At first blush, summer seems to conjure happy thoughts such as sun, beaches, baseball, fireworks and family vacations with songs like “Surfin’ U.S.A.,” “Summer Nights” and “Cool for the Summer” helping to create the season’s soundtrack. However, a darker soundtrack for the season can just as easily be formed with classics like “Cruel Summer,” “Summertime Blues” and “Summertime Sadness” leading that playlist.

This summer undoubtedly falls in the latter category for the hydrocarbon market with prices continuing to slump in the natural gas, NGL and crude oil markets. In this case, the sooner that winter comes, the better.

Indeed, these markets should experience an uptick in the fall and winter as heating demand increases and with Saudi Arabia set to pull back production from its record high of 10.56 million barrels (bbl) produced in June by 200,000 to 300,000 bbl per day (bbl/d), according to The Wall Street Journal. This isn’t a reflection of the country changing its stance on production; rather it is related to seasonal reductions in cooling demand as Saudi Arabia uses crude-fired power generation.

The record production out of Saudi Arabia has helped stunt the modest gains that West Texas Intermediate (WTI) crude experienced in the spring and early summer. In the past two months, WTI has lost $10/bbl in value as it is now trading under $50/bbl.

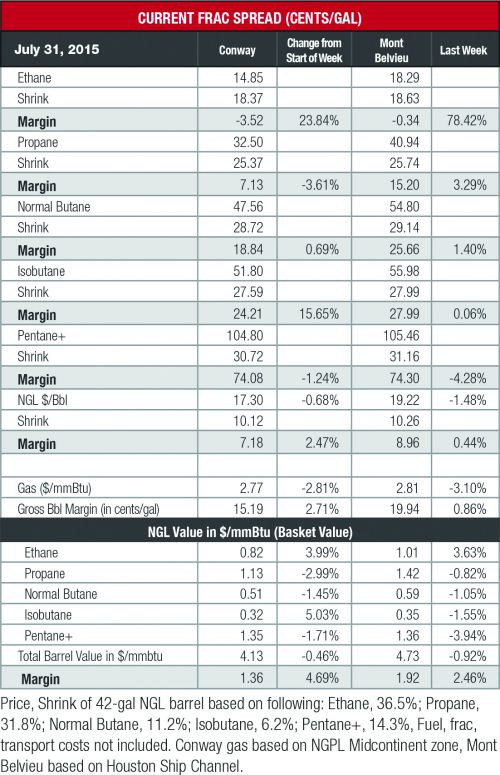

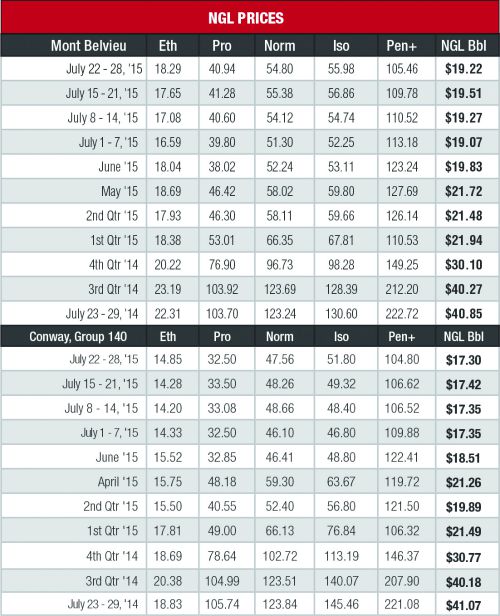

This downturn has had a negative impact on heavy NGL prices, especially C5+, which has lost 17 cents per gallon (gal) at both Conway and Mont Belvieu in the past month. Butane and isobutane prices have stabilized in the past month as refiners will soon begin to switch from refining summer-grade gasoline to winter-grade gasoline.

Light NGL prices remain challenged, but are moving in opposite directions. The outlook for propane still remains negative as stock levels are at their highest levels in five years and it will take a perfect storm of increased winter heating and crop-drying demand along with peak LPG exports. Such a scenario is unlikely to occur, which will keep propane prices challenged for the next year. However, it is likely that prices are at their bottom for the year and will improve in the fall and winter.

Ethane prices experienced 4% gains at both hubs as inventory levels are beginning to drop with rejection efforts finally beginning to have a noticeable impact on stocks. It is important to note that prices have a long way to go to return to steady profitability. Prices this week were their highest in a month at both Conway and Mont Belvieu at 18 cents/gal each, but remained unprofitable.

Frac spread margins were helped by lower gas prices at both hubs as prices were down 3% for the week. The Conway price fell to $2.77 per million Btu (MMBtu) and the Mont Belvieu price was down to $2.81/MMBtu. This resulted in margins generally improving with ethane having the largest gain, but C5+ remained the most profitable at 74 cents/gal at both hubs. This was followed, in order, by isobutane at 24 cents/gal at Conway and 28 cents/gal at Mont Belvieu; butane at 19 cents/gal at Conway and 26 cents/gal at Mont Belvieu; propane at 7 cents/gal at Conway and 15 cents/gal at Mont Belvieu; and ethane at negative 4 cents/gal at Conway and nil at Mont Belvieu.

Natural gas storage levels rose by a smaller-than-expected 52 billion cubic feet, which implies a nearly balanced market according to Tudor, Pickering, Holt & Co. Storage levels rose to 2.88 trillion cubic feet (Tcf) the week of July 24 from 2.828 Tcf the previous week. This was 26% greater than the 2.294 Tcf posted last year at the same time and 3% greater than the five-year average of 2.795 Tcf.

Cooling demand will be mixed this week as the National Weather Service’s forecast anticipates warmer-than-normal temperatures in the Southern U.S., but cooler-than-normal temperatures in the Northeast and Midwest.

Contact the author, Frank Nieto, at fnieto@hartenergy.com.

Recommended Reading

Exxon Versus Chevron: The Fight for Hess’ 30% Guyana Interest

2024-03-04 - Chevron's plan to buy Hess Corp. and assume a 30% foothold in Guyana has been complicated by Exxon Mobil and CNOOC's claims that they have the right of first refusal for the interest.

Petrobras to Step Up Exploration with $7.5B in Capex, CEO Says

2024-03-26 - Petrobras CEO Jean Paul Prates said the company is considering exploration opportunities from the Equatorial margin of South America to West Africa.

The OGInterview: How do Woodside's Growth Projects Fit into its Portfolio?

2024-04-01 - Woodside Energy CEO Meg O'Neill discusses the company's current growth projects across the globe and the impact they will have on the company's future with Hart Energy's Pietro Pitts.

Deepwater Roundup 2024: Offshore Australasia, Surrounding Areas

2024-04-09 - Projects in Australia and Asia are progressing in part two of Hart Energy's 2024 Deepwater Roundup. Deepwater projects in Vietnam and Australia look to yield high reserves, while a project offshore Malaysia looks to will be developed by an solar panel powered FPSO.

Pitts: Heavyweight Battle Brewing Between US Supermajors in South America

2024-04-09 - Exxon Mobil took the first swing in defense of its right of first refusal for Hess' interest in Guyana's Stabroek Block, but Chevron isn't backing down.