The price of Brent crude ended the week at $83.36 after closing the previous week at $80.75. With the increase of last week, the price of Brent crude moved back above its 200-day moving average. The price of WTI ended the week at $79.77 after closing the previous week at $76.49. The price of DME Oman crude ended the week at $82.93 after closing the previous week at $80.58.

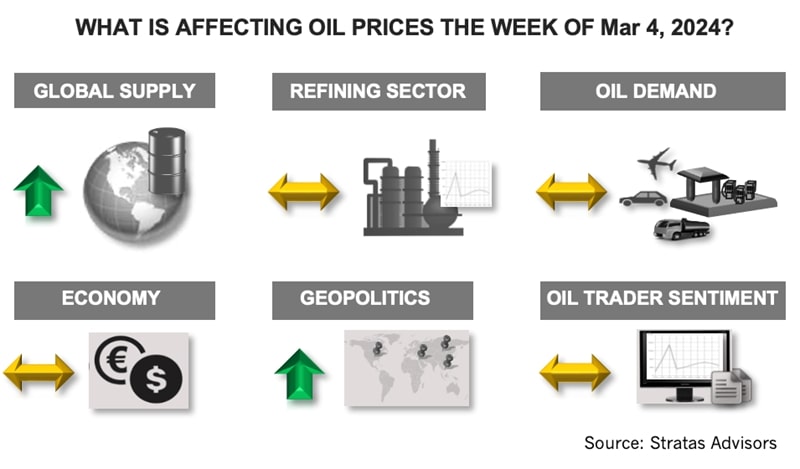

On March 3, it was reported by the Saudi Arabia Press Agency that Saudi Arabia will extend its voluntary crude production cut of 1 MMbbl/d until the end of the second quarter. Additionally, Russian Deputy Prime Minister Alexander Novak stated that Russia will reduce its production and export supplies by a combined 471,000 bbl/d until the end of June. The announcements align with our expectations, as well as most involved in the oil market. As such, it is likely that market reaction and the impact on oil prices will be muted.

With respect to oil demand, the economic outlook continues to look mixed:

- The latest economic data for the U.S. were relatively positive, but not all indicators are flashing green. The personal consumption expenditures (PCE) price index increased by 0.3% from the previous month and 2.4% from the previous year. The price for goods decreased by 0.2%; conversely, prices for services increased by 0.6%. Food prices increased by 0.5%, while energy prices decreased by 1.4%. Stripping out food and energy, the PCE price index increased by 0.4% for the month and 2.8% from the previous year. The rising cost of food and housing is contributing to the depressed level of the Conference Board’s Consumer Confidence Index, which decreased from 110.9 in January to 106.7 in February. In comparison, before COVID-19, the index was nearly 140. Another concern for the U.S. economy is the weakness associated with the manufacturing sector. The ISM Manufacturing PMI decreased from 49.1 in January to 47.3 in February – and is the 16th consecutive month of contraction.

- The European Commission recently reduced its growth forecast for the EU to 0.9% from its previous forecast of 1.3%. From a positive perspective, the forecast of annual inflation for the Euro area has been reduced from 2.8% in January to 2.6%.

- China’s economy continues to be hampered by weakness in the property market, which represents 25% of China’s GDP and 70% of household wealth. As such, weakness in the property market affects consumer demand. Other negative factors include weak export markets and high youth unemployment. Moreover, the manufacturing sector continues to contract. The official manufacturing PMI decreased from 49.2 in January to 49.1 in February – and is the fifth consecutive month of contraction. Together all these factors are contributing to deflationary pressures. China is expected to release its official growth target for 2024 this upcoming week.

While the Russia-Ukraine conflict and the Israel-Hamas conflict are having a limited impact on oil prices, recent developments are raising concerns about the potential for both conflicts moving to more dangerous phases.

- In response to recent talk suggesting direct military involvement of NATO members in support of Ukraine, Putin stated in his annual state of the nation speech that NATO countries will be risking a nuclear war. To add to the heightened rhetoric, it appears that Russia intercepted an internet conference between German officers that took place on Feb. 19 and included discussions about military personal from the U.S. and U.K. already in Ukraine. Additionally, training of Ukrainian staff in Germany for a mission involving the use of Taurus missiles was discussed, as well as targeting the Kerch Bridge that connects Russia’s mainland with Crimea.

- In the aftermath of the more than 100 Palestinian civilians killed in northern Gaza while trying to reach aid being provided by a truck convoy, there is increasing pressure on the Biden Administration to take further action. While Biden expressed optimism about the talks pertaining to a ceasefire, a deal still has not been reached. The talks that have been taking place in Qatar and Paris involving a 40-day truce have not been able to resolve key issues between Israel and Hamas – including Hamas’ demand for a permanent end to war with a withdrawal of Israeli troops. Tensions could increase further with the start of Ramadan on March 10. Leadership of Hamas is calling on Palestinians in Jerusalem and the west Bank to march to Al-Aqsa, which is one of the holiest sites for Muslims, as well as for Jews. Conversely, Israel has indicated that it is considering restrictions on visits to Al-Aqsa during Ramadan.

For the upcoming week, we are expecting the price of Brent will move sideways and will struggle to break through $85.00.

For a complete forecast of refined products and prices, please refer to our Short-term Outlook.

About the Author: John E. Paisie, president of Stratas Advisors, is responsible for managing the research and consulting business worldwide. Prior to joining Stratas Advisors, Paisie was a partner with PFC Energy, a strategic consultancy based in Washington, D.C., where he led a global practice focused on helping clients (including IOCs, NOC, independent oil companies and governments) to understand the future market environment and competitive landscape, set an appropriate strategic direction and implement strategic initiatives. He worked more than eight years with IBM Consulting (formerly PriceWaterhouseCoopers, PwC Consulting) as an associate partner in the strategic change practice focused on the energy sector while residing in Houston, Singapore, Beijing and London.

Recommended Reading

Kosmos Energy’s RBL Increased, Maturity Date Extended

2024-04-29 - Kosmos Energy’s reserve-based lending facility’s size has been increased by about 8% to $1.35 billion from $1.25 billion, with current commitments of approximately $1.2 billion.

Barnett & Beyond: Marathon, Oxy, Peers Testing Deeper Permian Zones

2024-04-29 - Marathon Oil, Occidental, Continental Resources and others are reaching under the Permian’s popular benches for new drilling locations. Analysts think there are areas of the basin where the Permian’s deeper zones can compete for capital.

NOV Announces $1B Repurchase Program, Ups Dividend

2024-04-28 - NOV expects to increase its quarterly cash dividend on its common stock by 50% to $0.075 per share from $0.05 per share.

Repsol to Drop Marcellus Rig in June

2024-04-28 - Spain’s Repsol plans to drop its Marcellus Shale rig in June and reduce capex in the play due to the current U.S. gas price environment, CEO Josu Jon Imaz told analysts during a quarterly webcast.

US Drillers Cut Most Oil Rigs in a Week Since November

2024-04-26 - The number of oil rigs fell by five to 506 this week, while gas rigs fell by one to 105, their lowest since December 2021.