The temperatures being experienced in much of the U.S. to start 2015 are an unwelcome cold blast from the past for most Americans, but gas and liquids producers are hoping that they bring a price surge similar to last winter’s. While temperatures are in the same range as last year’s infamous polar vortex, thus far the surge in prices hasn’t occurred yet.

Short of an extended cold front it is extremely unlikely gas and propane prices will begin to approach the levels they had last year due to the degree they’ve fallen in the past few months. Though storage was worked off in fairly short order last winter, prices were much stronger at that time.

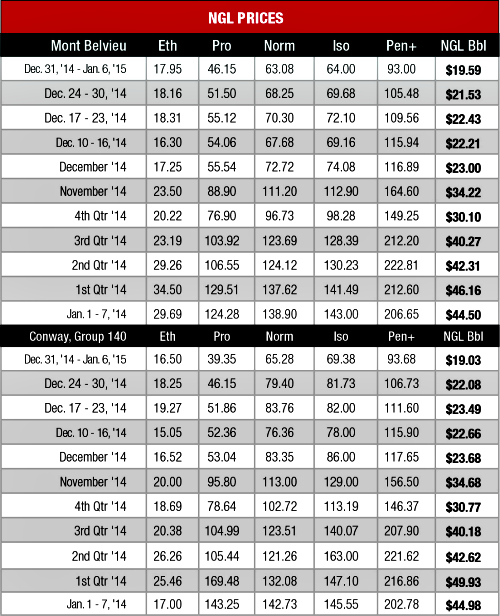

Indeed, Conway propane was four-times as valuable and Mont Belvieu propane was nearly three-times as valuable at the start of 2014 as current values. Natural gas prices were $1 per million Btu (/MMBtu) greater than their current levels.

The propane storage overhang is so large that it will require a combination of both heating and export demand to be worked off. In order to encourage LPG exports, propane prices will likely have to continue to follow crude prices.

Thus far prices have not had a problem tracking with West Texas Intermediate (WTI) crude as Conway propane—which typically posts the largest gains in the fall and winter due to increased crop-drying and heating demand—fell to its lowest level in more than a decade. Following a 15% decrease, the price fell to 39 cents per gallon (/gal), the lowest it has been since it was the same price the first week of August 2002. The Mont Belvieu price was supported a bit more by LPG exports as it fell 10% to 46 cents/gal, the lowest it has been since it was 45 cents/gal the week of Aug. 29, 2002.

While new construction of midstream infrastructure is a positive for the near-term, it is having an impact on netbacks at the moment while transportation and fractionation costs have increased to cover construction costs. With NGL prices tracking lower, it is making it even harder for producers as margins are further hampered.

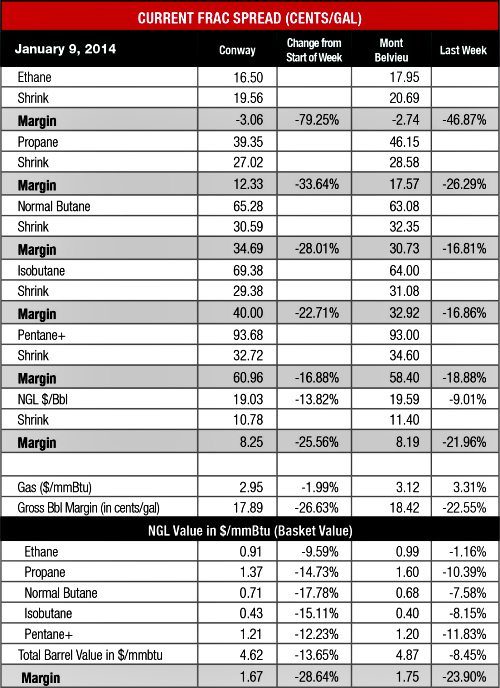

Traditionally ethane required a frac spread margin of more than 6 cents/gal to achieve true profitability once transportation and processing costs were factored in. Newbuild costs have helped to drive this level up slightly in some parts of the country, which further hampers an extended ethane price rebound.

Ethane prices leveled off at Mont Belvieu where they fell 1% to 18 cents/gal, but experienced a 10% decline at Conway to 17 cents/gal with limited trading. After nearly reaching a nil margin the final week of 2014, ethane collapsed as margins fell 79% at Conway and 47% at Mont Belvieu. In short, it’s highly unlikely that ethane will be profitable in the near term.

The biggest question mark in regards to where the NGL market is headed is, of course, when does the free fall in crude oil prices stop? This is an especially tough question to answer given that there are strong indications that the market is overreacting to negative news regarding crude fundamentals.

While global and domestic production and storage levels are high, the U.S. Energy Information Administration (EIA) reported that crude reserves decreased by more than 3 million barrels (MMbbl) when industry expectation were for slightly less than a 1 MMbbl build. This indicates that domestic demand is stronger than expected, but WTI crude only experienced a minimal price improvement. At some point, crude prices will hit their floor and begin a recovery. While it is possible this floor has been reached, it is just as likely that prices will bounce off that floor several times before coming back to life.

Theoretical NGL bbl prices fell to their lowest levels at Conway and Mont Belvieu since 2008 as they were down 14% to $19.03/bbl with a 26% drop in margin to $8.25/bbl at Conway while the Mont Belvieu bbl fell 9% to $19.59/bbl with a 22% decrease in margin to $8.19/bbl. This should further encourage a pullback in liquids drilling and give the market more time to work off excess volumes during a price recovery.

Natural gas prices continue to hover at about $3/MMBtu, but could see improvement in the near term due to the solid storage withdrawals resulting from frigid temperatures. The EIA reported that gas storage levels were down 131 billion cubic feet to 3.089 trillion cubic feet (Tcf) the week of Jan. 2 from 3.22 Tcf the previous week. This was 9% above the 2.839 Tcf figure posted last year at the same time and 2% below the five-year average of 3.156 Tcf. The National Weather Service’s forecast for the week of Jan. 14 anticipates normal weather temperatures, which should continue to deplete storage levels and support gas prices.

Recommended Reading

Sangomar FPSO Arrives Offshore Senegal

2024-02-13 - Woodside’s Sangomar Field on track to start production in mid-2024.

NAPE: Chevron’s Chris Powers Talks Traditional Oil, Gas Role in CCUS

2024-02-12 - Policy, innovation and partnership are among the areas needed to help grow the emerging CCUS sector, a Chevron executive said.

CNOOC Makes 100 MMton Oilfield Discovery in Bohai Sea

2024-03-18 - CNOOC said the Qinhuangdao 27-3 oilfield has been tested to produce approximately 742 bbl/d of oil from a single well.

TPH: Lower 48 to Shed Rigs Through 3Q Before Gas Plays Rebound

2024-03-13 - TPH&Co. analysis shows the Permian Basin will lose rigs near term, but as activity in gassy plays ticks up later this year, the Permian may be headed towards muted activity into 2025.

Proven Volumes at Aramco’s Jafurah Field Jump on New Booking Approach

2024-02-27 - Aramco’s addition of 15 Tcf of gas and 2 Bbbl of condensate brings Jafurah’s proven reserves up to 229 Tcf of gas and 75 Bbbl of condensate.