With potentially billions of dollars at play, natural gas—known as a transition fuel to some and a destination fuel to others—finds itself stuck in the middle again.

Its role in companies’ ability to claim the 45V hydrogen production tax credit offered in the Inflation Reduction Act (IRA) is fueling more uncertainty. That uncertainty, industry experts say, could give some producers of blue hydrogen (natural gas with carbon capture and storage) and their partners pause. Discussion continues on the proposed rules released in late December by the U.S. Treasury Department and Internal Revenue Service (IRS) as the departments near the Feb. 26 close of public comments.

“I think there are certainly some unanswered questions for blue hydrogen producers,” Connor Thompson, legal scholar for the University of Houston Law Center, told Hart Energy. The government is seeking feedback from stakeholders on how to verify emissions for hydrogen production from fossil fuel and biomass resources, how to adopt rules to verify the rate of carbon capture at blue hydrogen facilities and how the so-called three pillars—deliverability, hourly matching and new supply—should be or can be adopted to fossil and biomass production of hydrogen.

“The initial 45V notice of proposed rule making was interesting particularly for blue hydrogen producers in what it didn’t provide. It was really largely silent on blue hydrogen,” Thompson said. “In my opinion, the document issued by IRS and Treasury really dealt with the requirements for green hydrogen, electrolytic hydrogen, and the adoption of the three pillars really focuses in those green hydrogen producers.”

Proponents are counting on hydrogen to help decarbonize a fossil-fuel dependent society and lower emissions. Predominately used today in oil refining and ammonia production, hydrogen is seen as a route to decarbonize hard-to-abate sectors such as steel, maritime and aviation, while also powering fuel cells, generating electricity, storing energy and serving as a transportation fuel.

Though natural gas is abundant, cleaner than most other fossil fuels and could put hydrogen on a faster track to development using existing infrastructure, there are concerns about its cleanliness, particularly potential leakage.

Taming the ‘super pollutant’

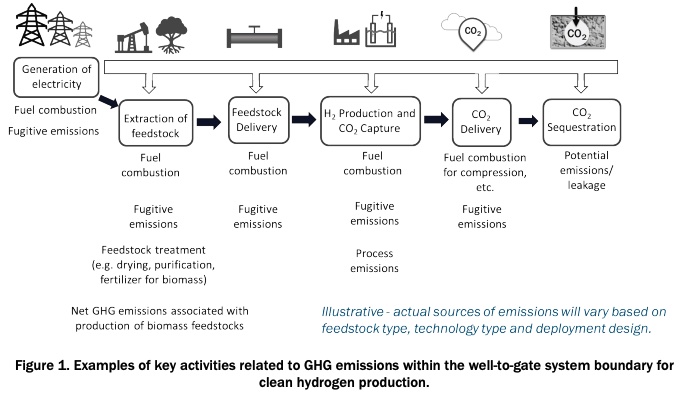

The GREET (Greenhouse gases, Regulated Emissions and Energy use in Technologies) model, is updated annually and will be used by the Treasury Department to calculate lifecycle greenhouse gas (GHG) emissions of hydrogen production from well to gate.

The 45VH2-GREET 2023 assumes that methane leakage during the natural gas recovery process and subsequent gas processing and transmission is about 0.9% of methane consumed by the reformer. However, the U.S. Environmental Protection Agency (EPA) estimates leak rates across the natural gas supply chain at about 2%-3%. Methane, a key ingredient of natural gas, is described by the EPA as a “super pollutant” due to its higher potency than CO2 and responsibility for about one-third of global warming caused by human activities.

Efforts are already underway to reduce methane from oil and gas operations.

RELATED

US Lays Out Plan to Slash Methane from Oil and Gas at COP 28

“I think that you’re going to likely see blue hydrogen producers putting the onus on those upstream [natural gas] producers and transporters of natural gas to really look at those [emissions] closely and that can be done contractually,” Thompson said.

Meanwhile, two camps have emerged regarding the three pillars.

On one side, there’s the opinion that these requirements will make the 45V tax credit unattainable for blue hydrogen, pushing them out of the market, Thompson said. In the other, he added, some say the rules are so stringent on green hydrogen producers that there will be an influx of capital into blue hydrogen projects with the idea that developers can use the 45Q tax credit for carbon capture.

“So, where [do] things ultimately shake out? I can’t say,” Thompson said.

45V v 45Q

The IRA’s 45Q provides a tax credit for qualified carbon oxide captured. The tax credit is $17/metric ton for sequestered qualified carbon oxide, but the value jumps to $60 per ton for storage associated with enhanced oil recovery (EOR), $85 per ton for dedicated geologic storage, $130 per ton for direct air capture with carbon utilization and up to $180 per ton for direct air capture with carbon storage.

The 45V and 45Q credits cannot be stacked, meaning companies cannot claim both.

“In our view, it’s going to be very difficult to achieve a carbon intensity through a blue hydrogen project where going for 45V would be a better economic outcome than going for 45Q and carbon capture and storage,” Ian Nieboer, head of energy transition research for the Enverus Intelligence Group, told Hart.

Put simply: the 45Q has easier math than 45V, he said, with fewer strings attached.

With 45V, “getting that carbon intensity down really does rely on you having a very low carbon intensity feedstock,” Nieboer added. “It’s achievable with things like RNG and sort of negative CI [carbon intensity] feedstocks, but that’s also pretty scarce.”

Enverus sees blue hydrogen producers opting for 45Q given the economics.

In the interest of achieving climate goals, Thompson believes it may be wise for Congress to consider letting companies claim both the 45Q and 45V.

“Maybe there’s a world where you could get a reduced 45Q and a reduced 45V to help us push the industry along if ultimately clean hydrogen is what the United States wants to achieve,” he said. The investment tax credit is another option.

RELATED

CNX Resources Shifts Gears on Hydrogen Amid Uncertainty

Looking at the bigger picture, a company’s ability to get a tax credit may not necessarily make or break some projects, though it sweetens the economics for cleaner hydrogen.

Most of the hydrogen produced today is gray, or produced using natural gas as feedstock without carbon capture and storage.

Unanswered questions will give some blue hydrogen producers pause, Thompson said; however, whether they pursue 45V or 45Q will be project specific. It goes back to the three pillars, considering factors such as deliverability requirements, needed electricity, proximity to storage, distance to end markets and transportation options and associated costs.

“Companies are going to have to look very closely at how to balance all those competing interests,” Thompson said.

Proposed requirements

So far, more than 2,100 comments have been received on the proposed regulations.

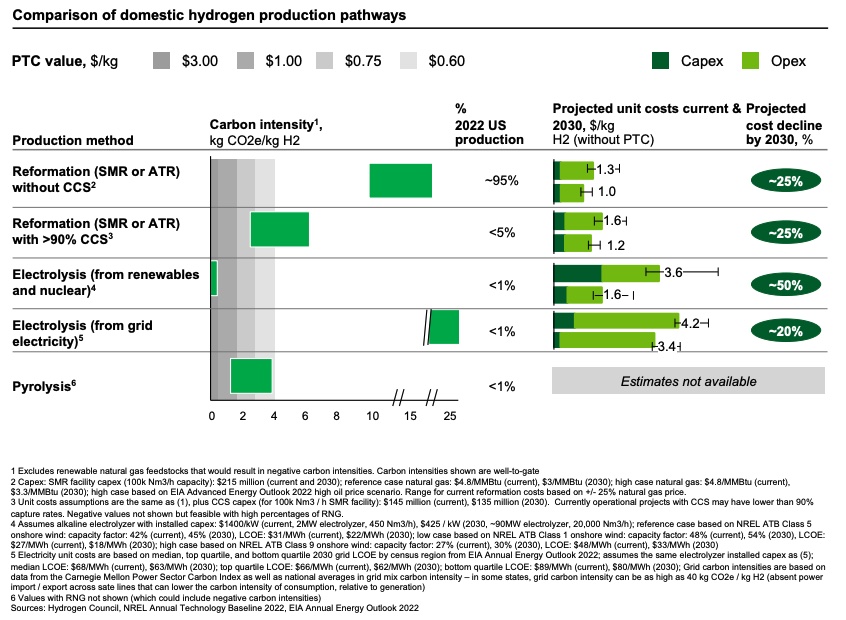

Hydrogen producers meeting a certain prevailing wage and registered apprenticeship requirements could qualify for a credit ranging from $0.60 per kilogram (kg) of hydrogen produced to $3/kg, depending on the lifecycle greenhouse gas emissions from hydrogen production, including its power source.

To capture the credit available for 10 years for facilities that start construction before 2033, hydrogen producers must have used electricity from a clean power facility built within three years of a hydrogen plant entering service; produce clean power from the same region as the hydrogen producer; and provide proof of purchase of clean power, which comes in the form of an energy attribute certificate that must be matched to production on an hourly basis.

The proposed requirements are considered the three pillars to building a clean hydrogen industry.

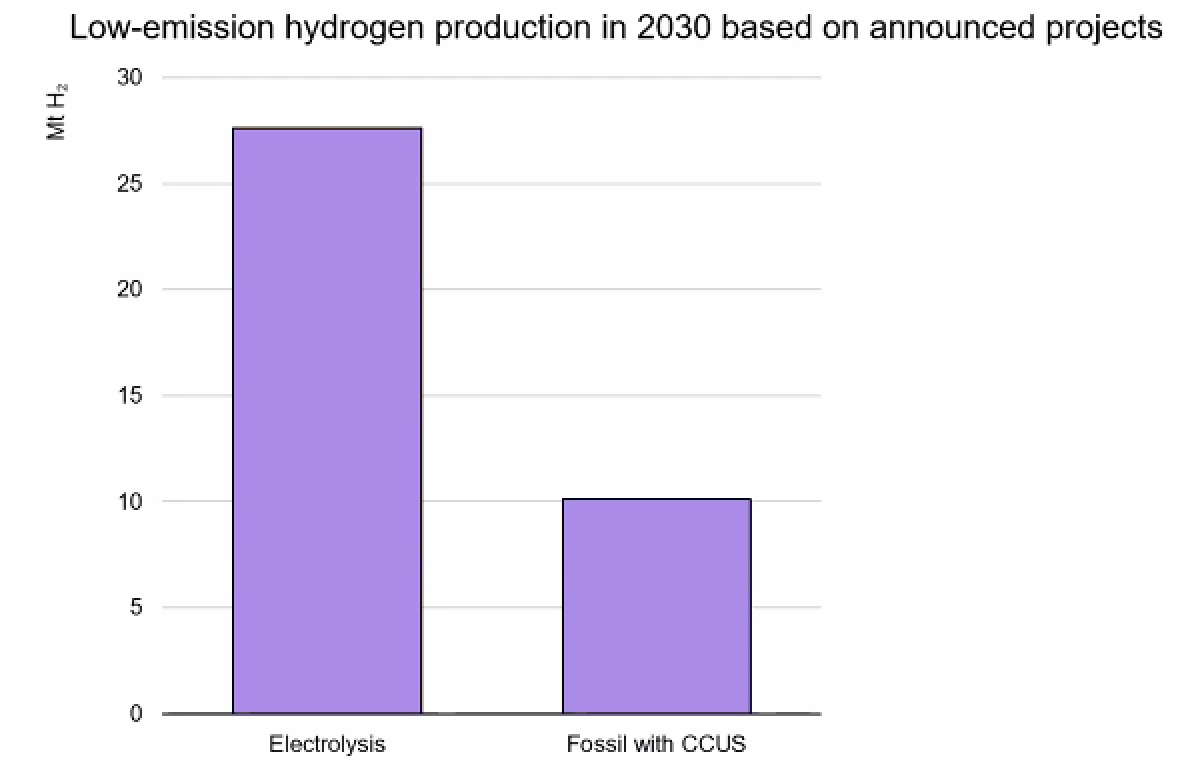

Globally, companies have announced projects that aim to produce a combined 38 million tons (MMton) of hydrogen—including 10 MMton of blue hydrogen—to meet government targets to produce 35 MMton by 2030, according to the International Energy Agency (IEA). However, only 4% of the announced projects have reached final investment decisions or are under construction.

That 4% accounts for 2 MMton, which is double that of 2021, José Miguel Bermúdez Menéndez, an energy technology analyst for the IEA, said during a recent GTI Energy webinar. “However, we cannot deny that this is slow progress in implementation,” Bermúdez added.

It’s a consequence of expected barriers such as new and complex value chains, demand uncertainty, lack of clarity in regulations and sluggish policy implementation.

Looking specifically at blue hydrogen, projects in North America account for about half of the announcements, Bermúdez said.

Recommended Reading

Ithaca Deal ‘Ticks All the Boxes,’ Eni’s CFO Says

2024-04-26 - Eni’s deal to acquire Ithaca Energy marks a “strategic move to significantly strengthen its presence” on the U.K. Continental Shelf and “ticks all of the boxes” for the Italian energy company.

Deep Well Services, CNX Launch JV AutoSep Technologies

2024-04-25 - AutoSep Technologies, a joint venture between Deep Well Services and CNX Resources, will provide automated conventional flowback operations to the oil and gas industry.

EQT Sees Clear Path to $5B in Potential Divestments

2024-04-24 - EQT Corp. executives said that an April deal with Equinor has been a catalyst for talks with potential buyers as the company looks to shed debt for its Equitrans Midstream acquisition.

Matador Hoards Dry Powder for Potential M&A, Adds Delaware Acreage

2024-04-24 - Delaware-focused E&P Matador Resources is growing oil production, expanding midstream capacity, keeping debt low and hunting for M&A opportunities.

Making Bank: Top 10 Oil and Gas Dealmakers in North America

2024-02-29 - MergerLinks ranks the key dealmakers behind the U.S. biggest M&A transactions of 2023.