ONEOK Inc. and Magellan Midstream Partners LP are combining to create a midstream giant with an enterprise value of $60 billion.

ONEOK will acquire all of Magellan Midstream’s outstanding units in a cash-and-stock transaction valued at $18.8 billion, including assumed debt, the companies announced on May 14.

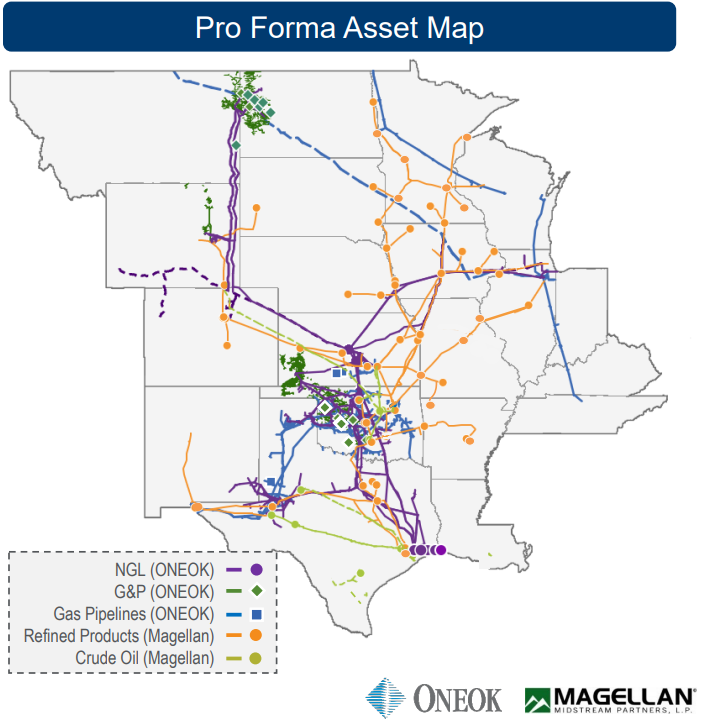

The deal will deliver ONEOK a primarily fee-based refined products and crude oil transportation business to complement its NGL infrastructure system.

“The deal is one of, if not the largest U.S. midstream deal we have seen in the past few years,” Truist Securities analysts wrote in a May 14 note.

Under the terms of the agreement, ONEOK will pay $25 in cash and 0.6670 shares of ONEOK common stock for each outstanding Magellan common unit.

The implied value to each Magellan unitholder of $67.50 per unit represents a 22% premium to the company’s closing price on May 12, ONEOK said in a press release.

Current ONEOK shareholders are expected to own approximately 77% of the company pro forma, with current Magellan unitholders owning the remaining 23%, according to an investor presentation.

ONEOK said it has secured $5.25 billion in committed bridge financing for the cash consideration of the proposed deal. ONEOK will also assume about $5 billion of existing net debt to acquire Magellan.

Magellan will be merged into a wholly-owned subsidiary of ONEOK upon closing, which is expected in the third quarter.

“The combination of ONEOK and Magellan will create a diversified North American midstream infrastructure company with predominately fee-based earnings, a strong balance sheet and significant financial flexibility focused on delivering essential energy products and services to our customers and continued strong returns to investors,” said Pierce H. Norton II, president and CEO at ONEOK.

Scaling up

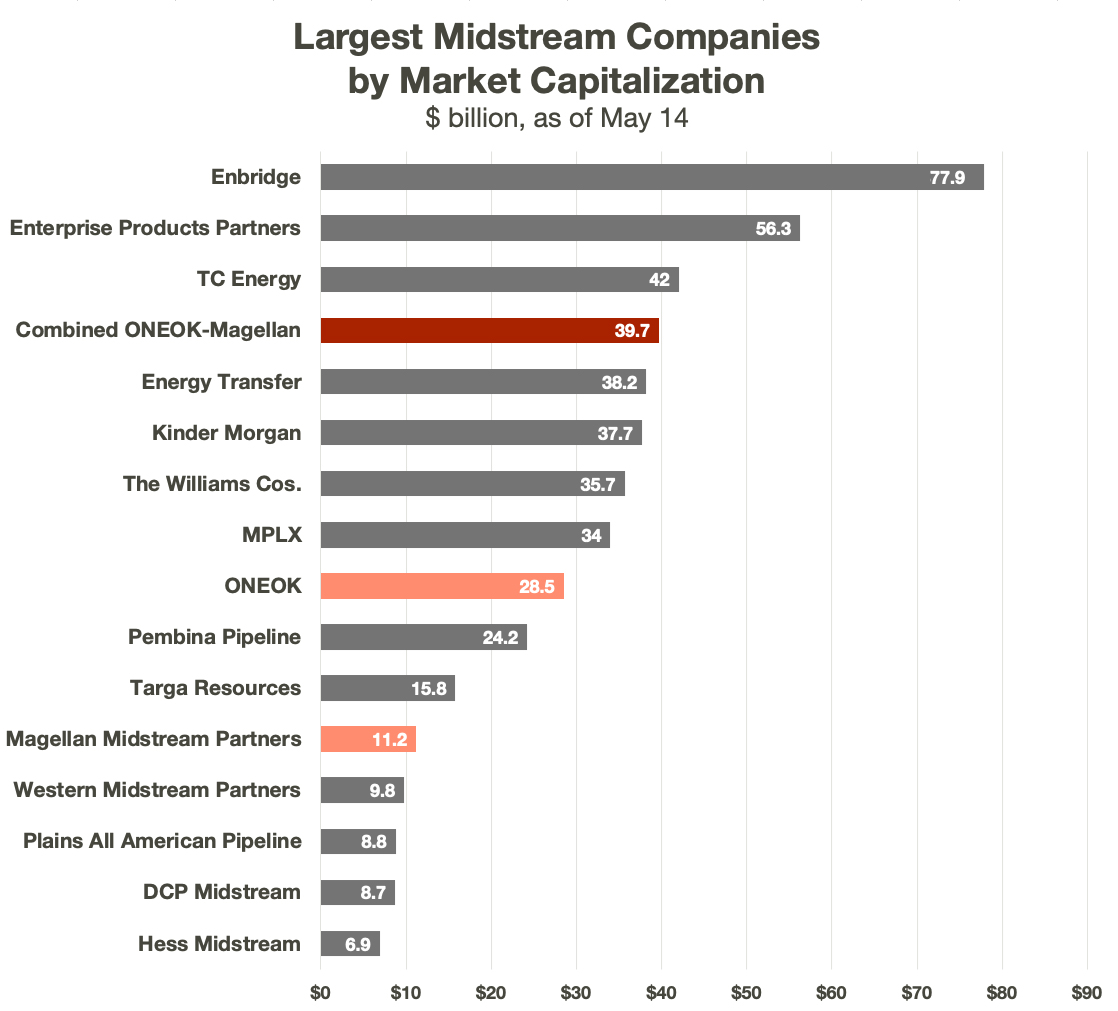

The merger would create a midstream behemoth with combined market capitalization of about $40 billion, larger than all public companies in the space except for Enbridge, Enterprise Products Partners and TC Energy.

The post-merger entity will own more than 25,000 miles of liquids-oriented pipelines, as well as significant assets in the Gulf Coast and Midcontinent markets.

“The transaction, including assumed debt and equity considerations, represents a 12.7x LTM EBITDA multiple,” Truist analysts said. “As seen by the recent historical acquisitions in the industry below, 12.7x is in-line to below many of the average multiples seen for this kind of transaction in terms of size and magnitude but also in adding scope and scale.”

ONEOK anticipates that the merger will position it to better take advantage of export opportunities, the company said in the press release. The result of the transaction has the potential to create annual synergies of more than $400 million within the next two to four years.

From an operational standpoint, the companies’ complementary assets could result in the company hitting at least $200 million in operational synergies once the companies become fully integrated, according to Truist.

ONEOK’s Norton will continue to serve as CEO of the combined company after the deal closes. ONEOK also plans to nominate one of two directors to serve on the board of Magellan’s general partner.

The combined company will continue to be headquartered in Tulsa, Oklahoma, where both companies are located.

The deal is expected to be accretive on an earnings-per-share basis starting in 2024; EPS accretion is expected to range between 3% and 7% per year from 2025 through 2027, ONEOK said. The company expects to see at least $200 million in savings through synergies per year.

RELATED: Targa, EnLink, ONEOK Building Out in a Hurry

Permian bottleneck

Truist analysts viewed the deal as largely positive “given the relatively low valuation versus recent deals and the potential earnings growth profile of the assets all while maintaining largely solid financial.”

“We expect the pro-forma company to be able to de-lever toward its 3.5x [leverage] target in relative short order though the time to reach the debt goal could be extended in order to prioritize capital allocation toward growth projects, particularly the likely debottlenecking capacity hiccups in the Permian region,” Truist analysts Neal Dingmann and Bertrand Donnes wrote in a May 14 note. “While OKE buying MMP is one of the first large midstream transactions we have seen in several quarters, we note that Plains All American Pipeline … has similar assets to OKE and trades at an attractive multiple potentially setting the company up as next to be bought.

The analysts said the merger will give the combined company strong assets across key basins.

“We view ONEOK as well positioned for the deal given its prior substantial de-levering, providing strong balance sheet capacity,” the analysts said. “The new assets appear to add more scope than scale: Magellan brings crude oil and refined products expertise to ONEOK while ONEOK’s core operations are within gas pipelines, NGLs and natural gas G&P.”

Recommended Reading

TC Energy’s Keystone Back Online After Temporary Service Halt

2024-03-10 - As Canada’s pipeline network runs full, producers are anxious for the Trans Mountain Expansion to come online.

Post $7.1B Crestwood Deal, Energy Transfer ‘Ready to Roll’ on M&A—CEO

2024-02-15 - Energy Transfer co-CEO Tom Long said the company is continuing to evaluate deal opportunities following the acquisitions of Lotus and Crestwood Equity Partners in 2023.

Waha NatGas Prices Go Negative

2024-03-14 - An Enterprise Partners executive said conditions make for a strong LNG export market at an industry lunch on March 14.

Pembina Pipeline Enters Ethane-Supply Agreement, Slow Walks LNG Project

2024-02-26 - Canadian midstream company Pembina Pipeline also said it would hold off on new LNG terminal decision in a fourth quarter earnings call.

TC Energy's Keystone Oil Pipeline Offline Due to Operational Issues, Sources Say

2024-03-07 - TC Energy's Keystone oil pipeline is offline due to operational issues, cutting off a major conduit of Canadian oil to the U.S.