The week ahead will be driven by sentiment more than fundamentals, with funds likely to continue unwinding bullish positions. Ideally, a reasonable floor will be quickly found but more likely prices will fluctuate throughout the next two weeks as markets seek a price that balances potential disruptions against current production.

Topic Of Interest

The supply problems dominating headlines last week are now old news, although many of the actual outages persist. Venezuela, Iran, Libya and even Russia, all have very real on-the-ground issues. All of these problems were forgotten when United States production posted another record breaking weekly number, with EIA estimates placing production at 12.3 MMbbl/d in the week ended April 26.

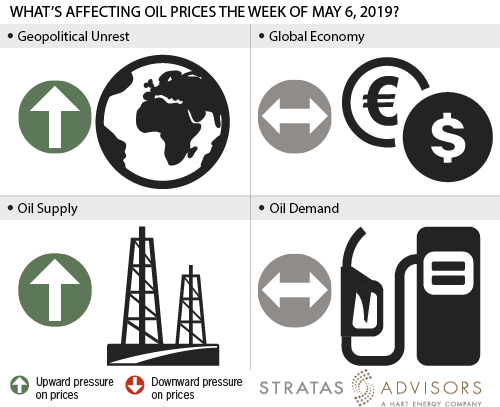

Geopolitics: Positive

Geopolitics will be a positive factor in the week ahead. The end of Iran sanctions waivers officially came into effect, meaning any shipments transiting the region will be under a microscope as markets attempt to assess compliance levels. Fighting in Libya continues, and without international intervention, could continue through the summer, impeding flows.

Global Economy: Neutral

The global economy will be a neutral factor in the week ahead. The U.S. dollar is at a nearly two-year high supported by strong US capital goods orders and strong GDP. Although a strong dollar can weigh on crude prices, the overall healthy numbers bode well for demand.

Oil Supply: Negative

Supply will be a negative factor in the week ahead as markets suddenly remembered the juggernaut that is US production. While supply issues persist, their impact will be seen in differentials more than headline Brent in the week ahead.

Oil Demand: Neutral

While strong, oil demand is likely to be a neutral factor in the week ahead. Demand in India and surrounding countries could be impacted by Cyclone Fani, but this will be temporary. Elsewhere, demand remains generally healthy, but mixed. The U.S. saw distillate demand drop, although stocks continued to fall, likely due to heavy refinery maintenance. In Europe, total product stocks have bumped above the five-year average, due to builds in jet fuel and gasoil, although these builds appear to be slowing.

Recommended Reading

Guyana’s Stabroek Boosts Production as Chevron Watches, Waits

2024-04-25 - Chevron Corp.’s planned $53 billion acquisition of Hess Corp. could potentially close in 2025, but in the meantime, the California-based energy giant is in a “read only” mode as an Exxon Mobil-led consortium boosts Guyana production.

US Interior Department Releases Offshore Wind Lease Schedule

2024-04-24 - The U.S. Interior Department’s schedule includes up to a dozen lease sales through 2028 for offshore wind, compared to three for oil and gas lease sales through 2029.

Utah’s Ute Tribe Demands FTC Allow XCL-Altamont Deal

2024-04-24 - More than 90% of the Utah Ute tribe’s income is from energy development on its 4.5-million-acre reservation and the tribe says XCL Resources’ bid to buy Altamont Energy shouldn’t be blocked.

Mexico Presidential Hopeful Sheinbaum Emphasizes Energy Sovereignty

2024-04-24 - Claudia Sheinbaum, vying to becoming Mexico’s next president this summer, says she isn’t in favor of an absolute privatization of the energy sector but she isn’t against private investments either.

Venture Global Gets FERC Nod to Process Gas for LNG

2024-04-23 - Venture Global’s massive export terminal will change natural gas flows across the Gulf of Mexico but its Plaquemines LNG export terminal may still be years away from delivering LNG to long-term customers.