Optimism about higher oil prices continues to be tamped down by ongoing weakness in the major global economies. (Source: Shutterstock)

The price of Brent crude ended the week at $93.27 after closing the previous week at $93.93. The price of WTI ended the week at $90.03 after closing the previous week at $90.77. The price of DME Oman ended the week at $94.08 after closing the previous week at $95.28.

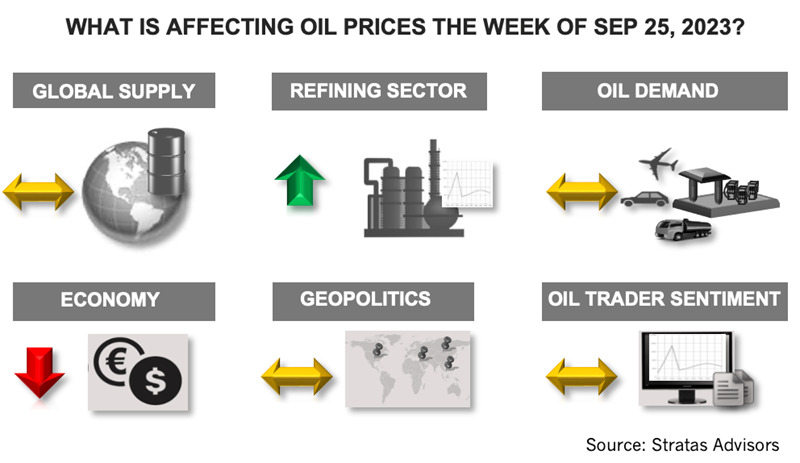

Last week, Russia announced a temporary ban of gasoline and diesel exports except for exports to Belarus, Kazakhstan, Armenia and Kyrgyzstan. At this point it is not clear how long the ban will last; however, Russia indicated that the ban is intended to stabilize the domestic market, including the agriculture sector. During 2022, Russia exported around 90,000 bbl/d of gasoline and 670,000 bbl/d of diesel. The total diesel market is around 28.30 MMbbl/d. The ban will put upward pressure on product spreads—most notably diesel spreads—especially since diesel inventories are below the 10-year average. The impact on crude oil prices will be less direct and less significant, given that the export ban does not apply to crude oil.

Optimism about higher oil prices continues to be tamped down by ongoing weakness in the major global economies. Last week, as expected, the U.S. Federal Reserve kept interest rates unchanged; however, the Federal Reserve warned that more interest rates will occur if inflation continues to run at the current pace—which is more than twice the Fed’s target of 2.0%. The leading economic indicators associated with the U.S. and Europe are showing further contraction in the manufacturing sector, while expansion in the service sector is waning. Meanwhile, China’s economy continues to be hampered by weak export markets, which resulted in China’s exports decreasing by 8.8% in August from the previous year, and even with a 7.4% decrease in imports, China’s trade surplus in August decreased to $68.36 billion from $80.60 billion in July.

RELATED: Chart Talk: Global Oil Prices on a Massive Upward Trend

Another factor putting downward pressure on oil prices is the strength of the U.S. dollar, with the U.S. Dollar Index ending last week at 105.38, rebounding from 99.91 in early July of this year. Since January of this year, the Chinese currency has weakened from 6.70 to the U.S. dollar to 7.30. The euro has also weakened against the U.S. dollar, with the U.S. dollar to euro decreasing from 1.12 in early July to 1.06. Additionally, while we are forecasting that oil demand in the fourth quarter will increase by 2.2 MMbbl/d in comparison to fourth quarter 2022, oil demand will increase by only 0.100 MMbbl/d in comparison to third quarter 2023.

From a supply-side perspective, we believe Saudi Arabia has reached its limit in terms of productions cuts because it is not willing to reduce production below 9 MMbbl/d. Additionally, the U.S. still has the potential to increase production, even with the reduction in the rig count, given the remaining inventory of DUC wells. There are, nevertheless, risks to supply—especially with respect to African producers and the sanctioned producers. However, African producers have shown some resiliency this year, including Libya’s production which has overcome the recent natural disaster. The sanctioned producers have also shown resiliency. Besides Russia, Venezuela and Iran have increased their production and exports. Iran’s production has increased to 3.15 MMbbl/d in August, which are the highest level since 2018, when additional sanctions were imposed on Iran by the U.S. Iran has further upside potential given that Iran’s oil production was 3.8 MMbbl/d prior to the sanctions.

For the upcoming week, however, we are expecting oil prices to be under pressure, with the price of Brent not able to break through $95 last week and may test $90 again.

For a complete forecast of refined products and prices, please refer to our Short-term Outlook.

About the Author: John E. Paise, president of Stratas Advisors, is responsible for managing the research and consulting business worldwide. Prior to joining Stratas Advisors, Paisie was a partner with PFC Energy, a strategic consultancy based in Washington, D.C., where he led a global practice focused on helping clients (including IOCs, NOC, independent oil companies and governments) to understand the future market environment and competitive landscape, set an appropriate strategic direction and implement strategic initiatives. He worked more than eight years with IBM Consulting (formerly PriceWaterhouseCoopers, PwC Consulting) as an associate partner in the strategic change practice focused on the energy sector while residing in Houston, Singapore, Beijing and London.

Recommended Reading

CEO: Coterra ‘Deeply Curious’ on M&A Amid E&P Consolidation Wave

2024-02-26 - Coterra Energy has yet to get in on the large-scale M&A wave sweeping across the Lower 48—but CEO Tom Jorden said Coterra is keeping an eye on acquisition opportunities.

E&P Earnings Season Proves Up Stronger Efficiencies, Profits

2024-04-04 - The 2024 outlook for E&Ps largely surprises to the upside with conservative budgets and steady volumes.

CEO: Magnolia Hunting Giddings Bolt-ons that ‘Pack a Punch’ in ‘24

2024-02-16 - Magnolia Oil & Gas plans to boost production volumes in the single digits this year, with the majority of the growth coming from the Giddings Field.

U.S. Shale-catters to IPO Australian Shale Explorer on NYSE

2024-05-04 - Tamboran Resources Corp. is majority owned by Permian wildcatter Bryan Sheffield and chaired by Haynesville and Eagle Ford discovery co-leader Dick Stoneburner.

BP Pursues ‘25-by-‘25’ Target to Amp Up LNG Production

2024-02-15 - BP wants to boost its LNG portfolio to 25 mtpa by 2025 under a plan dubbed “25-by-25,” upping its portfolio by 9% compared to 2023, CEO Murray Auchincloss said during the company’s webcast with analysts.