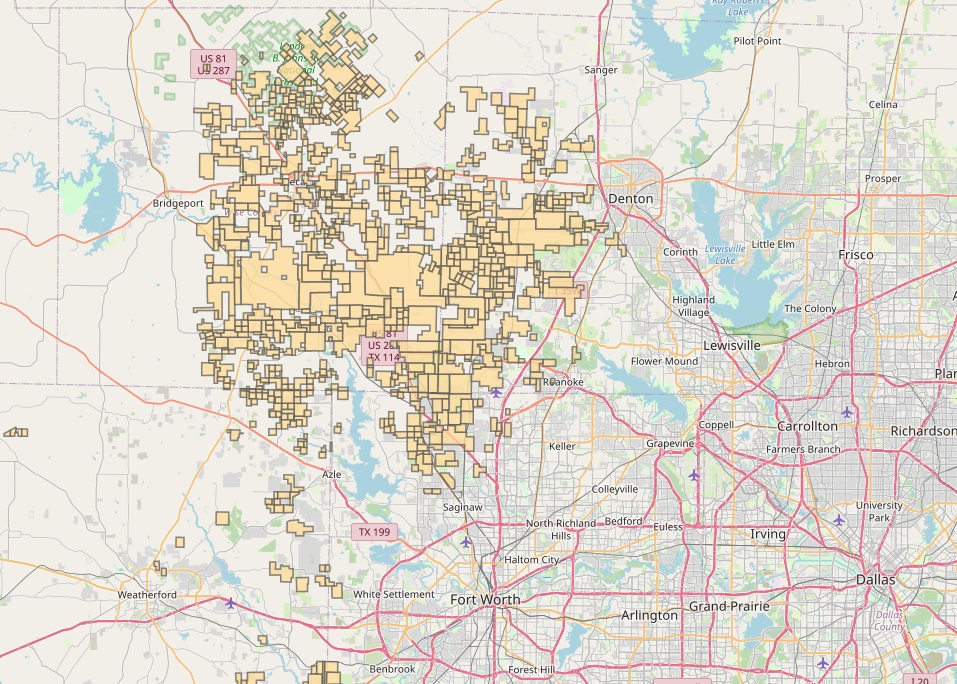

BKV is the largest producer in the Barnett Shale—the storied gas play near Fort Worth, Texas, unlocked by pioneer George Mitchell to usher in the shale revolution.

The rapid decline in natural gas prices in late 2022 and throughout 2023 came as a massive surprise to the market and chilled near-term investor interest in the gas sector, Kalnin said.

Henry Hub spot gas prices averaged $6.42/MMBtu in 2022 amid a confluence of supply-demand imbalances emerging from the COVID-19 downturn, Russia’s invasion of Ukraine and a myriad of other issues.

But prices fell over 60% to average $2.54/MMBtu in 2023 due to an oversupply of production and glutted storage inventories, according to the Energy Information Administration.

“I think that the general sentiment is super bullish gas long-term, but people don’t want to mistime that window,” Kalnin said.

BKV, along with most of the largest U.S. gas producers, believes better price stability will start to come into view later this year and into 2025 as a wave of new LNG export capacity comes online along the Gulf Coast.

That confidence in natural gas prices needs to also be mirrored by confidence in the broader economy, he said.

But one of the biggest things BKV is watching for is other IPOs successfully taking off. No one is eager to serve as the guinea pig.

“I think we need to see IPOs perform,” he said. “I think we need to see the IPO market come back in a big way.”

After several years of limited interest by the public capital markets, a small handful of energy-focused companies launched public offerings last year.

TXO Partners went public in January 2023. The MLP is led by Bob Simpson, an industry veteran who previously founded XTO Energy Inc., which sold to Exxon Mobil for $41 billion in 2010.

Kodiak Gas Services, a provider of contract compression services with a large footprint in the Permian Basin, made its public debut last summer.

And Midcontinent E&P Mach Natural Resources, which also is organized as an MLP, went public in October.

Energy stocks generally performed well in 2023, so some experts expect to see more energy IPO activity move forward this year.

“The IPO sector itself, if you think of it as a sector, requires a pretty stable market with a long-term bullishness in the overall capital markets’ view—because it’s a riskier asset class than just traditional equities,” Kalnin said.

BKV entered the Barnett in 2020 by acquiring over 289,000 net acres from Devon Energy. The company expanded its Barnett footprint by acquiring another 165,000 net acres from subsidiaries of Exxon Mobil in 2022.

BKV also has a smaller footprint of assets in northeastern Pennsylvania.

Production averaged 866.9 MMcfe/d (80% natural gas, 20% NGL) as of Sept. 30, 2023, according to the company’s most recent SEC filings; BKV’s total acreage position was approximately 497,000 net acres at that time.

RELATED

Barnett Shale’s Largest Producer BKV Corp Files for IPO

Capturing the gas value chain

BKV doesn’t want to be known just as a gas producer.

The company aims to differentiate itself from other competitors in the market with robust, net-zero emissions goals and a vision for an integrated gas value chain—from wellhead to pipeline, all the way to power generation and retail electricity.

BKV—in partnership with its financial sponsor, Thai energy giant Banpu—owns interests in two combined cycle gas and steam turbine power plants in Temple, Texas—Temple I and Temple II.

The plants, located within the Texas electric grid’s north zone market, have annual average power generation capacities of 752 MW and 751 MW, respectively.

The company also owns midstream assets for gathering, processing and transporting natural gas produced by its own upstream assets, as well as for third-party producers.

BKV plans to establish midstream contracts in the near term to allow the company to supply its own natural gas directly to its power plants in Temple, the company said in regulatory filings.

Last February, BKV launched its own retail electric business, BKV Energy, to sell power to commercial, industrial and residential retail customers in Texas. Since launching last year, BKV Energy has nabbed more than 34,000 customers.

Kalnin likens BKV’s vision to what we saw the big oil majors start doing in the 1950s: They didn’t just pump oil and gas—they started building refineries and fuel stations and their own midstream systems.

Why?

“One, they wanted to build relationships with the end customers,” Kalnin said. “But importantly, they wanted to reduce the volatility of just being a commodity producer and capture margin along the entire value chain.”

If there was a downturn in commodity prices, the majors could make up some of those losses through gains on refining margins, or retail sales at gas stations, he said. That model has not been as popular with investors of late, but sentiments can change.

And BKV wants to do all of this while achieving net-zero Scope I and Scope 2 emissions by the end of 2025. To meet that goal, BKV is working on several carbon capture, utilization and storage (CCUS) projects to permanently sequester emissions from its owned-and-operated upstream assets.

Commercial operations for BKV’s first, high-concentration CCUS project, Barnett Zero, began last year; first volumes were injected in November 2023. The Barnett Zero project separates CO₂ from substantially all of BKV’s EnLink Midstream-gathered gas production.

Kalnin believes that the market for a premium product like carbon-sequestered gas, or carbon-negative gas, will only grow as global demand grows for cleaner forms of energy.

Last August, BKV inked an agreement with French energy company Engie for the sale and purchase of BKV’s carbon-sequestered gas.

Under the contract’s terms, BKV committed to deliver up to 10,000 MMBtu/d of carbon-sequestered gas. Delivery is expected to begin early this year.

BKV expects its second CCUS project to begin sequestration by the end of this year.

RELATED

Recommended Reading

Initiative Equity Partners Acquires Equity in Renewable Firm ArtIn Energy

2024-04-26 - Initiative Equity Partners is taking steps to accelerate deployment of renewable energy globally, including in North America.

Energy Transition in Motion (Week of April 26, 2024)

2024-04-26 - Here is a look at some of this week’s renewable energy news, including the close of a $1.4 billion decarbonization-focused investment fund.

No Silver Bullet: Chevron, Shell on Lower-carbon Risks, Collaboration

2024-04-26 - Helping to scale lower-carbon technologies, while meeting today’s energy needs and bringing profits, comes with risks. Policy and collaboration can help, Chevron and Shell executives say.

Solar Sector Awaits Feds’ Next Move on Tariffs

2024-04-25 - A group of solar manufacturers want the U.S. to impose tariffs to ensure panels and modules imported from four Southeast Asian countries are priced at fair market value.

Solar Panel Tariff, AD/CVD Speculation No Concern for NextEra

2024-04-24 - NextEra Energy CEO John Ketchum addressed speculation regarding solar panel tariffs and antidumping and countervailing duties on its latest earnings call.