The price of Brent crude ended the week at $90.89 after closing the previous week at $87.00. The price of WTI ended the week at $86.71 after closing the previous week at $83.17. The price of DME Oman crude ended the week at $91.06 after closing the previous week at $87.28.

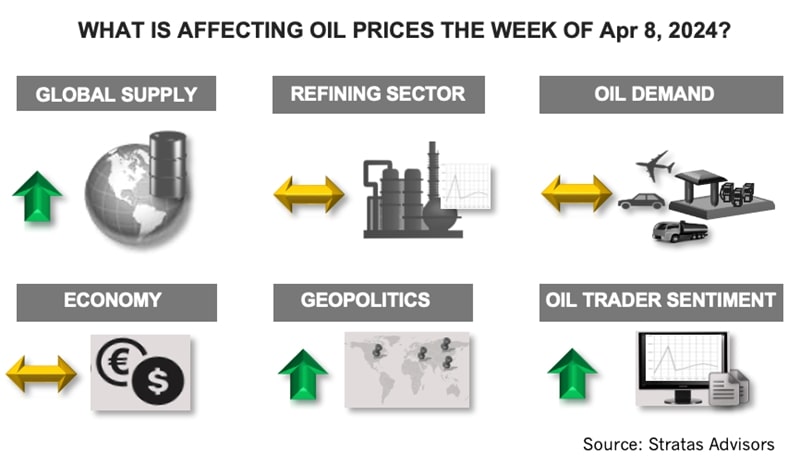

Oil prices continue to be supported by tighter supply conditions with the maintenance of supply cuts by OPEC+ and less robust supply increases from non-OPEC producers – including the U.S. The latest EIA report indicated that U.S. oil production was 13.1 MMbbl/d, which is unchanged from the previous three weeks. Last week, the number of operating oil rigs in the U.S. decreased by 3 and now stands at 506, which compares to the pre-COVID level of 683 that occurred during the week of March 13, 2020. One year ago, the U.S. rig count was 592. We are still expecting that U.S. production will increase this year but at only about half of the increase of last year. The fire at Pemex’s Akal-B platform adds to the uncertainty about supply. Even though the volumes that could be directly affected are relatively minor, the fire comes on the heels of reports that Pemex is cancelling some 400,000 bbl/d of exports scheduled for April to make crude oil available for its Dos Bocas refinery.

We are also expecting slightly higher demand growth and have recently increased our demand growth forecast for 2024 to 1.41 MMbbl/d from our previous forecast of 1.3 MMbbl/d. We are also seeing some signs of improvement in China’s economy. The official PMI for manufacturing in March increased from 49.1 in February to 50.8 in March, which is the highest level in thirteen months. It is also the first reading above 50 (which indicates expansion in 12 months. Additionally, the index for new orders increased from 49 to 53 and the new manufacturing export order index increased from 46.3 to 51.3. Furthermore, the composite PMI (including manufacturing and non-manufacturing) increased from 50.9 to 52.7, which is the highest level since May 2023.

Additionally, the sentiment of oil traders is becoming more bullish. The net long positions of WTI traders have increased significantly with net long positions doubling since early February and are now at the highest level since October 2023 when the price of WTI was nearly $90.

Obviously, geopolitics are also providing a boost for oil prices with the conflicts in Ukraine and Gaza escalating – and while crude oil and oil products continue to flow, the possibility of disruption is increasing, which is resulting in a risk premium with respect to oil prices.

The situation in the Middle East is only becoming more volatile and dangerous with the increasing possibility of a wider conflict. Last week, Israel attacked Iran’s embassy in Syria which killed seven Iranian officers, including a general who was a senior officer in Iran’s Revolutionary Guard. Additionally, there continues to be military action along the border with Lebanon between Israel and Hezbollah, and over the weekend, there was an exchange of aerial attacks. So far, Iran has exhibited constraint since the beginning of the Israel-Hamas conflict in that Iran has not taken direct action against Israel, but with the high-profile attack on its embassy, there is concern that Iran will launch some sort of response against Israeli assets – and even, U.S. assets. Meanwhile, the situation in Gaza remains volatile. Talks between the two parties were to resume this weekend in Cairo, but so far, the negotiations are at an impasse with Hamas holding to its position of a permanent ceasefire with Israel moving all its troops from Gaza. Israel has removed all its troops from southern Gaza – however, it appears not because of a change in strategy, but to prepare for an invasion of Rafah.

For a complete forecast of refined products and prices, please refer to our Short-term Outlook.

About the Author: John E. Paisie, president of Stratas Advisors, is responsible for managing the research and consulting business worldwide. Prior to joining Stratas Advisors, Paisie was a partner with PFC Energy, a strategic consultancy based in Washington, D.C., where he led a global practice focused on helping clients (including IOCs, NOC, independent oil companies and governments) to understand the future market environment and competitive landscape, set an appropriate strategic direction and implement strategic initiatives. He worked more than eight years with IBM Consulting (formerly PriceWaterhouseCoopers, PwC Consulting) as an associate partner in the strategic change practice focused on the energy sector while residing in Houston, Singapore, Beijing and London.

Recommended Reading

Range Resources Holds Production Steady in 1Q 2024

2024-04-24 - NGLs are providing a boost for Range Resources as the company waits for natural gas demand to rebound.

Canadian Natural Resources Boosting Production in Oil Sands

2024-03-04 - Canadian Natural Resources will increase its quarterly dividend following record production volumes in the quarter.

Keeping it Simple: Antero Stays on Profitable Course in 1Q

2024-04-26 - Bucking trend, Antero Resources posted a slight increase in natural gas production as other companies curtailed production.

PrairieSky Adds $6.4MM in Mannville Royalty Interests, Reduces Debt

2024-04-23 - PrairieSky Royalty said the acquisition was funded with excess earnings from the CA$83 million (US$60.75 million) generated from operations.

Exxon Mobil, Chevron See Profits Fall in 1Q Earnings

2024-04-26 - Chevron and Exxon Mobil are feeling the pinch of weak energy prices, particularly natural gas, and fuels margins that have cooled in the last year.