The all-equity transaction, which includes the assumption of $3 billion of Crestwood debt, adds infrastructure in the Williston and Delaware basins and also provides Energy Transfer with an entry into the Powder River Basin. (Source: Shutterstock.com)

Energy Transfer LP said on Aug. 16 it will acquire Crestwood Equity Partners LP in an all-stock merger valued at $7.1 billion, the latest midstream sector megadeal this year.

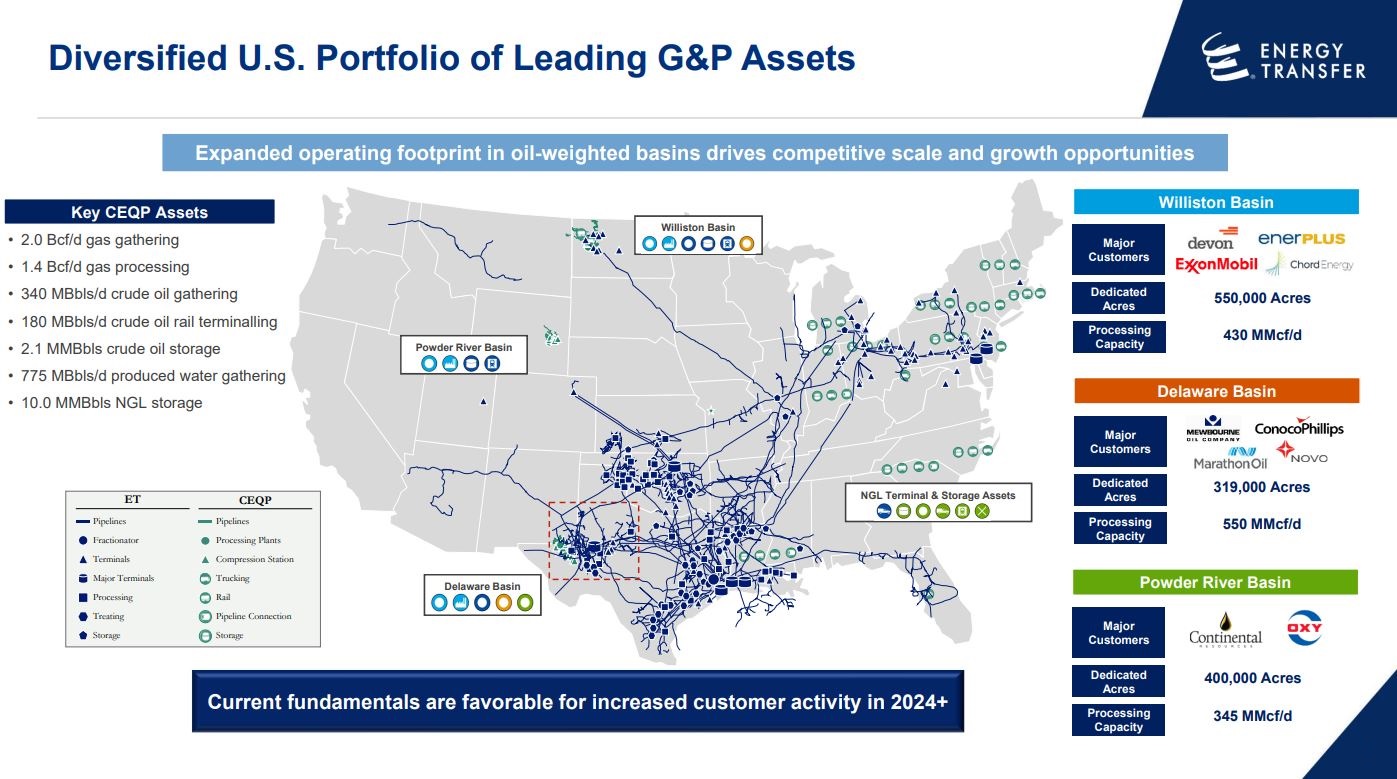

Crestwood’s system includes gathering and processing assets located in the Williston, Delaware and Powder River basins. Crestwood’s assets comprise approximately 2 Bcf/d of gas gathering capacity, 1.4 Bcf/d of gas processing capacity and 340,000 bbl/d of crude gathering capacity.

“If consummated, this transaction would extend Energy Transfer’s position in the value chain deeper into the Williston and Delaware basins while also providing entry into the Powder River basin,” Energy Transfer said in an Aug. 16 press release.

The assets are expected to complement Energy Transfer’s downstream fractionation capacity at Mont Belvieu, as well as its hydrocarbon export capabilities from both its Nederland Terminal in Texas and the Marcus Hook Terminal in Philadelphia.

Energy Transfer said the bolt-on is also expected to provide benefits to the company’s NGL and refined products and crude oil businesses with the addition of strategically located storage and terminal assets, including approximately 10 MMbbl of storage capacity, as well as trucking and rail terminals. The systems are anchored by predominantly investment-grade producer customers with firm, long-term contracts and significant acreage dedications.

Energy Transfer’s deal includes the assumption of Crestwood’s $3.3 billion in debt but the Energy Transfer said the described the acquisition as a “credit neutral bolt-on.” Under the terms of the agreement, Crestwood common unitholders will receive 2.07 Energy Transfer common units for each Crestwood common unit based on unit prices on Aug. 15. The transaction is expected to close in fourth-quarter 2023, subject to the approval of Crestwood’s unitholders, regulatory approvals and other customary closing conditions.

Upon closing, Crestwood common unitholders are expected to own approximately 6.5% of Energy Transfer’s outstanding common units.

Energy Transfer also expects to achieve at least $40 million of annual run-rate cost synergies before additional benefits of financial and commercial opportunities. The transaction is anticipated to provide Crestwood unitholders a benefit to distributions per unit and an opportunity to participate in Energy Transfer’s targeted annual distribution per unit growth rate of 3% to 5%.

BofA Securities acted as sole financial adviswr to Energy Transfer and Kirkland & Ellis LLP acted as legal counsel. Intrepid Partners LLC and Evercore acted as financial adviswrs to Crestwood and Vinson & Elkins LLP acted as legal counsel.

RELATED: ONEOK to Acquire Magellan Midstream Partners for $18.8 Billion

Recommended Reading

Kimmeridge Fast Forwards on SilverBow with Takeover Bid

2024-03-13 - Investment firm Kimmeridge Energy Management, which first asked for additional SilverBow Resources board seats, has followed up with a buyout offer. A deal would make a nearly 1 Bcfe/d Eagle Ford pureplay.

M4E Lithium Closes Funding for Brazilian Lithium Exploration

2024-03-15 - M4E’s financing package includes an equity investment, a royalty purchase and an option for a strategic offtake agreement.

Laredo Oil Subsidiary, Erehwon Enter Into Drilling Agreement with Texakoma

2024-03-14 - The agreement with Lustre Oil and Erehwon Oil & Gas would allow Texakoma to participate in the development of 7,375 net acres of mineral rights in Valley County, Montana.

California Resources Corp. Nominates Christian Kendall to Board of Directors

2024-03-21 - California Resources Corp. has nominated Christian Kendall, former president and CEO of Denbury, to serve on its board.

Uinta Basin: 50% More Oil for Twice the Proppant

2024-03-06 - The higher-intensity completions are costing an average of 35% fewer dollars spent per barrel of oil equivalent of output, Crescent Energy told investors and analysts on March 5.