Stratas Advisors predicts that for another week, oil prices will be under pressure due in part to supply/demand and global economy issues. (Source: Shutterstock.com)

The price of Brent crude ended the week at $84.80 after closing the previous week at $86.81. The price movement aligned with our expectations that the price of Brent crude would be under pressure last week. The price of WTI ended the week at $81.28 after closing the previous week at $83.19. The price of DME Oman ended the week at $86.03 after closing the previous week at $88.01.

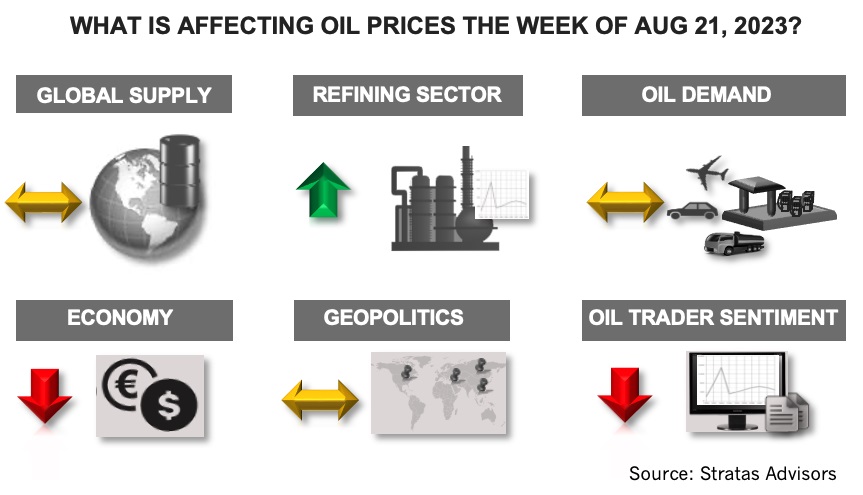

While the supply cuts by OPEC+ are resulting in demand outstripping supply and establishing a price floor of around $80.00 for Brent crude, the supply cuts have also resulted in spare capacity of nearing 6.0 million bbl/d. As such, if crude prices start to ramp-up, it will be tempting for some of the OPEC+ producers to increase supply, which will put downward pressure on oil prices. Additionally, as we have been highlighting (and highlighting and highlighting) concerns about the global economy will continue to be a dampening factor for oil prices.

Moreover, there is nothing appearing on the horizon that will change the current dynamics. Geopolitics are not likely to reduce supply; in fact, it is likely that the geopolitical trends will have less impact on oil supply. Last week, we highlighted that there will be increased pressure on Ukraine to seek a negotiated settlement. While the Biden Administration continues to request more funding for Ukraine, the support of the US voters is waning. A recent poll by CNN shows that 55% of US citizens believe that the US Congress should not provide additional funding to support Ukraine, which is a significant shift since February 2022 when 62% of US citizens were in favor of more support for Ukraine. With the US presidential campaign starting, it is likely that support for the Ukraine will be under further pressure. Another sign of support decreasing is the initiation of efforts to prep the US public for a change in approach, as illustrated by The Washington Post reporting on Sunday that the intelligence community has determined that Ukraine’s counter-offensive has not met its core objectives. Support is also starting to soften in Germany. A recent poll by Germany’s public broadcaster (ARD) showed that 52% of Germany’ public opposed sending long-range missiles to Ukraine.

We also do not see concerns about the global economy being addressed anytime soon. Back at the end of July we highlighted that a major risk for the US economy was the growing dependency on consumer spending for economic growth. Consumer debt is at an all-time high, as is the interest rate being applied to the debt. Additionally, the job market is cooling with a slowing rate of job additions in 2023, which has decreased significantly from 2022 (399,000 monthly to 278,000). Last week, the Federal Reserve Bank of San Francisco released a new study, which states that the excess savings that consumers accumulated during the COVID pandemic (and peaked at $2.1 trillion in August 2021) will be gone by the end of the 3Q if the drawdown continues at the current pace of $100 billion per month. At the same time, the manufacturing sector has been in contraction since November of 2022. The service sector is still growing; however, growth has been slowing down since May of this year. Another worrisome sign is that the Conference Board’s monthly Index of Leading Economic Indicators has been declining since April of 2022. China’s economy continues to be hindered by weakening manufacturing sector and exports, disappointing consumer spending, and an overleveraged real estate sector. The latter is illustrated by China Evergrande Group (one of China’s major property developer), which defaulted on debt payments in December 2021, and filed last week for bankruptcy protection in the US. Europe continues to be hindered by elevated inflation, increasing interest rates and is likely to face further energy-related challenges in the coming months. The Euro continues to weaken against the US dollar, falling from 1.124 in the middle of July to 1.0882. Recent data from Eurostat show that EU business bankruptcies increased by 8.4% in comparison to 1Q and registrations of new businesses decreased by 0.6%.

For another week, we are expecting that the price of Brent crude oil will be under pressure.

For a complete forecast of refined products and prices, please refer to our Short-term Outlook.

Recommended Reading

Patterson-UTI Braces for Activity ‘Pause’ After E&P Consolidations

2024-02-19 - Patterson-UTI saw net income rebound from 2022 and CEO Andy Hendricks says the company is well positioned following a wave of E&P consolidations that may slow activity.

Baker Hughes Awarded Saudi Pipeline Technology Contract

2024-04-23 - Baker Hughes will supply centrifugal compressors for Saudi Arabia’s new pipeline system, which aims to increase gas distribution across the kingdom and reduce carbon emissions

E&P Earnings Season Proves Up Stronger Efficiencies, Profits

2024-04-04 - The 2024 outlook for E&Ps largely surprises to the upside with conservative budgets and steady volumes.

CEO: Coterra ‘Deeply Curious’ on M&A Amid E&P Consolidation Wave

2024-02-26 - Coterra Energy has yet to get in on the large-scale M&A wave sweeping across the Lower 48—but CEO Tom Jorden said Coterra is keeping an eye on acquisition opportunities.

Endeavor Integration Brings Capital Efficiency, Durability to Diamondback

2024-02-22 - The combined Diamondback-Endeavor deal is expected to realize $3 billion in synergies and have 12 years of sub-$40/bbl breakeven inventory.