Editor's note: This article originally appeared in the December 2019 issue of E&P as part of an LNG Special Report. Subscribe to the magazine here.

First mile and last mile are always the biggest challenges for any global supply chain, and the boom in North American LNG export terminals is no different. Having lived through several vertiginous recent expansions in unconventional production, the midstream sector has made some effort to get out in front of the multiple waves of liquefaction trains. In several cases that has been facilitated by the fact that midstream companies have been partners in the terminal projects. Gas supply and LNG offtake agreements have been diligent about specifying complete connections from field wellhead to vessel bulkhead. But just when it seemed safe to go back into the water, concerns of overbuilding have arisen.

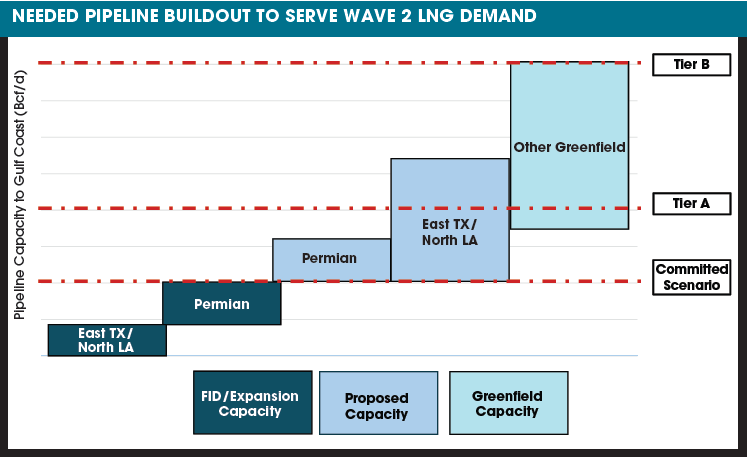

“We have an extreme propensity in U.S. markets to overbuild infrastructure,” said Anthony Scott, an analyst with BTU Analytics, during a conference call in September to discuss the energy consultancy’s “Getting to the Gulf—Can We Supply Wave 2 LNG?” report. “If you look at LNG imports as an example, many of the LNG export facilities exist today because they were LNG import facilities that were ultimately never utilized.”

The next wave of LNG demand, which the BTU analysts believe will last through 2030, will be much greater than it is now, especially with China and other Asian nations demanding more and more of the natural gas resource. The anticipation has brought about more investment projects for additional pipelines from natural gas producing basins like the Permian, Haynesville and Eagle Ford as well as export facilities around the Gulf Coast.

“As we think about building this Wave 2, it is not a guarantee that pipelines can be constructed, particularly if they need to go through an area where the regulatory environments have gotten more challenging,” Scott said. “Unfortunately, for most of these projects, they are all going to be interstate pipelines, unless you are going in the state of Texas and subject to the FERC review process. So that potentially adds significant delays and potential for cost overruns.”

“It seems like most of the proposed projects have adequate access to major supply lines,” said Charlie Palmer, managing director in process and technology practice at energy consultancy Opportune. “The local connections have either been installed, planned or are easy enough to get completed when the projects are funded. There may be situations where multiple assets have been proposed for one area that seem to exceed the available supply. In those situations, it is unlikely that all the projects reach FID [final investment decision] and actually get constructed.”

But perhaps the bigger risk is with contracting strategies for the large volumes of gas supply required for these large-scale plants. “While the physical supply may be available, are the necessary contracts in place for firm large supply volumes and firm pipeline capacity?” Palmer said. “Given the massive volumes required, too much exposure to the spot market could be extremely risky.”

Several terminal operators have plans for midsize liquefaction trains. Those could be seen as efficient additional capacity as markets ebb and flow; they could also be seen as pre-emptive, low-cost capacity to pre-empt other new entrants or large-train additions by existing operators.

While not handicapping the race to first loadings among the many competitors, Palmer noted that “as the cost of the midsize facilities comes down, those assets should have an economical advantage and competitive versus new grassroots investments. Also, having the ability to make use of existing fixed assets further lowers investment costs.”

That said, he was quick to add there is an important tactical focus for those midsize trains. “With the current market uncertainties around demand growth, these smaller assets allow them to move more quickly and nimbly to capture smaller-sized demand opportunities. The smaller investment and ability to quickly link to firm customer contracts should also increase the ease of funding. These factors reduce the risk, so it would likely be seen as an increased risk for new operators, thus effectively increasing their risk,” Palmer said.

An important milestone for the global LNG business took place in early September—1,000 miles from the Gulf Coast. CME Group, parent of the Chicago and New York mercantile exchanges, announced it would begin trading an LNG futures contract on Oct. 14 pending regulatory review.

CME claims first-mover status, asserting in a press release that its “U.S. LNG Export futures will be the first-ever physically delivered LNG contract. Participants will take delivery at Cheniere Energy’s Sabine Pass facility. The Freeport LNG terminal and additional facilities will be included in future delivery months. The new LNG futures contract expands CME Group’s suite of global natural gas futures and options and will complement the world’s leading gas benchmark, Henry Hub Natural

Gas futures.”

U.S. LNG Export futures will be available for trading on CME Globex, for submission for clearing through CME ClearPort, and will be listed with and subject to the rules and regulations of Nymex.

CME said it “worked very closely with commercial customers and industry participants.”

“This contract is structured to align with the complex logistics of the LNG markets, including a monthly physical settlement on the U.S. Gulf Coast,” said Peter Keavey, global head of energy, in the press release. “At a time when the United States is poised to become a significant source of freely traded LNG cargoes, we believe our LNG and Henry Hub Natural Gas futures will help the industry more effectively and efficiently manage price risk around the world.”

Notably, the CME contracts are for physical delivery. The Intercontinental Exchange already has a monthly cash-settled futures contract based on the Platts daily assessment price for the LNG Japan/Korea Marker. In March 2018, an online exchange called Redwood Markets announced plans to begin trading physical LNG.

Modular LNG

There are some efforts for small-scale LNG to reduce flaring in the Permian. LNG into New England as an end-run around pipeline problems in New York has been suggested, which would require U.S.-flagged ships.

“While this is not likely to be a major impact in the near-term, I think this is ripe for major opportunities in the midterm,” Palmer said. “As costs for small-scale facilities, both liquefaction and regasification, come down, local market economics can drive new investment opportunities previously inaccessible with the typical large-scale, multibillion dollar investments. Also, as local communities become more comfortable with these facilities, combined with the environmental benefits, new opportunities will emerge.”

There are many, niche-type market opportunities that could be solved by small-scale plants, Palmer added. “They could capture gas that is being flared in regions that lack adequate offtake capacity, such as the Permian, Bakken and Marcellus, that could increase value and avoid the environmental issues,” he said.

In New England small-scale LNG could in effect debottleneck constrained gas pipeline capacity. Liquefaction could provide increased storage and delivery capabilities to meet peaking capacity needs for power generation and local distribution.

By rail and road, “containerized shipments are becoming more available and economical,” Palmer said. “The current administration is also pursuing rulemaking to allow long-haul rail shipping of LNG.”

There is a growing market in export opportunities for small-scale LNG to the Caribbean and Central America for generation, both for peak shaving and baseload to replace high-emission fuel oil. Palmer noted that Jax LNG recently went into operation with a 15-MMcf/d facility. Jax LNG is a partnership of Pivotal LNG, a wholly owned subsidiary of Southern Company Gas, and NorthStar Midstream. The latter is backed by Oaktree Capital Management and Clean Marine Energy.

“The recent International Maritime Organization’s 2020 rule, which requires ships operating in international waters to reduce their sulfur emissions by more than 80%, creates a new market for LNG demand as the availability of LNG to more ports increases,” Palmer said. “For example, Carnival Cruise Line is investing in two LNG-fueled vessels. Shell has recently stated they expect the maritime market for LNG bunkers would reach 25 million metric tons by 2035.”

Beginning in late 2017 with a single International Organization for Standardization (ISO) container, FortisBC has made three shipments of LNG to China, according to a report by the Western Energy Institute. The trade has grown: A shipment late last year to Shanghai by China Energy Reserve and Chemicals Group comprised 19 ISO containers with more than 300 MMmt of LNG.

According to the institute, “LNG in an ISO container will remain in liquid form for as long as two and a half months without any additional cooling, and it can be easily transported without either import terminals or pipeline networks. In 2017, 19 million metric tons of LNG were transported through China by a fleet of approximately 10,000 road tankers.”

A few companies are trying to do the same type of thing on a local and regional scale in the U.S. Edge Gathering is one of them. It operates trailer-mounted Cryobox liquefaction units with throughput of 1,000 cf/d. The first commercial unit went into service in the Marcellus in May, shipping LNG to a customer in New England.

Edge Gathering is a joint venture (JV) of three large international firms: Galileo Technologies, based in Buenos Aires, provides the Cryobox and Virtual Pipeline technologies. Blue Water Energy is a specialist international private-equity firm focused on the energy sector, with more than $2.5 billion under management. NextEra Energy Marketing handles sales and marketing, and it is a subsidiary of Next-Era Energy, which claims primacy as “the world’s largest utility company.”

The output is warm LNG, said Edge Gathering CEO Mark Casaday, with a Btu range of 1,020 to 1,035 per metric cubic feet, as compared to 1,010 to 1,020 per metric cubic feet for cold LNG from the massive coastal liquefaction trains. “Permian flared gas is high-Btu gas, so for that we would use three units: an NGL stabilization unit that would take full wellhead gas at 1,200 Btu or more and cut out the C3s and higher,” he said. “Those can be sold or sent back to the producer. Then there is a pretreating unit to remove CO2 before liquefaction.”

Casaday stresses the plug-and-play simplicity. “This is not new technology; it’s just been miniaturized and made portable. We load into standard intermodal ISO tanks at pressures of about 40 to 45 psi. They can sit on average for 30 days and go anywhere by truck or train. There is no boil off.”

Even though the components are standard, the margins are surprising. “The economics of LNG from gas that would otherwise be flared crushes the economics of diesel for in-basin fuel,” Casaday said. “It creates its own market. Producers capture the differential.”

Not surprisingly, the first big installation for Edge Gathering is being developed in the Bakken, which has taken the lead over the Permian in moving to regulate and limit flaring. “We are completing a toll arrangement in the Bakken, putting cryo clusters at every well pad,” Casaday said. “The producer can use the LNG for enhanced oil recovery, for power generation or as fuel for pumps and equipment.”

The West is yet to come

No news is good news for the first of several LNG projects slated for the Canadian West Coast. Since the FID was made in October 2018, the Royal Dutch Shell LNG project in Kitimat, British Columbia, has proceeded uneventfully through the early stages of long-lead commissioning and site preparation. Soon after the Shell decision, TransCanada said it would proceed with construction of the Coastal GasLink pipeline project to the terminal. Petronas, PetroChina, Kogas and Mitsubishi are involved in the project as well.

While Canadian LNG is not bad news per se for Gulf Coast terminals, it certainly becomes another variable in the equation. Shell is not only among the elder statesmen of the global majors, it is also one of the largest energy trading houses. Another global major, Chevron, leads the other well-advanced project for British Columbia. In addition, there are at least two other substantive plans and a host of others. As with the gaggle of Gulf Coast terminals, some will fall by the wayside. But there is little doubt that a third coast will open for North American LNG exports.

Shell’s CA$40 billion project, slated for 14 million tonnes per annum (mtpa), goes by the simple name “LNG Canada.” It will be several days’ sailing closer to major markets in Japan, Korea and China, which will save time, costs and possible delays for shipments through the Panama Canal.

The proposed “Kitimat LNG” project is a 50:50 JV between Chevron and Australian firm Woodside Energy, and it is planned to comprise three LNG trains totaling 18 mtpa. The design calls for an all-electric plant powered by hydroelectricity from BC Hydro. The FID has not been made.

Chevron and Woodside collectively operate approximately 15% of global LNG production in 12 LNG trains and loaded more than 500 cargoes in 2018. The partners stress that they have “established First Nations partnerships that are unique in the Canadian energy industry and have received strong support from local indigenous communities across the entire value chain.”

There have been several LNG terminals proposed for the U.S. West Coast, of which Jordan Cove is the last project standing. “A lot of other projects came and went due to a host of issues … whether it was cost, regulatory issues or First Nations issues,” said Scott Atha, senior manager for marketing responsible for LNG at Pembina Pipeline Corp. “When we get this project permitted, we truly believe we’ll be the only project that ever gets built on the West Coast of the U.S.”

Separately, Pembina is in the process of buying Kinder Morgan’s Canadian operations for about $4 billion.

The liquefaction plant at Coos Bay, 200 miles southwest of Portland, Ore., is planned for a capacity of 7.5 mtpa in five trains using the Black & Veatch Prico process. “It is a smaller, modular train design,” Atha said. “That allows a lower cost structure and a high degree of utilization. A lot of the projects in the Gulf Coast are shifting to the smaller train design with more units.”

Pembina hopes to have final certificate decision from the Federal Energy Regulatory Commission (FERC) in February 2020. In the meantime, the company has detailed publicly that it has 11 MMmt of nonbinding agreements with customers. “We are actively trying to convert those agreements into binding tolling agreement,” Atha said.

LNG Project Profiles >>>

The following are overviews of LNG projects in various stages. These summaries include profiles of the main terminals already delivering LNG or soon to do so, followed by reports on plants under construction.

Terminals Set to Deliver LNG

Cheniere Energy: Corpus Christi

Early in June 2019, Cheniere Energy secured a long-term gas supply agreement with Apache Corp. under which Apache will sell 140,000 MMBtu/d of gas to Corpus Christi Stage III for about 15 years. The LNG produced from that gas supply, about 0.85 mtpa, will be marketed by Cheniere. Apache will receive an LNG price, net of a fixed liquefaction fee and certain costs incurred by Cheniere, based on international LNG indices.

“This first-of-its-kind long-term agreement with Apache represents a commercial evolution in the U.S. LNG industry,” said Jack Fusco, Cheniere’s president and CEO. “It will ensure the continued reliable delivery of gas to Cheniere from one of the premier producers in the Permian Basin, while enabling Apache to access global LNG pricing and receive fl ow assurance for its gas.”

The Corpus Christi Stage III project is being developed to include up to seven midscale liquefaction trains with a total expected nominal production capacity of approximately 9.5 mtpa. Corpus Christi Stage III received a positive environmental assessment from the FERC in March 2019 and is expected to receive all remaining necessary regulatory approvals for the project by the end of the year.

Three months after the Apache deal, Cheniere said its Corpus Christi Liquefaction (CCL) subsidiaries secured long-term gas supply agreements from EOG Resources. The initial arrangement is similar to the Apache arrangement in that it will run for about 15 years beginning in early 2020, with the quantity starting at 140,000 MMBtu/d. The volumes will then increase to 440,000 MMBtu/d.

The LNG produced with the first 140,000 MMBtu/d of gas will be owned and marketed by Cheniere. EOG will receive a price based on the Platts Japan Korea Marker for that. The remaining 300,000 MMBtu/d will be sold by EOG to Cheniere at a price indexed to Henry Hub.

The split-price gas-supply agreement with EOG came just weeks after Cheniere announced “substantial completion” of the second liquefaction train at Corpus Christi was achieved on Aug. 28. Commissioning has been completed and Cheniere’s engineering, procurement and construction (EPC) contractor, Bechtel Oil, Gas and Chemicals, handed over the keys. The occurrence passed without much fanfare because it was the seventh such event between Cheniere’s two terminals, Corpus Christi and Sabine Pass.

Under sale and purchase agreements with Électricité de France, Iberdrola, Naturgy Energy Group, PT Pertamina and Woodside Energy Trading Singapore, the date of first commercial delivery is expected to occur in May 2020.

The first train at Corpus Christi began operations in 2018. Train 2 is expected to be fully operational by the end of 2019. Train 3 is expected to be fully operational in 2021. When all three trains are completed, the aggregate nominal production capacity at the Corpus complex is expected to be 13.5 mtpa of LNG. It bears mentioning that this export terminal at one of Cheniere’s existing sites was previously permitted for an import regasification terminal.

Upon completion of Train 2 at Corpus, Bechtel noted that “since the first notice to proceed was announced in August 2012, [we] have completed a total of seven LNG trains for Cheniere in seven years at Sabine Pass and Corpus Christi. Bechtel-delivered facilities account for roughly one-third of the global LNG capacity, supplying about 66 mtpa, or enough energy to power more than 85 million homes.”

Bechtel is designing and building three LNG trains and related facilities at Corpus. The engineering firm noted that Corpus is the first greenfield LNG export facility in the U.S. in nearly 50 years.

In addition to the three liquefaction trains, Bechtel also is building three LNG storage tanks with capacity of more than 10 Bcfe and two berths that can accommodate vessels with capacity of up to 267,000 cu. m.

Construction of the complex is taking place over two stages. Stage I included two LNG trains, two tanks, one complete berth and a second partial berth. Train 1 celebrated its first production of LNG from the facility on Nov. 15, 2018, and Train 2 reached substantial completion in August 2019. Stage II covered one LNG train, one additional tank and completion of the second berth. Stage III received full notice to proceed in June 2018.

The trains use the ConocoPhillips Optimized Cascade process, a well-established technology deployed in numerous LNG projects around the world. The process uses three refrigeration phases involving propane, ethylene and methane to progressively cool the natural gas.

Inbound, Cheniere said “CCL is fully contracted with transportation capacity to meet the full requirements of the terminal. CCL has purchased over 50% of its baseload natural gas needs for Trains 1-3 for the next few years.”

The company’s own 23-mile, 48-in. pipeline connects the complex plant to several interstate and intrastate pipelines. Through a midstream subsidiary, Cheniere plans to build bidirectional interstate lines to deliver feed gas to the Stage III expansion, LNG Facilities. The Stage III pipe system would include a new 21-mile-long, 42-in.-diameter line that would run parallel to a 48-in.-diameter line already approved.

In addition, Cheniere has transport capacity on third-party pipelines under long-term agreements. Natural gas supply is purchased from producers and marketers on a short- and long-term basis to form a balanced portfolio of natural gas feedstock.

Outbound, more than 10 mtpa from Corpus Christi Trains 1 through 3 has been contracted to long-term third-party customers, including Pertamina, Endesa, Iberdrola, Naturgy, Woodside, EDF, EDP, Trafigura and PetroChina. As with Sabine Pass, excess capacity not sold under long-term contract is sold into the global spot market.

In addition to the main three units, Cheniere plans to build as many as seven midscale liquefaction trains and an LNG storage tank adjacent, together called Stage III. The concept allows phased construction in response to market demand that would produce up to 11.45 mtpa upon completion of the seventh train.

Cheniere Energy: Sabine Pass

Cheniere Energy claims primacy as “the leading producer of LNG in the United States” and is expected to be a top 5 global provider of LNG by 2020, as stated on the company’s website. There is no dispute that it was the first, with its initial shipment in February 2016. Since startup, nearly 700 cumulative cargoes of LNG originating from Cheniere have been delivered to 32 destinations.

According to its website, Cheniere is operating, constructing and developing two LNG facilities on the U.S. Gulf Coast. Cheniere’s Sabine Pass terminal is in Cameron Parish in southwest Louisiana. It has five fully operational liquefaction trains. A sixth train has all necessary permits and reached FID in June 2019. When that sixth and last train goes into commercial operations, the aggregate nominal production capacity of the Sabine Pass complex is expected to be about 27 mtpa of LNG, the company reported.

Cheniere asserts that Sabine Pass Liquefaction (SPL), a subsidiary of Cheniere Partners, “is fully contracted with transportation capacity to meet the full requirements of the terminal. SPL has purchased over 50% of its baseload natural gas needs for Trains 1-6 for the next few years.”

The 1,000-acre Sabine Pass site was chosen to provide LNG for its expansive area, proximity to prolific unconventional gas plays in Louisiana and Texas, interconnections with multiple interstate and intrastate pipeline systems, and marine access less than 4 miles from the Gulf Coast.

Natural gas liquefaction is an exemplar for economies of scale, or as Cheniere calls it, “expansion economics.” The Sabine Pass terminal has access to existing infrastructure, including five storage tanks and two berths, as well as Cheniere Partner’s 94-mile Creole Trail Pipeline, which was reconfigured to reverse the flow of gas, making it a bidirectional pipeline. Eventually the Corpus Christi complex will enjoy similar advantages.

More than 20 mtpa from Sabine Pass Trains 1 through 6 has been contracted to long-term third-party customers, including Shell, Naturgy, Kogas, Gail, Total, Centrica, Petronas and Vitol.

Dominion Energy: Cove Point

“Cove Point came into commercial service in April 2018 for liquefaction so it has about a year and a half of operations,” said Paul Ruppert, president of Gas Transmission and Storage, in the gas infrastructure group at Dominion Energy. “Liquefaction terminals are extremely complex facilities, and we consider it a significant milestone to get through the early operations so smoothly. The facility is in its second annual scheduled outage for maintenance, and everything is on schedule. We are very pleased with the work of IHI Kiewit, our EPC contractor and also with the Air Products C3MR technology.”

Cove Point is a toll facility. Dominion’s customers arrange for their molecules to arrive by pipe and leave by ship. Regulatory filings indicate 85 ships loaded through July 2019. The facility was first built as a regas terminal for imports and still sees some inbound cargoes. It was reactivated for regas in 2003, and some customers have 20-year contracts.

In getting gas to the cold box, Dominion itself as well as Transco and TransCanada have large pipelines. The terminal is in Lusby, Md., just south of Baltimore, thus very close to the Marcellus Shale.

“On the East Coast, we are farther from Asia than the facilities on the Gulf Coast, but we are also closer to Europe. We also get fewer hurricanes, and we’re sheltered from those that do come up the coast by the Chesapeake Bay,” Ruppert said.

Another contrast to several of the terminals on the Gulf Coast is that those tend to be centrally isolated on huge landholdings. Cove Point is “a little constrained on real estate,” Ruppert said, “but it is a robust facility, and we are highly focused on optimization.”

Cove Point has a nameplate liquefaction capacity of 5.25 mtpa, equivalent to approximately 8.3 MMgal/d of LNG. Behind that is storage capacity of 14.6 Bcf and a daily send-out capacity of 1.8 Bcf. The terminal connects, via its own pipeline, to the major Mid-Atlantic gas transmission systems of Transcontinental Gas Pipeline, Columbia Gas Transmission and Dominion Energy Transmission.

Officially, Dominion produces LNG for ST Cove Point, which is the JV of Sumitomo Corp. and Tokyo Gas, and for GAIL Global (USA) LNG, the U.S. affiliate of GAIL (India), under 20-year take-or-pay contracts.

In the 1970s Cove Point was built by Consolidated Natural Gas, parent of what is now Dominion Energy Transmission, for LNG imports in a venture with the Columbia Gas System. In a roundabout series of transactions, Consolidated sold its interest in the terminal and the Cove Point pipeline to Columbia in 1988, then Williams purchased Cove Point from Columbia in 2000 only to sell it ultimately back to Dominion Energy two years later.

Cove Point received its first LNG shipment associated with import reactivation in the summer of 2003 when the unconventional development that would transform global oil and gas markets was just getting rolling. Eleven years later Dominion began construction of the liquefaction facilities. With a cost of about $4 billion, that initiative was the largest construction project ever for the company and in the state of Maryland.

While the export market figures large for Cove Point, another growing market for LNG is much closer: surrounding and adjacent states. “There are severe infrastructure constraints in the Northeast as well as other parts of the country,” Ruppert said. “We see significant opportunities for modular LNG in the domestic market.”

Dominion will soon complete construction on a modular LNG project in north central Pennsylvania, a JV with Rev LNG called NiCHe LNG.

“It will be modular LNG loaded into intermodal tank containers,” Ruppert added. “Those can be delivered to industrial or commercial users, or to an interconnect with an existing distribution system to create a virtual pipeline around geographic constraints.”

Towanda, in Bradford County, Pa., is on about four acres adjacent to the Howard Energy Compressor Station that is part of the gathering system supplying gas. Chart Inc. supplied a nitrogen-expander liquefaction system rated at 50,000 gal/d. The modular LNG facility also has gas pretreatment, a truckloading rack and three 60,000-gal LNG storage tanks.

There are two main objectives in the modular LNG market, Ruppert explained. “There are still residential, industrial and power generation customers that are relying on higher-carbon fuels, such as fuel and heating oil. Some of that is because the region is so constrained on pipeline infrastructure. Modular LNG is both a way around those constraints and also a way for generators and other energy users to switch from higher carbon fuels,” he said.

Dominion Energy is one of the nation’s largest producers and transporters of energy, with a portfolio of about 26,000 MW of electric generation; 14,800 miles of natural gas transmission, gathering and storage pipeline; and 6,600 miles of electric transmission lines.

Freeport LNG

Freeport LNG was formed in 2002. The terminal started LNG import operations in June 2008. Liquefaction for export is being accomplished by “the largest fully electric motor drive natural gas liquefaction plant in the world,” the company stated, “reducing emissions at the facility by over 90% relative to other plants that use combustion turbines.”

Zachry Group, along with its partners McDermott International and Chiyoda International, announced late in July 2019 that Train 1 of the Freeport LNG Liquefaction project on Quintana Island in Freeport, Texas, has reached the final commissioning stage. That included the introduction of feed gas. The project includes three pretreatment trains, a liquefaction facility with three trains, a second loading berth and a 165,000-cu.-m LNG storage tank.

On Sept. 3, Freeport LNG shipped the first LNG commissioning cargo from its liquefaction facility. Approximately 150,000 cu. m of LNG were loaded aboard the LNG Jurojin. “We are very pleased that it took less than 45 days to load our first cargo since gas was introduced to liquefaction,” said Michael Smith, founder, chairman and CEO at Freeport LNG.

Freeport LNG’s limited partnership interests are ultimately held by Smith, Global Infrastructure Partners and Osaka Gas. Train 2 is advancing precommissioning to support an in-service date of January 2020. Train 3 is nearing completion to support an in-service date of May 2020.

Total Holdings has joined the list of Freeport LNG’s list of customers. Total said it had completed its purchase of Toshiba’s LNG portfolio, including its 20-year, 2.2-mtpa tolling agreement with Freeport LNG. That tolling agreement will begin with the commercial operation of Freeport’s third liquefaction train. With the first shipment, Freeport became the sixth largest U.S. liquefaction facility.

In reporting the start of the first train, Reuters noted that the new capacity is expected to add to a supply glut, which has been weighing on spot LNG prices in Asia.

“The startup of Freeport LNG contributes to even more supply growth at a time when the market is already oversupplied,” said Edmund Siau, an LNG analyst with FGE. “Winter is just around the corner and seasonal demand will help to absorb this new supply; however, we see a key risk posed by European gas inventories that are already above 90% full.”

Under three-train operations, Freeport’s facility will rank seventh in current global liquefaction production capacity, with the facility rising to the world’s fifth largest producer once Train 4 is completed. Train 4 operations are anticipated to commence in 2023.

Also in early September, Freeport signed a 20-year liquefaction tolling agreement with Sumitomo Corp. of Americas for 2.2 mtpa of LNG. The deal made Sumitomo Freeport’s first customer for Train 4.

“Sumitomo’s significant U.S. gas trading and LNG operations make it an especially great addition to our existing customers,” Smith said. The tolling agreement “is a major step toward Freeport LNG contracting the approximately 3.5 mtpa needed for financing and commencing construction of Train 4.”

After Total and Sumitomo came on board in September and the first cargo left the dock, Freeport secured a $1.025 billion mezzanine loan from Westbourne Capital to support a proposed 5-mtpa fourth liquefaction train. That loan follows Freeport obtaining FERC and U.S. Department of Energy (DOE) authorizations for the Train 4 project. With those approvals in hand, Freeport signed a fixed-price contract with KBR for Train 4. The contract is expansive, including EPC, commissioning, startup and the associated gas pretreatment plant.

Aggregate export capability of the four-train facility would rise to more than 20 mtpa once Train 4 is in service. About 13.5 mtpa of this capacity has been contracted under 20-year tolling agreements to Osaka Gas Trading & Export, JERA Energy America, BP, Toshiba and SK E&S LNG. A further half million metric tons per year have been contracted to the big trading house Trafigura under a three-year sale-and-purchase agreement starting in 2020.

In addition to conventional long-term contracts, Freeport also is exploring some innovative sales approaches. In the middle of a very busy September, Freeport said it would start a “virtual private storefront” for selling LNG via the Redwood Marketplace in November. That is an online commodity-trading platform that enables buyers and sellers of physical LNG to negotiate and confirm commercial terms.

Unlike bilateral sales, the platform also provides “efficiency, standardization and price discovery to the global community of LNG stakeholders,” Freeport said in a press release. As the host of its private “storefront,” Freeport can negotiate and match physical, bilateral LNG transactions with potential LNG buyers in a variety of online trading formats with multiple options for transparency.

“The number of participants in the global LNG market has increased substantially over the last decade,” said Hugh Urbantke, executive vice president and chief commercial officer at Freeport LNG, in a statement. “The storefront will streamline interactions. It will also allow us to provide counterparties direct access to spot cargoes efficiently and transparently.”

Kinder Morgan: Elba Island

Elba Island was originally built in 1972 by Southern Natural Gas (Sonat) to import LNG. Imports ceased in 1980. In 1999 Sonat was acquired by El Paso Corp. In turn El Paso was acquired by Kinder Morgan in 2012.

Early in October 2019, the second LNG export terminal on the U.S. East Coast came into service. The Elba Liquefaction Co. (ELC), a JV between Kinder Morgan and EIG Global Energy Partners (EIG), confirmed commercial service of the first of what are intended to be 10 liquefaction units of the $2 billion project. Previously only an import terminal, Elba Island is now able to do both. The facility is just outside Savannah, Ga.

Progress at Elba Island is also being made on the remaining nine units. Startup activities are underway on the second and third units, the commissioning of units four through six is ongoing and construction on the remaining units is largely complete. “Under full development, the Elba Liquefaction Project is expected to have a total capacity of approximately 2.5 million tonnes per year of LNG for export, which is equivalent to approximately 350,000 Mcf per day of natural gas,” Kinder Morgan reported on its website.

Kinder Morgan owns 51% of ELC, with EIG holding the rest. In turn, ELC owns the liquefaction units and other ancillary equipment. Other facilities associated with the project are wholly owned by Kinder Morgan. The project is supported by a 20-year contract with Shell, which provides all the inbound gas and takes all the LNG.

In contrast to standard projects—gathering and processing that are done in collaboration with producers, or long-haul transport lines funded internally—midstream companies like Kinder Morgan have found few capital or regulatory hurdles in connecting their systems to planned liquefaction complexes. The sheer size of the projects means gas-supply infrastructure amounts to little more than a rounding error in the overall budget. Similarly, permits are rarely a complication because the terminals have so far been built in areas with heavy petrochemical and midstream infrastructure in place.

EIG is an institutional investor in global energy with $23.3 billion under management. For more than 37 years, the firm has committed almost $31 billion to the energy sector through more than 350 projects or companies in 36 countries on six continents. EIG’s clients include many pension plans, insurance companies, endowments, foundations and sovereign wealth funds in the U.S., Europe and Asia.

In reporting the first train in operation at Elba Island, Reuters noted that the start is a year after it had been originally due to begin operations. The facility has experienced startup problems that led to delays since late 2018 as it tweaked the setup of its 10 trains.

While Elba Island is not the only LNG facility to use many smaller trains rather than a few massive liquefaction units, it is the only facility to use the modular approach as its IP. Others, such as Cheniere’s Corpus Christi terminal, have multiple smaller units planned as flexible peaking capacity beyond a baseload liquefaction from a few large trains. Each of the Kinder Morgan trains has a nameplate capacity of 300,000 tonnes per annum (tpa) compared to about 5 mtpa for other U.S. trains.

The process is Shell’s Movable Modular Liquefaction System. There are two small ironies in that. One is that the concept of the modular technology is quicker fabrication, transport and installation as compared to the massive multibillion-dollar full-scale trains. The other irony is that Shell is an investor in several LNG terminals, as well gas supplier and LNG taker from still others that do not use the technology. It has been noted that the technology is well-established worldwide, but Elba Island is the first deployment in the U.S.

Sempra Energy: Cameron

In June 2019, Reuters reported that the first LNG cargo to be shipped from Sempra Energy’s $10 billion Cameron export terminal in Louisiana was headed to France. Mitsui & Co., one of the partners in the Cameron project, chartered the tanker Marvel Crane.

Reuters reported, “Japanese stakeholders of the project were initially expected to import the cargoes to meet domestic demand, but weak spot prices in Asia mean that it is not economically viable to ship cargoes from the U.S. to Asia, traders said.”

Nevertheless, the ease with which the cargo was diverted into commerce shows how liquid the deepsea LNG market has become.

In August 2019, Sempra Energy stated that its share of full-year run-rate earnings from its first three LNG trains at Cameron Parish, La., are projected to be between $400 million and $450 million annually.

Train 1 is part of Phase 1 of the Cameron LNG project that includes a projected export capacity of 12 mtpa of LNG, or approximately 1.7 Bcf/d of natural gas. Cameron LNG is jointly owned by Sempra, Total, Mitsui & Co. and Japan LNG Investment, which is jointly owned by Mitsubishi Corp. and Nippon Yusen Kabushiki Kaisha. Sempra Energy indirectly owns 50.2% of Cameron LNG.

Cameron LNG Phase 1 is one of five LNG export projects that Sempra Energy is developing in North America: Cameron LNG Phase 2, previously authorized by the FERC, encompasses up to two additional liquefaction trains and up to two additional LNG storage tanks; Port Arthur LNG in Texas; and Energía Costa Azul LNG Phase 1 and Phase 2 in Mexico.

In May 2019, Sempra and Saudi Aramco reported their respective subsidiaries, Sempra LNG and Aramco Services Co., announced their intention to make final a 20-year purchase agreement for 5 mtpa of LNG from Port Arthur Phase 1. The intention is to negotiate a 25% equity investment in Phase 1.

“Since the initial award in 2014, McDermott and its joint venture partner on the project, Chiyoda, have provided the engineering, procurement and construction for the Cameron LNG project,” according to a May 14 McDermott press release. “Once Train 1 is at full production and we have completed Trains 2 and 3, this facility will be one of the largest producers and exporters of LNG to markets around the world,” said Mark Coscio, McDermott’s senior vice president for North, Central and South America, in the release.

As if to confirm the international reach of North American LNG exports, another tanker, Shinshu Maru, called at Cameron a week after the first shipment in June to load another cargo. “Shipping market sources said it was chartered by Spain’s Repsol from Russia’s Novatek and could deliver a Cameron cargo to Spain where LNG imports have been growing since May on lower hydro generation,” a Reuters report stated.

In January 2019, Sempra’s Port Arthur terminal along with two associated pipelines obtained their final environmental impact statement from the FERC. The company plans a liquefaction terminal in Jefferson County, Texas, as well as the Texas and Louisiana connector pipelines that will deliver gas to the new export facility.

The proposed Port Arthur project is expected to include two natural gas liquefaction trains capable of processing approximately 11 mtpa of LNG as well as three LNG storage tanks and associated facilities including the new gas-transmission lines. The environmental impact statement is the final step in the review process before the FERC can issue an order approving the project.

Sempra selected Bechtel as the EPC and commissioning contractor for the project. In June 2017, Korea Gas Corp. signed a memorandum of understanding for potential participation in the Port Arthur project.

Sempra and its subsidiary in Mexico, IEnova, plan to add liquefaction facilities to the existing Energía Costa Azul regasification terminal on the Pacific in Baja California. Energía Costa Azul’s existing facilities include one marine berth and breakwater, two LNG tanks of 160,000 cu. m each, LNG vaporizers, nitrogen injection systems and pipeline interconnections. “The liquefaction project would add natural gas receipt, treatment and liquefaction capabilities and loading of LNG cargoes,” according to Energía Costa Azul. The company anticipates adding more liquefaction capability.

Sempra has received two authorizations from the U.S. DOE to export U.S. produced gas to Mexico and to re-export LNG to countries that do not have a free-trade agreement with the U.S.

The DOE authorizations allow the export of 636 Bcf/year of U.S. gas. Phase 2 of the project will require additional DOE approval to export its full expected capacity.

With the Costa Azul project, all three North America Free Trade Agreement nations have proposed LNG export terminals on their west coasts. The farthest advanced is by Shell and partners in Kitimat, British Columbia. Energía Costa Azul LNG Phase 1 is to be a single train. It is expected to use current LNG storage tanks, marine berth and associated facilities. Phase 2 is projected to include the addition of two trains and one LNG storage tank.

Plants under Construction

Calcasieu Pass

In August 2019, Venture Global announced the FID and the closing of the project financing for its Calcasieu Pass LNG project as well as associated TransCameron pipeline in Cameron Parish, La. The project has 20-year LNG sale and purchase agreements with Royal Dutch Shell, BP, Edison SpA., Galp, Repsol and PGNiG.

Stonepeak Infrastructure Partners provided a $1.3 billion equity investment for the project. The debt and equity financing fully fund the balance of the construction and commissioning of Calcasieu Pass. Full site construction has been underway since February, and the project is expected to reach its commercial operations date in 2022.

EnLink has an agreement to provide gas to Calcasieu Pass. The midstream company expects to spend $20 million on the project during 2020 and have it operational in 2021.

Venture has a turnkey EPC contract with Kiewit. Baker Hughes was awarded a contract to provide a proprietary liquefaction train system with 18 modularized compression trains across nine blocks, for a total nameplate capacity of 10 mtpa. Venture Global also is developing the 20-mtpa Plaquemines LNG project and the 20-mtpa Delta LNG project, both in Plaquemines Parish, La. Under the master equipment supply agreement, Baker Hughes could ultimately supply liquefaction equipment to Venture for as much as 60 mtpa LNG capacity. Equipment deliveries are expected to begin in the second half of 2020. Chart Industries is providing cold boxes and brazed aluminum heat exchangers for Calcasieu Pass.

The modular liquefaction approach at Calcasieu Pass will be like the Kinder Morgan Elba Island terminal and a portion of the Cheniere Corpus Christi complex. The modularized system is supposed to be a plug-and-play approach that enables faster installation and lower construction and operational costs. These modules will be manufactured, assembled, tested and transported from Baker Hughes’ fabrication facilities in Italy.

Golden Pass

In February 2019, Zachry Group and its partners, Chiyoda International and McDermott International, were awarded an EPC contract by Golden Pass Products, a JV of Qatar Petroleum and Exxon Mobil affiliates, to build an LNG export terminal in Sabine, Texas. The complex is to have three big liquefaction trains each with capacity of about 5.2 mtpa. Combined output will be close to 16 mtpa. The facility is expected to be operational in 2024.

Golden Pass has a 20-year firm transportation agreement with Enable Midstream Partners to supply gas. Golden Pass has also secured pipeline capacity on Kinder Morgan’s NGPL line. As with several other new liquefaction projects, Golden Pass is adding those capabilities to its existing import facility in Sabine Pass. And with Dominion, Golden Pass will retain regas capabilities to provide the flexibility to import and export natural gas in response to market conditions.

The current Golden Pass LNG terminal facilities include five 155,000-cu.-m LNG storage tanks, two marine berths capable of offloading various-sized ocean-going LNG carriers and process facilities capable of regasifying LNG to produce approximately 2 Bscf/d of natural gas. The new $10 billion facility will use the existing tanks, berths and pipeline infrastructure. New facilities for gas pretreatment and liquefaction will be built.

Pipeline upgrades will include installation of approximately 3 miles of 24-in. pipeline to facilitate bi-directional flow capability and improve system hydraulics. Installation of additional compressor stations will facilitate the receipt and redelivery of up to 2.6 Bcf/d of natural gas supply to the export facility.

Magnolia

Late in September 2019, Australia’s Liquefied Natural Gas Ltd. received preliminary FERC approval to increase liquefaction capacity at its proposed Magnolia LNG complex by 10%, from 8 mtpa to 8.8 mtpa. The four-train project is to be built adjacent to an existing LNG regas terminal in the Port of Lake Charles, La. According to the company’s website, the “project is construction ready with all permitting, design, contracting and equity arrangements in place to enable construction to start immediately upon finalization of LNG offtake agreements.”

Full project equity, up to $1.5 billion, has been arranged through Stonepeak Infrastructure Partners. Limited-equity participation is being offered to offtake parties. A consortium of lenders will provide the debt at about three times equity.

Design work is complete with the front-end engineering executed by contractor KBR, working with SK E&C USA. Ammonia and mixed-refrigerant compressors along with associated equipment for the first two trains have been prepurchased from Siemens. The liquefaction cold boxes and brazed aluminum heat exchangers for the first two trains have been prepurchased from Chart Industries.

Gas will come from the existing Kinder Morgan Louisiana Pipeline. The interconnect agreement stipulates 1.4 Bcf/d for 20 years. It was signed in January 2015.

The project site covers an area of 115 acres opposite to the existing Trunkline LNG import terminal operated by Southern Union. The project will involve the construction of four 2.2-mtpa liquefaction trains, installation of two 180,000-cu.-m cryogenic tanks and construction of a berth jetty for tankers with capacity of up to 170,000 cu. m.

A variety of gas tolling agreements has been signed with different customers since 2013. One was with Brightshore Overseas, an affiliate of Gunvor Group, for 1.7 mtpa plus another 300,000 tpa of interruptible capacity for 20 years, extendable by five years. Another agreement was signed with Gas Natural Fenosa for up to 1.7 mtpa. A term-sheet agreement was signed with West Face Capital Group for 1.7 mtpa and another was signed with AES Corp. Group for between 800,000 tpa and 1 mtpa.

Jacksonville Eagle

Late in September 2019, Eagle LNG Partners said the FERC issued authorization for its proposed on-water LNG facility in Jacksonville, Fla.

Eagle LNG is a wholly owned subsidiary of Ferus Natural Gas Fuels, a privately held portfolio company of The Energy & Minerals Group (EMG). That is the management company for a series of specialized private-equity funds. EMG invests primarily in natural resources including upstream and midstream. EMG has about $15 billion of regulatory assets under management and $11 billion in commitments allocated across the energy sector since inception.

This will be the smallest of the planned liquefaction operations and will have more in common with a propane distribution hub than with the massive multibillion-dollar deepsea complexes. The $500-million Jacksonville Eagle project is to have capacity of 1.65 MMgal of LNG per day or close to 1 mtpa. It will have 12 MMgal of storage plus marine and truckloading capabilities on site. Eagle would give no in-service date more precise than “early to mid-2020s.”

To be sure, export markets are very much intended, and most of these will be Caribbean islands to which LNG will be shipped in intermodal tank containers.

“Numerous independent studies have shown that sourcing LNG for power generation allows Caribbean island nations the ability to substantially reduce power costs and simultaneously reduce CO2 emissions by 30% to 40% as compared to fuel oil and coal,” said Sean Lalani, president of Eagle LNG, in a company press release.

In addition to providing U.S. gas to the Caribbean basin, once the Jacksonville facility is completed, its operations will be combined with Eagle LNG’s Maxville Facility and the Talleyrand Bunker Station for fueling LNG-powered ships.

Read the rest of E&P's special report on LNG here.