Rumors are swirling that Marathon is searching for deals of its own to gain greater scale in U.S. shale. (Source: Shutterstock)

With a wave of M&A (and deal rumors) crashing over the U.S. upstream sector, Marathon Oil says it’s not rushing to strike a deal.

The market has seen “significant consolidation” in the oil and gas E&P space recently, Marathon Oil Corp. Chairman, President and CEO Lee Tillman said during the company’s third-quarter earnings call.

October was a historic month for energy megadeals: Exxon Mobil Corp. announced a $60 billion acquisition of Pioneer Natural Resources, extending its runway of top-tier drilling locations in the Permian Basin.

Less than two weeks later, Chevron Corp. unveiled a $53 billion takeover of Hess Corp., giving the California-based major greater scale in international offshore and U.S. shale production.

The Permian Basin, America’s top oil-producing region, has also seen a flurry of consolidation as private equity-backed drillers and small mid-caps sell to larger operators.

“While every transaction is unique with its own set of facts and circumstances, a common takeaway is clear,” Tillman said. “Low-cost, high-quality, traditional oil and gas assets will have a critical role to play in helping meet global energy demand for decades to come.”

Rumors are swirling that Marathon is searching for deals of its own to gain greater scale in U.S. shale. Marathon has reportedly held preliminary conversations with Devon Energy Corp. about a potential combination.

Tillman declined to address the market speculation during the company’s earnings call—but he said Marathon certainly isn’t ruling out growth through M&A.

“I will reiterate that it's our duty to always explore avenues to further enhance the long-term value for our shareholders,” he said.

RELATED

Chevron Buys Hess for $53B as Historic M&A Bonanza Continues

Checking boxes

For Marathon to consider M&A, large or small, opportunities need to check the right boxes for the company, Tillman said.

“Any transaction must meet our tried and true principles of financial and return of cash accretion, industrial logic within our existing basins, inventory life extension and no harm to our investment grade balance sheet,” he said.

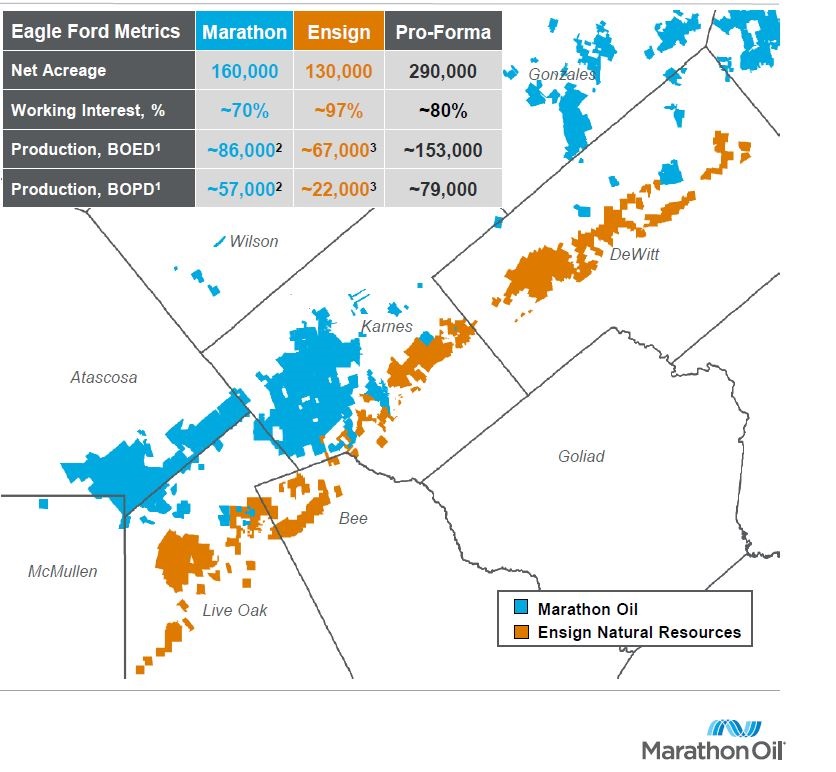

Marathon’s $3 billion cash acquisition of Ensign Natural Resources’ assets in the Eagle Ford Shale last year did check the right boxes for the company. In that sense, Tillman said the Ensign deal “was a little bit of a unicorn.”

The Ensign acquisition added 130,000 net acres adjacent to Marathon’s existing Eagle Ford acreage.

“We have a tremendous amount of organic opportunity that was made only stronger with the addition of Ensign,” Tillman said.

And as Marathon evaluates the current landscape for oil and gas M&A, the company insists that its bar for potential deals remains high.

“As we look at what's in the market today or rumored to be in the market today, I have to say, frankly, that they really don't tick the boxes on our criteria,” Tillman said. “They may tick one or two, possibly, but we can be patient.”

RELATED

Marathon Closes $3B Eagle Ford Buy From Ensign

Quarterly results

Marathon’s U.S. production averaged 369,000 boe/d during the third quarter, up from 356,000 boe/d in the previous quarter.

Crude oil production averaged 189,000 bbl/d, up from 181,000 bbl/d during the second quarter.

The company’s output from the Eagle Ford averaged 158,000 boe/d, including 80,000 net bbl/d of oil production.

Production in the Bakken averaged 121,000 boe/d, including 77,000 net bbl/d. Anadarko Basin production averaged 46,000 net boe/d, including 9,000 bbl/d.

And in the Permian Basin, Marathon’s production averaged 42,000 net boe/d, including 22,000 net bbl/d.

Also during the quarter, Marathon announced inking a five-year LNG sales agreement with Glencore Energy U.K. Ltd. The agreement includes a portion of Glencore’s equity natural gas from the Alba Field offshore Equatorial Guinea.

Equatorial Guinea production came in at 52,000 boe/d during the third quarter, including 9,000 net bbl/d.

Marathon returned $476 million to shareholders during the quarter, including $415 million in share repurchases and $61 million disbursed through base dividends.

Recommended Reading

NOG Closes Utica Shale, Delaware Basin Acquisitions

2024-02-05 - Northern Oil and Gas’ Utica deal marks the entry of the non-op E&P in the shale play while it’s Delaware Basin acquisition extends its footprint in the Permian.

Vital Energy Again Ups Interest in Acquired Permian Assets

2024-02-06 - Vital Energy added even more working interests in Permian Basin assets acquired from Henry Energy LP last year at a purchase price discounted versus recent deals, an analyst said.

California Resources Corp., Aera Energy to Combine in $2.1B Merger

2024-02-07 - The announced combination between California Resources and Aera Energy comes one year after Exxon and Shell closed the sale of Aera to a German asset manager for $4 billion.

DXP Enterprises Buys Water Service Company Kappe Associates

2024-02-06 - DXP Enterprise’s purchase of Kappe, a water and wastewater company, adds scale to DXP’s national water management profile.

Tellurian Exploring Sale of Upstream Haynesville Shale Assets

2024-02-06 - Tellurian, which in November raised doubts about its ability to continue as a going concern, said cash from a divestiture would be used to pay off debt and finance the company’s Driftwood LNG project.