Rigs drill the 16-well Megalodon pad for Aethon Energy Management, landing eight in each the Haynesville and Bossier in East Texas. (Source: Aethon Energy Management LLC)

[Editor's note: A version of this story appears in the August 2020 edition of Oil and Gas Investor. Subscribe to the magazine here.]

In early 2020, LNG tanker-spotting at Gulf Coast ports had become common—online and in person.

A day trip to Surfside Beach, Texas, for example, usually netted a bonus view of one or two docked at the Freeport LNG Development LP terminal across from the town’s boat launch.

Then there were none. Not there.

Not at Corpus Christi, Texas. Not at Sabine Pass, La. Not at nearby Hackberry. In early July, a quick online scan of the Gulf of Mexico spotted none underway either. But they’re coming, according to Welles Fitzpatrick, managing director of E&P research with SunTrust Robinson Humphrey.

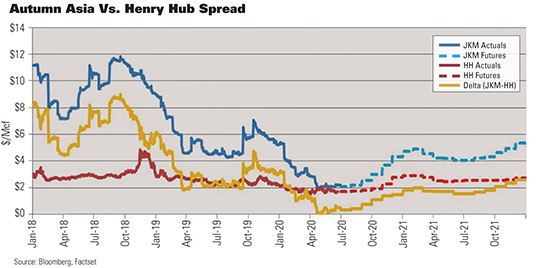

While U.S. LNG exports were down 6 Bcf/d from the pre-downturn 9.6 Bcf/d, demand should improve in October, he reported. The indicator is seen in the Asia-versus- Henry-Hub (JKM-HH) autumn spread. It was more than $1/Mcf in June, “implying sendout could double into year-end.”

U.S. resumption of just the April level of 8.3 Bcf/d of liquefaction “alone would shift us into an immediate and significant undersupply” in November, he added.

While some gas from turning shut-in oil wells back into sales is coming, there are too few rigs drilling to make up for the overall loss, he wrote.

His forecast is that a Henry Hub price of between $3 and $3.50 “is likely in 2021.”

And the Haynesville is ready. J.P. Morgan Securities LLC’s Arun Jayaram, an E&P analyst, wrote in mid-June that there are more than 150 drilled but uncompleted wells (DUCs) in the play.

Leo Mariani, managing director and equity analyst with KeyBanc Capital Markets Inc., reported in early July that, for winter and full-year 2021 futures prices, “Almost every gas-focused E&P is planning to ramp up production during this time.”

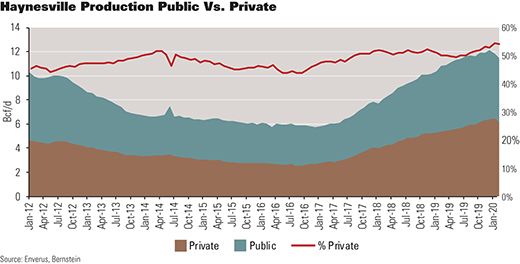

At 12 Bcf/d currently, Haynesville production could grow another 2 Bcf as takeaway is expanded, wrote Jean Ann Salisbury, senior natural gas analyst with AB Bernstein.

As it pushed past 12 Bcf last year, the local differential blew out. Two expansions—CJ Express and Acadian—should make the basin grow to 14 Bcf/d next year, she wrote.

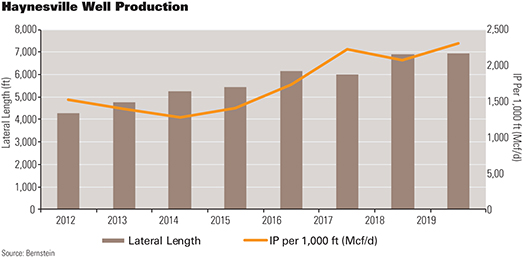

Powerful IPs from Haynesville wells—the average IP is 16 MMcf/d—means “So muchmoney is made in the first year that hedging 24 months of production guarantees payback at the current forward curve,” she added, “and an estimated 40% unlevered IRR by the end of Year 3 even with no terminal value.”

The rig count, including both Louisiana and Texas, was 32 entering July with 21 of those in Louisiana. Four of them were drilling for Comstock Resources Inc., which is now the largest Haynesville operator, producing 1.4 Bcfe/d and marketing 2 Bcfe/d.

As a conventional-formation producer in the region beginning in 1987, Comstock went horizontal in the Haynesville in 2008 in the play’s early days. Already having leases, it stayed clear of the land rush that pushed an acre to as much as $30,000. Instead, Comstock began buying out others in just the past two years.

The company’s Haynesville-prospective portfolio is now 307,000 net acres with proved reserves of 5.4 Tcfe, 98% gas.

In mid-June, Comstock paid down its bank debt—to 62% of the $1.4-billion revolver that had been decreased in April from $1.5 billion— with $441 million of net proceeds from a $500-million 9.75% senior notes placement due 2026, priced at 90% of par and increased from an initially anticipated appetite of $400 million.

The 9.75% notes join its $619 million of 7.5% notes due 2025 that had been paid down by $5.6 million this spring with equity.

In mid-May, it redeemed its $210 million of Series A convertible preferred with $190.4 million of net proceeds from a 40-million-share offering at $5 each. The preferred was held by Covey Park Energy LLC investors, who received them in the $2.2 billion Covey-Comstock merger last summer.

Comstock’s remaining preferred shares outstanding had a face value in June of $175 million, all owned by Dallas Cowboys owner Jerry Jones, who holds 84% of Comstock common.

After the notes offering, Fitch Ratings revised its outlook on Comstock from Negative to Positive, giving the operator a B issuer-default rating.

Among reasons, it cited Comstock’s position as the largest Haynesville producer, low operating and drilling costs, ability to generate free cash flow at strip, low differentials, inventory of nearly 2,000 net well locations, which are 91% operated, and its “significant equity commitment from” Jones.

A unicorn

Investor buy-in of E&P debt and equity offerings had become rare before 2020; uptake in the midst of global-pandemic-inspired soft oil and gas demand is a neutrino-capture type of event.

But natgas investment ideas appear to have some takers.

“There is just such a chasm now between haves and have-nots,” said Jay Allison, Comstock chairman and CEO.

Allison formed Frisco, Texas-based Comstock 33 years ago, building portfolios of both commodities. He transitioned the company fully to gas beginning in 2015 and exclusively in the Haynesville in northeastern Texas and northwestern Louisiana.

Each commodity has had its ups and downs.

“I have seen it from both sides,” Allison said. “It’s hard for the have-nots, and you have to see what kind of resolve you have, what kind of asset base you have and if you can bounce back.”

At Comstock over the years, the focus has been on increasing well productivity and decreasing costs. In 2010, when gas was $5 or more, “We would get about a 30% IRR,” he said.

Early Haynesville wells, at a depth of more than 10,000 ft, cost as much as $12 million, drilled and completed (D&C), for about 5,000 ft of lateral.

Today, “With $2.50 natural gas, we get a 55% IRR,” he said. “You used to think that you have to have a $4 gas price to have that type of return.”

Comstock’s capex budget this year and its outlook for 2021 expect a 55% IRR from its new wells. That includes having hedged 64% of its 2021 production at $2.51. For 2020, 48% is hedged at an average of $2.64.

That there were buyers of its debt and equity offerings demonstrates it has checked all the boxes, he added.

Completion costs have declined further this year as pressure pumpers are looking for where they can deploy equipment and crews.

“Our frac costs really are impacted by the activity in the Permian,” Allison said. “They are not impacted by how busy the Appalachian producers are.”

Peak Permian hydraulic fracturing spreads at work totaled 170; there were 17 in mid-June. Compared with peak Permian, Comstock’s completion costs per frac stage have declined 70%.

Just as recently as first-half 2019, D&C wells of 6,000 ft or more of lateral cost about $1,400 per lateral foot. As 2020 began, it was $1,100. The 2020 target is $950.

Currently, “We’re a little less than $1,000 [per ft],” Allison said. “We’ve come down $400 per foot just to drill and complete these wells.”

Building DUCs

Comstock had nine rigs drilling for it in the fourth quarter. It began 2020 with six and was at four in June, working across its leasehold— not for HBPing leases; its leasehold is virtually 100% HBP.

Rather, Comstock maps targets based on not overwhelming takeaway capacity or disrupting its offset wells.

“So our marketing, geological and operations groups can tell you where every well should be drilled between now and 2022,” Allison said.

Meanwhile, as Haynesville operators are in a long-running collaboration consortium, “We share information with each other, which helps us know where offset operators are planning to drill,” he said. “So we try to coordinate with each other and not interfere with each other’s operations as much as possible.”

Comstock was not completing wells in June—it had more than 20 DUCs—but it had not planned to. Completions will resume in this quarter, putting the new wells online during winter-gas pricing.

When resuming, Allison expects frac costs to decline a further 15% from the 2019 level.

Plans are to produce at least $200 million of free cash flow in 2021 and use that to further pay down its bank debt. Extended laterals in the bag are 237 to date—the most among Haynesville operators. General and administrative (G&A) expenses declined from 14 cents per Mcfe pre-Covey merger to 6 cents this year. Unit operating costs have fallen from 68 cents per Mcfe to 50 cents.

The 20 wells that were completed in the first quarter had IPs averaging 23 MMcf/d— and from four corners of the play rather than in one hot spot.

Versus Appalachia

Comstock’s differentials to Henry Hub are between 20 and 25 cents per Mcf. Its gathering and transportation costs are about 23 cents per Mcf, and the Appalachian was at $1.03 in the first quarter.

Comstock’s EBITDA-margin-to-finding-cost ratio was 3.6 in 2019; the Appalachian Basin’s average was 3.1.

“The advantage is primarily driven by the higher IRR of Haynesville wells,” Allison said.

Comstock’s wells typically pay out in 1.5 years, and the Appalachia plays out in about 2.5 years, extended by higher transportation costs.

“So we get our money back faster. The wells cost more, but we’ll get our money back quicker,” he said. “The midstream costs are less here.”

Comstock doesn’t have minimum volume commitments (MVCs) to shippers.

Altogether, “That’s the difference in where we are and why we’re there,” Allison said.

Frac science

That Haynesville consortium has resulted in intel sharing toward perfecting best practices in the play, particularly in completion design. Operators share results, including findings from individual science projects.

Earlier this year, Comstock was evaluating pumping smaller fracs—less proppant—on some wells.

“We think we can achieve a similar well performance for less cost, resulting in better economics,” Allison said.

Meanwhile, Comstock is staggering intrapad landings in Haynesville and overlying Bossier. And over the past several years, it’s been reducing the length between frac stages and the spacing between clusters, “which delivers better capital efficiency,” he said.

Chokes are being managed to tailor drawdown, maximizing recovery.

“We’ve been doing that for several years, and it seems to be working. The results are pretty impressive.”

How the wells are drilled hasn’t changed much, but “We’re always changing up completions,” Allison said. The recipe is “probably 90% settled out.”

Comstock is also looking at using diverters more often; a neighbor in East Texas is doing this.

“I do think they’re probably going to improve the effectiveness of the fracs.”.

Goodrich DUCs

Goodrich Petroleum Corp. is also seeing lower service costs.

“When you’re spending $11.5 million to $12 million per well and, all of a sudden, you’re seeing a 15% to 20% reduction, that’s pretty dramatic,” said Rob Turnham, Goodrich president and COO. “You’re looking at $1.5 million to $2 million per well, if not $2.5 million in cost savings.”

As well productivity remains strong—12.6 Bcf on average for a 4,600-ft lateral— adding in the D&C savings is “a big improvement in the economics,” he said.

The Houston-based operator holds 22,300 net Haynesville acres. Proved reserves are 510 Bcfe. Production is 137 MMcfe/d.

While service firms are open to long-term contracts, Goodrich would also have to be willing to commit to a level of activity for an extended period. The newly discounted bids are spot rates.

“We can get a two-, three-, four-well package at that rate,” Turnham said. “But they won’t go 12 months out or [longer]. Unless you’re willing to commit to a full-calendar-year program, they’re not willing to lock those prices up.”

Meanwhile, Goodrich’s rig count in June was zero. It had two at work earlier this year and left the wells uncompleted for now, managing for commodity price when it brings them online rather than turning them to sales at the sub-$2 prompt-month price this summer.

“So we have some DUCs that are set to be completed later this year. We built an inventory that would give us that flexibility, once prices recover,” Turnham said. “Thankfully we did it that way because service costs, particularly on the frac side, just continue to fall.”

Otherwise, its $40 million to $50 million of capex this year is to keep its production flat, “with the ability to accelerate in the back half of the year, if prices do materialize,” he said.

At the full-year 2020 strip as of June, Goodrich’s budget generates free cash flow of between $10 million and $20 million. At $2.50 gas and current service costs, it can generate a more than 100% rate of return.

“We’ve never seen that type of return in the basin,” Turnham said. “And, you know, it’s a margin business based on how productive your wells are, how much revenue you generate, what your lifting costs are and what service costs you factor into the capex.”

Roughly 50% of Goodrich’s gas is hedged at $2.60.

“So even though, prompt month, we’re below $2 physically in the market, the numbers work very well when you blend it with our hedges,” he said.

In early July, the lowest 2021 price on Nymex was $2.48; the 12-month strip, beginning this month, was $2.42.

Rubble-ize

Goodrich is also a member of the Haynesville consortium.

“As a group, I think we are very comfortable that we’ve designed the optimal completion recipe, which is tighter frac intervals and proppant concentration of approximately 4,000 pounds per foot,” Turnham said.

Earlier Haynesville wells’ intervals were some 200 ft apart on average; the formula has settled on between 100 ft and 125 ft—“tighter frac intervals, which get you better near-wellbore stimulation.

“You spread the same amount of perforations or holes over a tighter interval. You’re going to rubble-ize the near-wellbore and recover a higher percentage of gas in place,” he said.

In trials with Chesapeake Energy Corp. in 2016, Goodrich pumped as much as 5,000 lb/ft of sand in what were dubbed the “Proppant- geddon” wells. Since then, Goodrich has settled on 4,000 lb/ft, which is still higher than the 1,000-lb formula that was the standard pre-5K trials and the 500 lb in the play’s earliest days. The 5K-loading was resulting in 3 Bcf per thousand feet or more.

“We just didn’t see a big enough incremental difference for the added costs; the rate of return was lower,” Turnham said. “The 5,000 pounds per foot would get you more gas over the long haul. But we just don’t think it gets you the best rate of return on your capital.”

The combination of tighter spacing and the 4K-sand concentration—no matter if a 4,600- ft or 7,500-ft lateral—is booking reserves of between 2.7 Bcf and 2.8 Bcf per foot.

“And that’s compared to our initial hopes of a type curve of 2.5 Bcf per thousand. So we’re getting flatter curves and more reserves per well,” he said. “And because of the service cost reductions, our finding costs have dropped dramatically and rates of return have risen dramatically.”

Closely held

Like Comstock, Goodrich was already an operator in what became the horizontal Haynesville play in 2008

“We were spending probably 30% more to drill and complete our wells. And we were getting less than half the reserves from each well,” Turnham said.

That was when it was pumping some 1,000 lb/ft and getting 1.1 Bcf per thousand feet.

“We’re now pumping four times the proppant, spending 70% of the capital and making 2.5 to 3 times the well result,” he said. “It is phenomenal, really.”

Among all Lower 48 producers, Goodrich is getting the third highest return on capital employed—“and that includes all the Permian guys,” he added.

Its debt is about 1.3 times EBITDA, “so very low from a leverage perspective,” he said. And returns on capital deployed? “We’re probably Top Five, no matter how you calculate it or what your peer group looks like.”

The stock was trading in June at less than 2.5 times enterprise value to EBITDA. Usually that low of a premium suggests a company’s “balance sheet is upside down or they don’t have a place to spend money that makes any money,” he said.

But in Goodrich’s case, the low multiple is likely due to thin trading. Some 56% of shares are held by six individuals and funds; daily volume averages are fewer than 54,000 shares.

“Everyone sees where we’re going, and therefore they don’t want to unload shares, so it doesn’t trade as much,” he continued.

Short-horizon investors aren’t playing the ticker.

But “if you like where gas is going, if you want a conservative balance sheet, if you want good rates of return and you have a time frame that would allow us to let that materialize,” he said, “then it’s a good place to look to make an investment.”

Aethon, 6,000 lb/ft

Private operators produce roughly half of the Haynesville’s 12 Bcf/d, according to Bernstein’s Salisbury. Of the 33 rigs drilling in the Haynesville in early July, according to the Baker Hughes Co. count, about 80% were drilling for privately held operators.

Among those, eight rigs were working for Dallas-based Aethon Energy Management LLC.

Aethon’s Haynesville portfolio has been built through roughly a dozen acquisitions and is virtually 100% HBP. Last year it picked up QEP Resources Inc.’s position, adding 49,700 net acres, 607 operated wells and gathering infrastructure for $735 million.

In May it made a well commitment on Black Stone Minerals LP minerals in the Shelby Trough Haynesville and Bossier in Angelina County, Texas, in exchange for a reduced royalty rate. The operator on the property had been BPX Energy, the Lower 48 onshore upstream unit of BP Plc that has been paring its work to focus on the Haynesville core.

Aethon’s Haynesville and Cotton Valley net acreage totals 340,000 to date, producing net 1 Bcfe/d.

The company has several field trials underway in the play.

“Our business has really turned more into manufacturing with highly predictable results,” said Gordon Huddleston, Aethon co-president. “But there are always a few tests and modifications we’re doing to continuously get better.”

In one, the company is working with a BJ Services Co. natgas-powered frac fleet.

said the 16-well Megalodon pad

should fill the new Bland Lake

gas plant from the outset.

“We’ve done some initial testing, and it was successful,” Aethon COO Paul Sander said. “Fewer pumps on location, fewer people and using a cheaper fuel.”

Sander expects it “could be somewhat transformational for the fracking industry.”

In addition, Aethon is using Precision Drilling Corp.’s latest-generation rig that allows automated drilling.

“That’s really helping us speed up connection times,” he said. “And we’re also using managed pressure drilling that has reduced the amount of time required to run casing, primarily, so some benefits are associated with that.”

In East Texas in mid-June, the company was developing a 16-well pad, Megalodon, to test both capital efficiency and spacing. Eight of the wells are landed in Haynesville and eight are in the upper Bossier.

Laterals in each are about 7,500 ft. Half of the Haynesville and Bossier wells travel north and the other half travel south.

Half of the wells were expected to be brought online in July and the other half in November.

The to-sales timing is while Aethon is building out its midstream business in East Texas. The staggered time line is in tandem with the startup of its main gathering system as well as its new gas plant at Bland Lake in northern San Augustine County.

“So as opposed to developing one well at a time [from small-pad developments] with production slowly ramping up, you are bringing on a set of wells to fill the plant at the outset,” Huddleston said. “These midstream infrastructure projects have a much better return when they can be closer to capacity.”

Sander said the midstream business was the primary driver for the Megalodon project.

“It’s doubtful that we’ll do another 16-well pad,” he said, “but we may entertain four- and six-well pads instead of two- or three-well pads based on what we learn here.”

The operator also has trials underway with eight-well pads, adding a couple of wells per section to determine whether two more affects overall recoveries.

It was also testing pumping the same amount of sand but with less water. Its frac jobs are usually slick water; the design being tested requires a gel system.

Meanwhile, it is testing as much as 6,000 lb/ ft of sand in wells.

“We tend to be a bit more aggressive in terms of how much sand we pump,” Sander said.

And the company was investigating results from far-field diverters to see if that improves the overall frac efficiency and complexity, thus better well performance—“and perhaps also minimizing damage to wells while we frac,” he said.

The slowdown in the oil side of the industry has brought new oilfield technology attention to the Haynesville, he added.

“A lot of R&D efforts have been focused on the Permian, and that’s really not the same animal as the Haynesville. We have a lot higher pressure and a lot higher temperature,” Sander said.

The Haynesville’s depth is between 11,000 ft and 13,000 ft in Louisiana and between 13,000 ft and 14,000 ft in Texas, while Permian targets are between 4,000 and 12,000 feet. “So we just have different equipment needs and different reliability issues,” he said.

EURs, rigs

Across its well portfolio, Aethon is booking 2.5 Bcf per thousand feet of lateral in Louisiana, on average, and 2.2 Bcf per thousand in Texas, depending on vintage and geology, Sander said.

Outside of field trials underway, the company’s completion recipe varies little.

“I think that, for the most part, we’ve standardized our operation,” Sander said. The trials are “usually multiyear-type efforts. And if they work, they become part of the new standards. But we believe we’re between 90% and 95% there.”

Aethon started 2020 with 10 rigs; in June, it had eight in the field.

“That’s kind of where we expect to remain,” Huddleston said. “It’s really more about just managing capital and whether our working interest partners are going to participate in future development. That has the biggest impact on our rig count right now.”

The company is hedged. It keeps the details private. But, Huddleston said, “We have more than 90% of expected volumes hedged for both 2020 and 2021 and then it trails off from there.

“We really view how we manage commodity price volatility as the core of our business model. It really is the critical component, especially because things have shifted into a more predictable type development mode.”

Sander added, “We try to lock in and ensure our cash flow. And we are also trying to own as much of the pot [as possible]. We’re not only an E&P player; we are a significant midstream owner/operator.”

Oilfield service costs are declining, resulting in a roughly 10% lower cost structure to Aethon. “Just like we lock in our cash flows with hedges, we also tend to do long-term arrangements with our major service providers,” he added.

Huddleston said, “Our main focus from a corporate standpoint is on risk management. And I think that’s why we’re able to continue developing through these downturns, whereas some of our peers may be in a more difficult or challenging position.”

Drilling through it

Also privately held, Houston-based Rockcliff Energy II LLC had four rigs drilling for it in East Texas in June. After picking up its 276,000 net acres—of which 150,000 include the Haynesville—in two acquisitions, including from Samson Resources II LLC in 2017, it has had four at work continuously.

Plans are to continue with four through 2020. It is running DUC-less, and it is completing new wells as they’re done. Net production is just under 700 MMcfe/d.

In the early days of targeting Haynesville in East Texas in Rockcliff’s area, “A lot of people were thinking ‘East Texas isn’t going to work. It’s going to have too much clay, or it’s just not going to be as good as Louisiana,’” said Alan Smith, Rockcliff president and CEO. But “It’s just performing really well.”

Smith’s oil and gas career began in East Texas in 1986. Beginning in 2003, East Texas assets have been a part of five of his startups’ portfolios.

Current declines in service costs are a boon. “You name it. Across the board, it’s all come down,” he said.

Rockcliff’s rig contracts tend to be six months, rolling, plus or minus. On completions, it contracts with one pressure pumper for a year.

“And then we have another frac player that kind of plays our second spot, which is pretty much full time, and we’re locked in with those guys for the year,” Smith said. There are “outs in the contract on both sides, but it’s a commitment to move forward with them and vice versa.”

Rockcliff has 80% of its 2020 production hedged at about $2.60, about 80% of 2021 at $2.56, and, for now, between 50% and 60% of 2022 at $2.48.

“We focus on locking in our underwriting on commodity prices, which, in this environment, has helped us increase the margins and make our economics even better,” Smith said. “A lot of people ask ‘Why are you running four rigs?’”

Natgas in June was sub-$2.

“The answer is ‘Because it’s economic.’ We just plan to drill through the cycle,” he said. “We’ve taken a lot of the price-risk out. We’ve got flow assurance with transportation and are pretty well locked in on basis. So we feel good about it.”

Even without the hedges, though, “It’s highly economic,” he added. Rockcliff’s IRRs at the June strip were some 50% on most of its wells. “That’s a very good return,” he said.

It is a sharp contrast to the oil-weighted business today. While oil producers were struggling to find returns, natgas producers have clarity.

“I tell the guys [here] every day, ‘stay humble,’” he said. “We’ve got a great asset and, while most everyone else’s borrowing base is staying flat or getting cut, our borrowing base just went up.”

It was increased from $700 million to $750 million—and on organic growth in asset value rather than acquisition.

“So that’s a huge testimony to the quality of our assets,” Smith said. “We’re putting new wells online that further enhance the value of the company, and we were rewarded by the banks. When you have 13 banks doing their due diligence and all agreeing that you should get an increase, that’s a big stamp of approval.”

Rockcliff’s leverage is less than 2 times EBITDA, which is “roughly two times asset coverage,” Smith said. “So that’s a very strong position to be in.

“That’s why we hedged such significant amounts—because we’re not worried about what we’re leaving on the table. We’re more worried about protecting our capital.”

Denser spacing

To combat costs, Rockcliff began developing its leasehold in 2018 with pad drilling exclusively. “So nearly every well we drill has been anywhere from a two-well to a four-well pad. There are a lot of efficiencies in that,” Smith said.

Also it is wine-racking, landing in both the upper and lower Haynesville in most of its pads.

“Here in East Texas, we’re getting more thickness in a large part of our acreage than they have in Louisiana, which translates to more gas in place,” he said.

Well spacing is 800 ft and stage spacing is 100 ft. Proppant is 3,500 lb/ft, delivered with between 85 and 100 bbl of water per foot, up from recipes of between 30 and 50 bbl per foot in the Haynesville’s early days.

“I think that’s what cracked the code over here on the East Texas side,” Smith said. “You’re trying to maximize stimulated rock volume.

“And by going to denser stage spacing on the fracs and pumping more fluid, we’re able to get a significant amount of stimulated rock volume.”

The 800-ft spacing is possible “because you are able to stagger your locations,” he added.

outlooks on the Haynesville’s

margins. “They say that the

best parts of the Haynesville

need $2.50 at a minimum. But that is just not true. We’re living it,” he said.

As for EURs, these are complicated by that, prior to Rockcliff’s entry to the area, the Haynesville had been completed with less sand and water than today. Rockcliff’s application of modern-intensity completions has resulted in enough wells to predict EUR across its acreage.

“In the initial wells we drilled, most of our results were semibounded in a lot of ways,” Smith said. “And when it’s semibounded, you get higher EURs.

“Then, as you begin to drill in a development pattern, you end up with bounded and semibounded wells and some parent/child situations.”

Nevertheless, Rockcliff’s EUR is looking like between 2.2 Bcf and 2.7 Bcf per thousand feet of lateral in the bulk of its acreage, averaging about 2.5 Bcf.

Sometimes it has to use four strings to drill and complete a well.

“But our three-string wells were originally $13.5 million. Now those wells cost $11.4 million. So we’ve taken $2 million of the capital costs per well out of the equation,” Smith said. “And the results are just as good or better on the EUR side. That’s why you’re getting such really strong returns—even in this environment.”

‘Living it’

Rockcliff picked the Haynesville when forming in 2017 for a couple of reasons, Smith said. It saw the rock being productive over a large area.

“Secondly, it is located in one of the best places in North America to own natural gas because it is the closest to the Henry Hub,” he said. “Haynesville gas is in front of just about any gas that’s produced in the country in going to the markets.”

And the rock performance “has been even better than expected,” he added.

The neighborhood is friendly, and there is plenty of takeaway capacity.

“So when you put all those ingredients together, it’s really some of the best economics in the country right now,” Smith said.

Rockcliff’s all-in cash costs are under $1/ Mcfe. For most Marcellus operators, it is more than $1.50. For one of them, it is nearly $2.50.

Gathering/transportation/compression is 25 cents per Mcfe for Rockcliff. For most Marcellus operators, it is 75 cents or more.

“No one’s questioning whether they have great rock,” he said. Rather, “They agreed to these MVCs in a much higher gas-price world. Some are 10-year. Some are 15-year. Depending on the company, they still have multiple years of MVCs on their books.”

Rockcliff’s breakeven cost with a 20% return is between $1.90 and $2.15 flat, depending on where it is in its leasehold.

“I do not understand why the research analysts have such a hard time grasping the Haynesville,” Smith said. “If you look at the stuff they put out, they say that the best parts of the Haynesville need $2.50 at a minimum.

“But that is just not true. We’re living it.”

Osaka’s Sabine

Doug Krenek has long been familiar with the East Texas subsurface. The president and CEO of Sabine Oil & Gas Corp. had worked with Rockcliff’s Smith at Chalker Energy Partners II LLC.

Smith’s first iteration, Chalker I, was sold to Forest Oil Corp. in 2006; Chalker II was sold to Nabors First Reserve (NFR Energy LLC) in 2008. Smith and Krenek moved on to forming other startups.

Meanwhile, NFR Energy was renamed Sabine Oil & Gas Corp., and it merged with Forest in 2014. So Sabine’s portfolio includes “legacy Chalker I and legacy Chalker II,” Krenek said.

Sabine exited Chapter 11 reorganization in 2016. Krenek was hired in 2017 to run the company.

This past November, it was purchased by Japan- based, publicly held, Osaka Gas Co. Ltd. subsidiary Osaka Gas USA Corp., which also holds an equity interest in Freeport LNG and several U.S. gas-fired power plants.

Sabine’s 175,000 net acres and Rockcliff’s acreage “touch in a lot of places, and we’ve done deals together with trades, joint wells and water disposal,” Krenek said. “We communicate and work together a lot.”

Sabine has three rigs running—two drilling Haynesville and one in Cotton Valley—up from two in the fourth quarter of 2019. The Cotton Valley drilling is in Rusk and Upshur counties, which are adjacent to the west to Panola and Harrison counties where Sabine is drilling for Haynesville.

As the operator went through reorganization, its MVCs were rejected in what is cited as a precedent ruling in U.S. Bankruptcy Court.

Finding and development expenses are between 70 and 80 cents; facilities development and operations all-in costs, including G&A, are about $1.60. Production is about 300 MMcfe/d, which includes some oil from the Cotton Valley. More than 80% of its gas is hedged. Its well count is approximately 1,200.

Currently, science-ing right now is on parent/ child wells, Krenek said.

“We haven’t drilled many parent/child wells yet,” he said. “But understanding how they’re going to perform will be important to us because, as we go further into development, we’ll be doing more of these kinds of wells.”

In eastern Harrison County, the company’s acreage is prospective for both Haynesville and Cotton Valley.

“We’re looking at some areas where we could develop potentially 10 wells from a pad,” Krenek said. “You’d have three Haynesville wells to the north, three to the south, two Cotton Valley to the north and two to the south.

“We’ve done individual wells confirming productivity, but we haven’t done the pads yet.”

Meanwhile, its completion recipe is fairly settled on.

“We’re doing little tweaks on number of clusters and testing increased proppant loading. But, for the most part, we feel pretty comfortable with where we’re at,” he said.

EURs for its Haynesville are more than 2 Bcfe per thousand feet of lateral; for the Cotton Valley, it is about 1.5 Bcfe per thousand.

Sabine’s acreage is primarily HBP except for its newly acquired leasehold.

“We try to replenish our inventory every year through grassroots leasing and bolt-on acquisitions and farm-outs,” he said. “All our drilling is HBPing in that new acreage we have picked up.”

Long-term view

Osaka had been evaluating ownership of U.S. natgas reserves since 2015. It picked up 35% working interest in the Haynesville half of Sabine’s portfolio in 2018, before buying Sabine as its platform U.S. upstream entry as an operator last year.

Ownership by an international conglomerate with an interest in gas reserves has meant that Sabine now has a long-term view when developing its assets, Krenek said.

When working for private-equity investors in the Chalker series and with the original Sabine owners, “We knew we were going to have an exit,” he said.

“But now, with a long-term view [at Osaka], we think and plan everything long term. We can make long-term investments in infrastructure. We can work with our service providers on a more long-term basis.

“We want them to be around for the long term with us. So we’re trying to get win-win solutions with all our providers, whether it’s the gatherers, the frac companies, the drilling companies, everyone.”

That includes land and minerals owners.

“When people have land open and are trying to lease, a lot of times they’re calling us because over the past three years we’ve demonstrated that we do what we say,” he said. “They’re confident that, if they partner with us, they’re going to be successful.”

Is Osaka looking to buy more Lower 48 gas reserves?

“Right now, we’re kind of in the ‘prove we did a good deal stage.’ So they’re not willing to take that leap yet until we can get this first year under our belt and they’re comfortable that their investment is doing what they wanted it to,” he said.

He believes Sabine will stick to natgas.

“I think we see that we’re not going to be a player chasing oil. I think they’re on board with that, because we think natgas is a cleaner fuel and will bridge us to the future,” Krenek concluded

Recommended Reading

Dividends Declared in the Week of Aug. 26

2024-08-30 - Here is a selection of dividends declared from select upstream and service and supply companies.

Talos Energy CEO Tim Duncan Steps Down; Mills to Take Helm

2024-08-30 - An analyst said Talos Energy President and CEO Tim Duncan was forced out over share price performance, although other factors may have played a role.

HNR Acquisition to Rebrand as EON Resources Inc.

2024-08-29 - HNR’s name change to EON Resources Inc. and a new ticker symbol, “EONR,” will take effect when trading commences on Sept. 18.

Hunting Wins Contracts for OOR Services to North Sea Operators

2024-08-29 - Hunting is securing contracts worth up to $60 million to deliver organic oil recovery technology to increase recoverable reserves for North Sea operators.

GreenFire Appoints Rob Klenner as President to Deliver Geothermal Solutions

2024-08-27 - As president of GreenFire Energy, Rob Klenner will be responsible for overseeing GreenFire’s geothermal energy projects.