Northern Oil & Gas has been on a hot streak of acquisitions, particularly in the Permian Basin. In June, Minneapolis-based NOG announced plans to acquire a 33.33% stake in EnCap-backed Delaware Basin E&P Novo Oil & Gas for $500 million—NOG’s largest deal to date. Earthstone Energy is scooping up the other 66% interest in Novo for $1 billion.

NOG closed a $167.9 million acquisition of Delaware Basin assets from Forge Energy II, another EnCap portfolio company, in late June. Vital Energy Inc., which will become the operator of the assets, agreed to purchase 70% of Forge’s assets for $378 million, with NOG purchasing the remaining 30%.

Earlier this year in the Midland Basin, NOG boosted its non-operated stake in the Mascot Project up to a 39.958% working interest. NOG had initially acquired a 36.7% interest in the project for $320 million in October 2022.

NOG is also making strides in its ground game, completing 13 mini-transactions that are expected to add more than 16 net wells to production in the coming years, the company reported in second-quarter earnings released Aug. 2.

In an exclusive interview with Hart Energy, NOG CEO Nick O’Grady and President Adam Dirlam said the company sees a nearly endless stream of opportunities to acquire disparate non-op interests in its development areas. The company has also considered expanding its footprint into new regions—if NOG can find the right deal.

Chris Mathews: NOG has announced several deals recently—including the Novo acquisition, NOG’s largest transaction to date. How has the company’s M&A strategy evolved over time?

Nick O’Grady: I think some of the evolution you've seen, just from the structure of our deals, is less a function of us changing our strategy. As the business has become larger, we’re capable of doing things that maybe always existed, but we did not have the capability when we were smaller, either from a risk or financial perspective.

I think I’d be very resistant to saying that we are evolving the business model into something else. I think if it's evolving, it's just that we can do three or four discreet businesses where once we did one or two.

In the lifecycle of A&D, I think that, at least for the time being, we’re close to a crescendo in terms of the volume of private M&A going on—meaning you’ve seen a lot of M&A activity in the last 12 months. A lot of sponsor companies are finally being sold. I think that you’re in the tail end of that.

There's still some to go. There are still an inordinate amount of companies that need to find a permanent home at some point, but maybe not of the same scale.

On the non-operated side, there are so many billions of disparate non-op interests that exist out there. I think that that's a business that will keep us very busy for a long time.

"I think we would love to grow our gas properties, especially in Appalachia. We're actively looking there." —Nick O’Grady, Northern Oil & Gas

Adam Dirlam: I think the co-buying or buying down minority interests in an operated asset really is the function of our scale. We've been doing this for the past few years. It just hadn't necessarily gotten to the level that might've been press-release worthy.

We’ve been partnering with operators across all our respective bases, helping them out as a capital provider, but really focusing on alignment and being an equitable partner.

I think the drillco’s of old left a bad taste in a lot of operators’ mouths. We've talked to a number of operators, both big and small, and at the end of the day, they wanted something that was different from a structural standpoint.

And our ability, especially as an engineering-centric E&P company, to approach the underwriting in an equitable fashion, has given us a leg up to really consider both the social and the operational dynamics as you perpetuate the development of these assets.

NO: What I think Adam is getting to is that we’re a permanent owner of these assets. We’re willing to take risk. We're not trying to turn it into a security in which all that risk is borne by the operator, and then somehow we want to go away at some point.

That trumps the cost of capital—being a fair and equitable partner. And what we need on the other end is for it to be fair and equitable.

What we try very hard to do, and you'll see me talk about this in our public statements, is we really believe in a portfolio management approach. And we have a portfolio theory: keep the diversity of the business, the diversity of operators and interest and partners.

We have problems every day, but the goal is to keep those problems relatively small, not to have all your eggs in one basket. Relationships are really important to us, but I think really when it comes down to it, is that we want to be a fair transacting partner, not necessarily to be in bed with one person or another for personal reasons.

AD: That’s right. We’re looking at true non-op packages day in and day out. We've got our ground game strategy, which is kind of the micro-acquisitions, where you’re dust-busting disparate interests.

The business model lends itself to the ability to stay within the core of our respective base ends, which then gives us the ability to maintain our return on capital employed. So, we don’t necessarily need to scale the business by stepping out into tier-two and tier-three acreage.

We continue to see hundreds of opportunities throughout each and every quarter, and it really gives us the opportunity to be picky and keep our hurdle rates where they need to be.

CM: What are the benefits to spreading your eggs—your non-op interests—around multiple baskets, versus keeping them all in one?

NO: One thing that’s notable about Forge and Novo—as well as a lot of the transactions we’ve done that have been more traditional non-op—is that even when we go down to the ground game level of when development is being sold, the dollars are important to what your competitive landscape is, but it’s also the concentration.

Buying 10 distinct 10% interests versus one 100% interest has a big impact on that risk management. When you’re a portfolio of 9,000-plus wells, we can take that 100% interest-type scenario. That’s certainly not the normal case for us to take something that high, and our average is still less than 10% as a portfolio.

The point being that it’s not just that it’s $50 million, but $50 million concentrated in a few things can disqualify a good portion of our competitors. Because even if they had the money, they can’t take a 50% interest in one well or something like that.

AD: I think the risk factors are effectively equal. But if one thing can go wrong on a large working interest with a small base, that could potentially tip over a small non-operator. What that gives us the ability to do is raise our discount rate and still get things done.

"We're not just buying a piece of land and then waiting for the rigs showing up. We're actively targeting the operators in the areas that we want to be in and then getting in ahead of the drill bit." —Adam Dirlam, North Oil & Gas

CM: Is NOG interested in expanding into new basins through M&A?

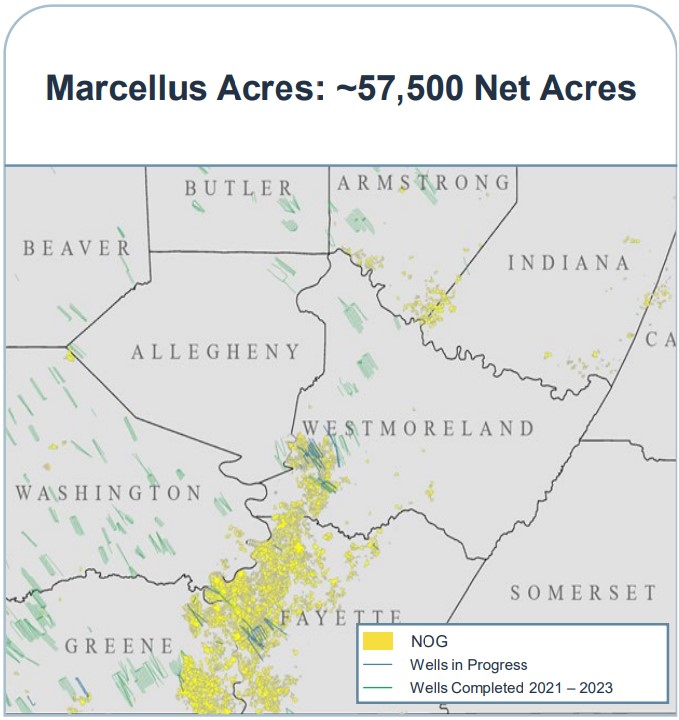

NO: I think you don’t need to look far from where we already are. I think we would love to grow our gas properties, especially in Appalachia. We're actively looking there. I think that’s one that we have optimism that we can do. Given the nature of the land and other issues in Pennsylvania, it really has to be very specific to certain things.

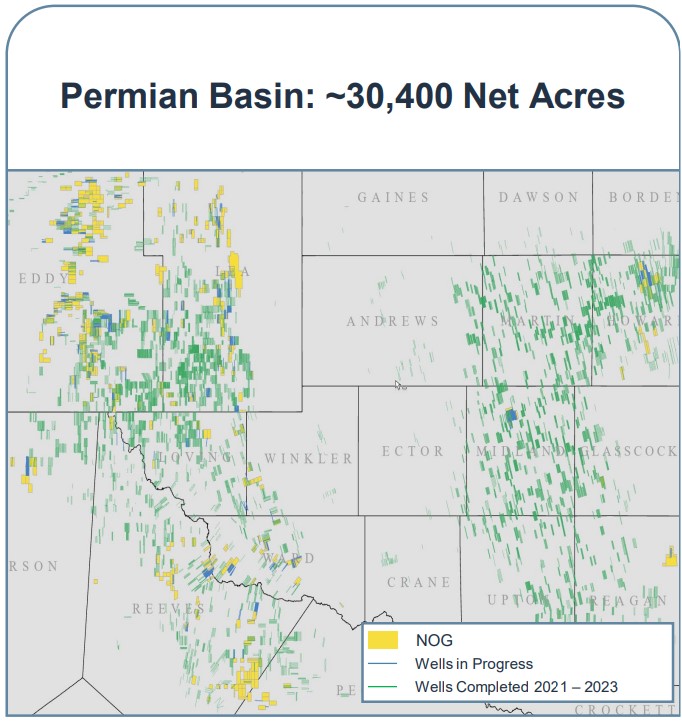

The Permian has as many rigs as the rest of the United States combined. As you can imagine, the volume of things going on, the fractional nature of the ownership across [the Permian], it creates a ton of opportunities.

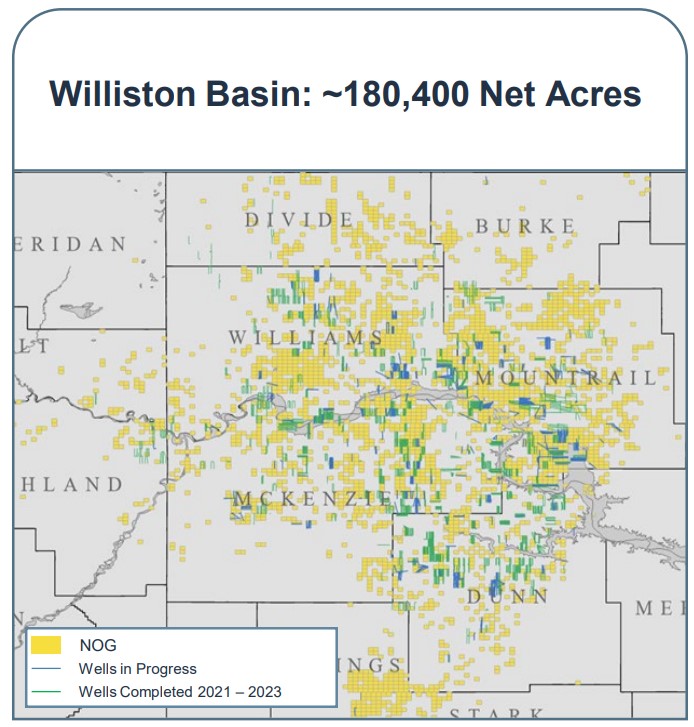

And in the Williston, which is our legacy asset—we continue to surprise ourselves with significant opportunities. We’re going to hit record volumes in the Williston this year, which is interesting. It’s not that we have de-emphasized it in any way, it’s just that other things have grown faster. But we have continued to find ways to grow the business there.

AD: And that’s a testament to the active management, right? We're not just buying a piece of land and then waiting for the rigs showing up. We're actively targeting the operators in the areas that we want to be in and then getting in ahead of the drill bit.

CM: Some of your biggest deals have been in the Permian Basin. What’s the state of Permian M&A; how competitive is it out there?

NO: I think for the first time in about 20 years in the United States, you really have sudden fears both from investors and Wall Street that shale is reaching its zenith in terms of locations; that it is a finite amount. Suddenly, inventory has become precious.

A few years ago, when it really came down to just survival, I think a lot of operators were more focused on generating cash and deleveraging, and not necessarily about replacing that inventory. Of those larger, chunkier private opportunities, there's been a bit of a feeding frenzy in some of the cases. And it’s varied from deal to deal, to be candid in our view, at least from how we look at these assets.

There has been a tale of haves and have-nots, where some of the midsize public companies have been in a replacement cycle or rejuvenation cycle—that’s why you’ve seen a slew of transactions.

In terms of the larger scale of those, at least from a sponsor perspective, they are starting to peter off. There are a number of very large private companies that could sell at a moment’s notice. But in terms of sponsor-backed stuff, I think you’re probably in the seventh or eighth inning of that for the time being.

There are smaller targets that aren’t necessarily going to grab the attention of the larger operator, and they may get sold at some point, or may merge into other midsize entities.

The trend of the number of publics has been shrinking. I think you’re likely going to see more potential mergers in the public sphere than you’re going to see new IPOs, in my opinion.

While [the Permian] is still very early in its life, as it goes to full development the finiteness of that inventory has created interesting opportunities for us.

Really, we were a later entrant to the Permian—which meant on one hand, we didn’t buy something and make 10x on it. But on the other hand, we didn’t buy something and get a donut. It meant that we had a lot more well control and surety and data to make sure we weren't going to do something inordinately stupid.

We really focused on New Mexico. It has benefits from a land perspective in terms of forced pooling that are good for a non-operator. It has the consistency that we see in the Williston and in the Midland Basin but with the higher pressures and returns that you typically see in the Delaware. It is more expensive to drill and more variable, say, than the Midland.

But what that has meant is finding the right operating partners to attack inventory is critical: whether it be Vital and their path for Forge, which was critical, or Novo. We both had a ton of existing land around the Novo acreage, as did Earthstone.

So, we felt that both were the logical party. Earthstone in particular should have some synergistic effects on cost given their existing operations in the area.

CM: You mentioned gas properties—what’s the appetite like to acquire more gas-weighted assets?

NO: The things that concern us about gas… The contango in the strip has the industry not reacting to a pretty hard down move than it should, in our opinion, which could potentially mean that it drags on a period of lower prices longer.

I think people are, very rightfully so, excited about a material uptick in export capacity for global gas demand for the United States, and I think those are valid points. I think what concerns me personally is that if the U.S. supply is not reacting to current pricing at all, are you effectively building that inventory of gas in advance of that? It’s been very hot this summer, which I think has kind of softened the blow of what you might have otherwise seen.

But I have not seen producers react, and they're drilling through it to some degree. That gives me a little bit of pause medium term versus people’s expectations. It’s like everybody is pivoting for something that may not come because they’re all pivoting towards it.

Longer term, I think that gas has a very bright future. It’s a lot easier for Adam and I to evaluate gas properties in a more normalized environment than it was last year when it was $6 or $8, the highest prices in a decade. It's very hard to want to buy things during that period.

I think that there is still long-life inventory in gas. I think the Haynesville is a phenomenal play at a certain price. It is also one of the older gas shale plays, relative to its overall physical size. So I think the inventory, it's maybe not in the eighth inning, but it's not in the third inning anymore, that's for sure.

The challenge there is that, effectively, anything you work to develop or do in the short to medium term is likely a money-losing proposition. Really, it would be a target towards the longer term.

Appalachia, I would say some of the core areas have largely been developed at this time, but it is a massive land footprint. We own one of the less developed areas, and I think we've got 20 years of inventory on our own asset. I think we bought the asset for that option.

AD: When you saw $7, $9 gas, you had a massive bid-ask spread. Now, you’ve kind of slipped that on its head and you still have a bid-ask spread that you could drive a truck through. So, I think we’ll continue to stay disciplined and opportunistic.

To your question about looking out of basins, we continue to keep our ear to the ground with the Haynesville, the Eagle Ford and a number of other different basins.

But those are generally going to be higher-bar areas for us to expand in, especially if you look at it from a relative perspective with the opportunities that we see within the Permian, within the Williston, within the Marcellus. We can continue to bolt-on properties there—and we will, if there’s an opportunity that we can’t pass up because of the return thresholds.

In an outside basin, that’s definitely something we’ll also take a hard look at.

Recommended Reading

Sangomar FPSO Arrives Offshore Senegal

2024-02-13 - Woodside’s Sangomar Field on track to start production in mid-2024.

NAPE: Chevron’s Chris Powers Talks Traditional Oil, Gas Role in CCUS

2024-02-12 - Policy, innovation and partnership are among the areas needed to help grow the emerging CCUS sector, a Chevron executive said.

CNOOC Makes 100 MMton Oilfield Discovery in Bohai Sea

2024-03-18 - CNOOC said the Qinhuangdao 27-3 oilfield has been tested to produce approximately 742 bbl/d of oil from a single well.

TPH: Lower 48 to Shed Rigs Through 3Q Before Gas Plays Rebound

2024-03-13 - TPH&Co. analysis shows the Permian Basin will lose rigs near term, but as activity in gassy plays ticks up later this year, the Permian may be headed towards muted activity into 2025.

Proven Volumes at Aramco’s Jafurah Field Jump on New Booking Approach

2024-02-27 - Aramco’s addition of 15 Tcf of gas and 2 Bbbl of condensate brings Jafurah’s proven reserves up to 229 Tcf of gas and 75 Bbbl of condensate.