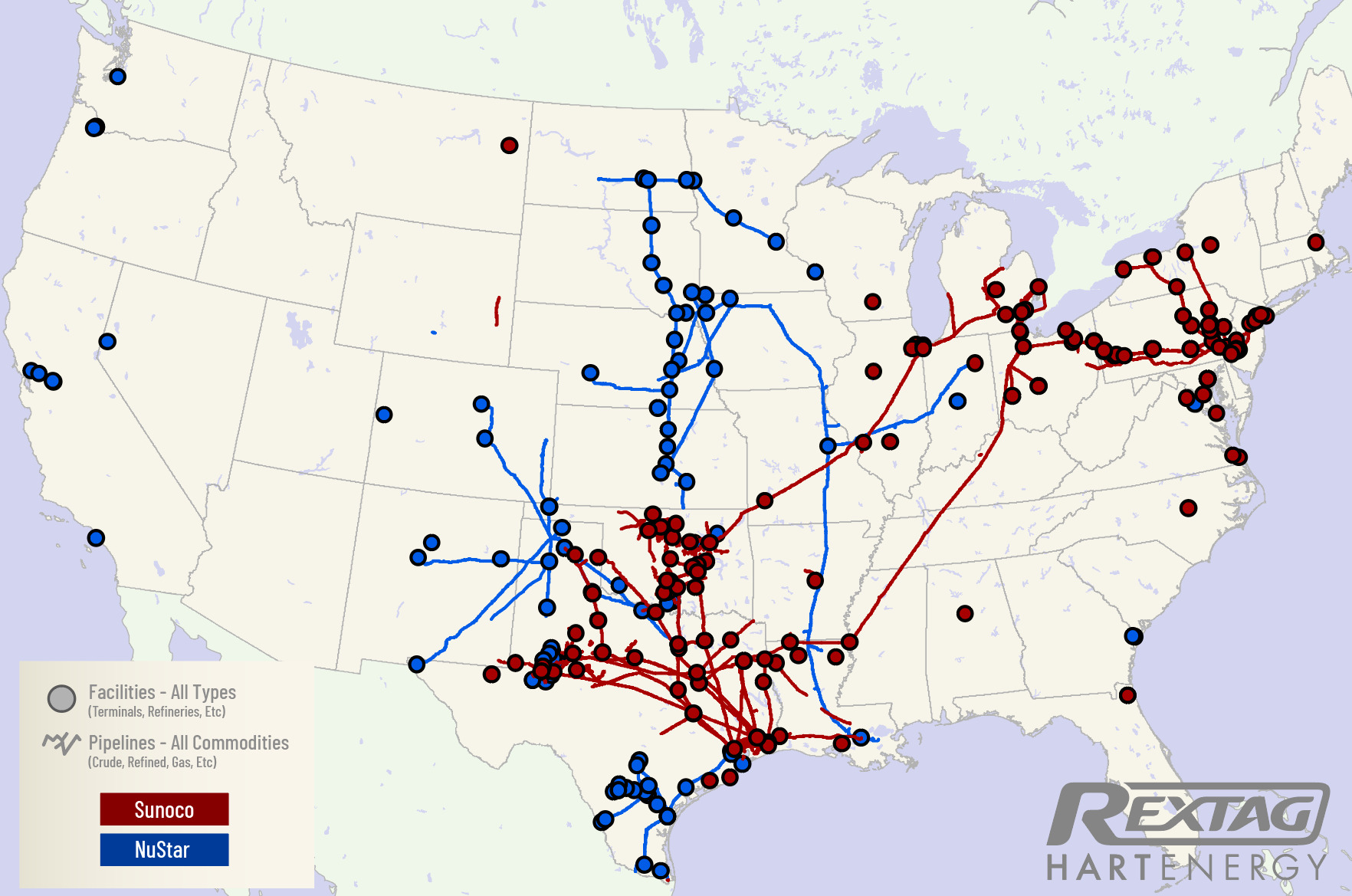

Energy Transfer-controlled Sunoco’s acquisition of NuStar Energy expands the large fuel distribution business with greater scale, but also branches out Sunoco into the crude oil midstream space with a strong Permian Basin footprint.

Sunoco agreed Jan. 22 to acquire NuStar in an all-equity deal valued at $7.3 billion with debt. The deal prices NuStar at nearly $3 billion, not counting debt.

Because of NuStar’s sizable crude oil business, the MLP merger seemingly makes it only a matter time before parent Energy Transfer decides to roll up Sunoco, including NuStar, in the continued consolidation of MLPs, said Hinds Howard, portfolio manager at CBRE Investment Management.

“These are [crude] assets that make more sense with Energy Transfer,” Howard said in an interview. “I think over time it will happen. These [NuStar] assets moving to Sunoco make a roll up make more sense.”

Howard said Energy Transfer attempted to directly acquire NuStar in the past, and that the Sunoco units likely offered the “best currency” to get the deal across the finish line.

Because Energy Transfer is an oil and gas giant with the third-largest market cap of North American midstream players, the deal could face more regulatory scrutiny.

But Scott Grischow, Sunoco’s treasurer and senior vice president of finance, said in an analyst call that the partnership is optimistic the deal will face few hurdles by the Federal Trade Commission in order to close.

“If you take a look at the combined assets of our organization, they’re very complementary in that there’s very little geographic or market overlap that you may typically see in mergers that have historically been of interest to the commission,” Grischow said.

NuStar founder Bill Greehey stepped down from the chairman role in late 2022, so maybe the timing was right to sell, according to analysts.

“NuStar is a really stable and mature MLP,” Howard said.

Amid an ongoing wave of MLP mergers and rollups in recent years, the deal leaves the industry with only 13 notable remaining MLPs, Howard said. Sunoco and NuStar combine the seventh and eighth-largest MLPs by market cap.

Permian power and more

NuStar’s Permian crude oil system currently moves about 540,000 bbl/d, according to NuStar, helping take crude volumes to refining and export hubs, including along the Texas Gulf Coast and Louisiana.

But crude oil still makes up less than half of NuStar’s overall business.

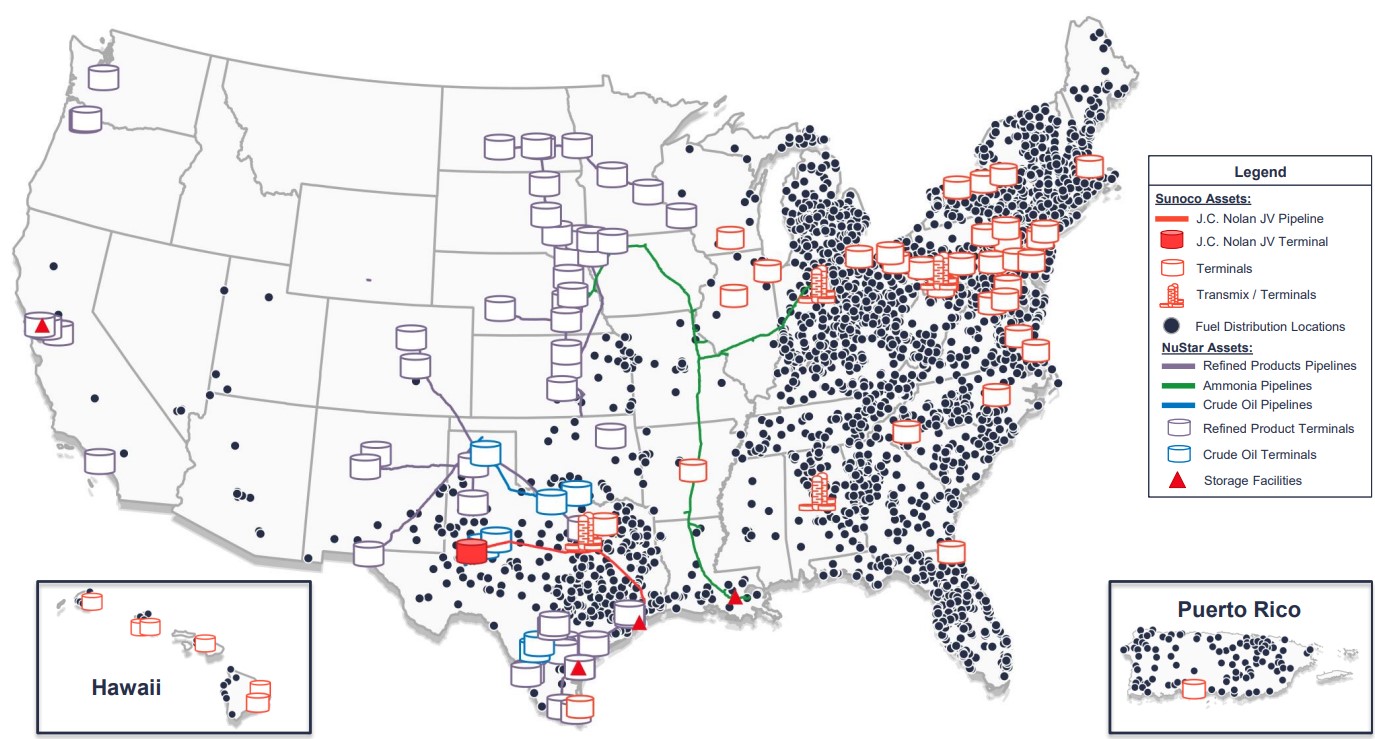

NuStar has approximately 9,500 miles of pipeline and 63 terminal and storage facilities that hold and distribute crude oil, refined products, renewable fuels, ammonia and specialty liquids. The combined system counts 49 MMbbl of storage capacity at its facilities in North America.

Sunoco executives said they expect the deal to be 10% accretive to distributable cash flow per LP unit by the third year after closing. The partnership anticipates realizing at least $150 million in cost-saving synergies by that point.

Sunoco said it has secured a $1.6 billion bridge term loan to refinance NuStar’s high-cost floating rate capital. NuStar’s market cap closed on Jan. 19 at $2.27 billion. Sunoco said the implied premium on the purchase is about 24% based on the volume-weighted average pricing over 30 days.

The partnership aims to achieve a leverage target of 4.0x within 12 to 18 months of closing, which is expected to occur during the second quarter.

Earlier in January, Sunoco agreed to sell 204 convenience stores to 7-Eleven for about $1 billion, indirectly helping to finance the all-stock NuStar deal. The convenience stores are primarily located in West Texas, New Mexico and Oklahoma.

The partnership expects to generate net proceeds of approximately $750 million from the asset sale, which will be used to materially reduce debt, said Sunoco CEO Joseph Kim during the Jan. 22 call with analysts.

“The pro forma company’s metrics would reflect variables that are very similar to investment-grade companies,” he said.

Fitch Ratings affirmed Sunoco’s long-term issuer default rating at BB+ with a “stable outlook” following the deal announcement.

“Fitch believes the acquisition of NuStar will improve [Sunoco’s] business risk profile through an increase in geographic and business line diversity,” Fitch stated.

NuStar will contribute crude and refined products terminals, as well as fuel and oil pipelines, a large ammonia pipeline and exposure to renewable fuels on the West Coast.

Of the pro-forma EBITDA, approximately 45% will come from fuel distribution, 25% from crude oil and 25% from refined products, with the balance from other services, Fitch noted, citing better balance and business line diversity going forward.

RELATED

Sunoco to Acquire NuStar Energy for $7.3B

M&A strategy

Sunoco’s deal with NuStar represents a similar strategy to several of Sunoco’s other recent acquisitions.

Take Sunoco’s 2021 acquisition of NuStar’s East Coast U.S. terminal assets for $250 million for example, said Sunoco COO Karl Fails: Sunoco was able to take its own East Coast fuel distribution business and couple it with NuStar’s expanded midstream presence in the area.

“You get benefits going both ways. Having the fuel distribution business helps keep your midstream assets more full,” Fails said. “And often the midstream assets provide a foundation for additional growth or supply synergies on the fuel distribution side.”

After closing the East Coast asset deal, Sunoco was able to stand up a gasoline blending business out of NuStar’s terminal in Linden, New Jersey—another example of creating new value for the combined business, Fails said.

Sunoco also aims to scale up its fuel distribution presence in the western Midwest—where the partnership doesn’t have a huge footprint—using NuStar’s existing asset base in the region.

Last year, Sunoco bought 16 refined product terminals from Zenith along the East Coast and in the Midwest for $110 million.

The NuStar takeover also expands Sunoco into new business lines, including crude oil pipelines. NuStar operates approximately 2,100 miles of crude pipelines in Texas and Oklahoma.

The transaction will also deliver Sunoco around 2,000 miles of pipeline to transport ammonia, another new business line for the partnership.

While these segments will be new to Sunoco’s portfolio, they do have ties to the refined products business with which the partnership is already quite familiar, said Grischow.

“We follow those markets closely and are excited to have assets that are going to be able to provide value for a broader customer base, moving a broader suite of product,” Grischow said.

RELATED

Energy Transfer to Acquire Crestwood Equity Partners for $7.1 Billion

Sunoco ties run deep

Energy Transfer acquired Sunoco back in 2012 for $5.3 billion. Today, Energy Transfer controls all of the incentive distribution rights (IDRs) of Sunoco, but Sunoco has remained independently traded.

Energy Transfer cofounder and executive chairman Kelcy Warren led the acquisition of Sunoco to expand the business, but he said in a recent interview that it also held stronger sentimental ties.

After all, Warren’s father was a longtime, loyal Sunoco employee in East Texas.

“It was just unbelievably rewarding,” Warren said. “It’s never the reason a business person should ever do an acquisition. If it has sentimental value to you, then never, ever. But, in this case, yeah, it had that, but it was also a fabulous acquisition for our unitholders. But it was a big deal. Big deal for me.”

Recommended Reading

Initiative Equity Partners Acquires Equity in Renewable Firm ArtIn Energy

2024-04-26 - Initiative Equity Partners is taking steps to accelerate deployment of renewable energy globally, including in North America.

Energy Transition in Motion (Week of April 26, 2024)

2024-04-26 - Here is a look at some of this week’s renewable energy news, including the close of a $1.4 billion decarbonization-focused investment fund.

No Silver Bullet: Chevron, Shell on Lower-carbon Risks, Collaboration

2024-04-26 - Helping to scale lower-carbon technologies, while meeting today’s energy needs and bringing profits, comes with risks. Policy and collaboration can help, Chevron and Shell executives say.

Solar Sector Awaits Feds’ Next Move on Tariffs

2024-04-25 - A group of solar manufacturers want the U.S. to impose tariffs to ensure panels and modules imported from four Southeast Asian countries are priced at fair market value.

Solar Panel Tariff, AD/CVD Speculation No Concern for NextEra

2024-04-24 - NextEra Energy CEO John Ketchum addressed speculation regarding solar panel tariffs and antidumping and countervailing duties on its latest earnings call.