Breakeven prices to profitably drill new wells in the Permian Basin continue to rise, according to the Dallas Fed—but the fields around Midland, Texas, have the lowest drilling costs in the area. (Source: Shutterstock)

The Dallas Fed led with the bad news first: breakeven prices to profitably drill in the Permian Basin continue to rise.

The good news is nearly everyone is making money in the current oil price environment.

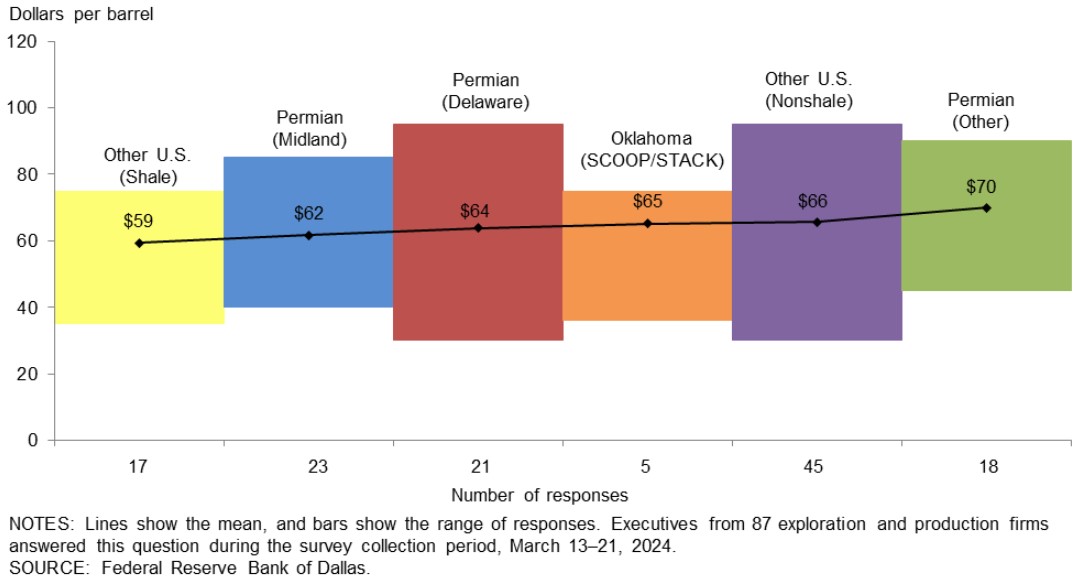

U.S. producers need an average $64/bbl WTI price to profitably drill new wells, according to the Dallas Fed’s first-quarter energy survey, which measures the sentiments of around 200 oil and gas firms across Texas, southern New Mexico and northern Louisiana.

That’s up from an average $62/bbl WTI price needed a year ago when the Dallas Fed last posed the question to industry executives.

Drilling costs and breakeven levels vary across basins. In the Permian—the nation’s top crude oil-producing region—breakeven prices average $65/bbl, an increase of $4/bbl year over year.

And breakeven prices vary even within different parts of the Permian itself. Costs are lowest in the Midland Basin, where breakeven prices average $62/bbl.

Breakeven prices move up in the Permian’s Delaware Basin ($64/bbl WTI average), which extends from West Texas into southeastern New Mexico.

In other areas of the Permian—the Central Basin Platform and extensional, fringier parts of the play—breakeven prices to turn a profit average $70/bbl.

Scale also matters when it comes to drilling profitable wells. Larger producers, with crude oil output of 10,000 bbl/d or more, required an average $58/bbl WTI price to drill.

Smaller producers that fall below 10,000 bbl/d of crude output need an average $67/bbl WTI price to economically drill.

But with WTI spot prices averaging $82.52/bbl during the survey period, “almost all firms in the survey can profitably drill a new well at current prices,” the Dallas Fed reported.

The need for scale, both on the balance sheet and in inventory depth, is fueling a red-hot dealmaking market in the U.S. upstream space.

The relatively low-cost Midland Basin is attracting huge amounts of attention from E&Ps large and small. Exxon Mobil’s $64.5 billion acquisition of Pioneer Natural Resources will yield one of the largest landowners and oil producers in the Midland Basin.

Two other major Midland producers were also recently snapped up: Endeavor Energy Resources was acquired by Diamondback Energy for $26 billion, while CrownRock LP was carved out by Occidental Petroleum for $12 billion.

“The difference in the breakevens between large and small firms potentially highlights the benefits of economies of scale in the oilfield,” Dallas Fed Senior Business Economist Kunal Patel said in a March 27 media briefing, “as it allows more contiguous acreage positions and the ability to better negotiate rates with service firms and suppliers.”

RELATED

ONEOK CEO: ‘Huge Competitive Advantage’ to Upping Permian NGL Capacity

Gassed up

Oil producers are still working within a healthy band of commodity prices to profitably drill new wells. The same can’t be said for all U.S. natural gas E&Ps.

Survey respondents continued to lament the current cycle of low prices befalling U.S. natural gas producers.

Henry Hub spot prices averaged $1.44/MMBtu during the survey collection period. February’s Henry Hub average of $1.72/MMBtu was an inflation-adjusted record low, according to the U.S. Energy Information Administration.

Oversupplied storage inventories and relatively mild winter weather across the U.S. have contributed to the depressed prices. But another major culprit for the sticky low prices is record-high volumes of gas associated with drilling oil wells—often referred to as associated gas.

The challenges facing the natural gas space have operators rethinking where they allocate their spending.

“Crude oil markets have continued to be constructive,” one anonymous survey respondent commented. “We have decreased capital investments in our natural gas portfolio and increased capital investments in our oil portfolio.”

“Natural gas is currently pricing at or below costs of production,” another respondent said.

But producers continue to be bullish on the future gas macro: Survey respondents expect Henry Hub prices to average $2.59/MMBtu by the end of 2024. Two years from now, producers expect spot prices of $3.18/MMBtu.

RELATED

EIA: Blame Associated Gas Volumes for Sticky Low NatGas Prices

Pause for concern?

The Biden administration’s move in late January to pause certification of new U.S. LNG export terminals drew condemnation from some survey respondents. Other producers and analysts aren’t so worried about the effect of the pause on the long-term LNG market.

“The LNG export pause effect is difficult to forecast several years into the future as both demand, supply and commodity pricing can all change,” one respondent said.

But survey respondents generally blasted what they view as “virtue signaling” and “pandering” by the administration during an election year.

And the pause could have broader implications on future domestic gas production, according to the Dallas Fed.

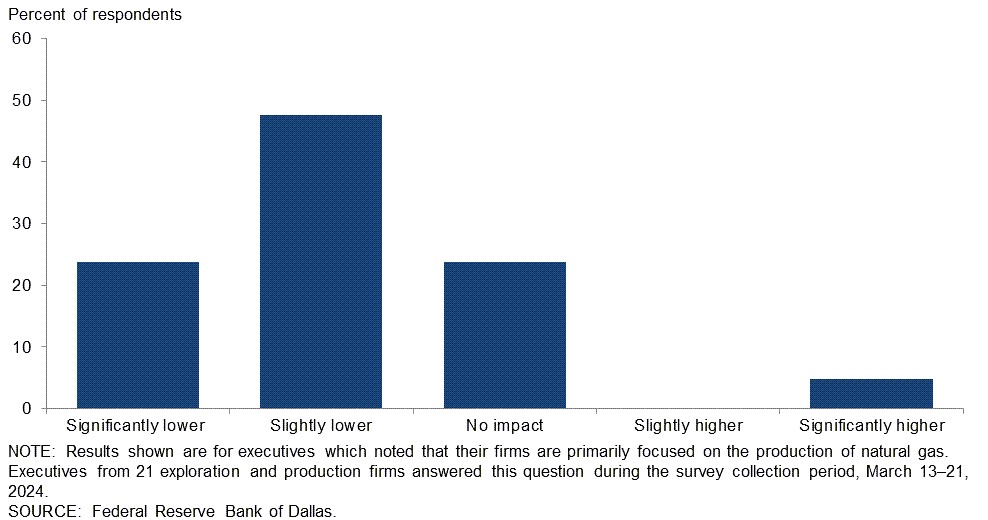

Among E&P respondents primarily focused on gas production, 48% expect their firm’s gas output five years from now to be slightly lower than their expectations before the pause was announced.

Another 24% expect their gas production to be significantly lower than their pre-pause expectations, while 24% expect no impact from the pause.

U.S. Energy Secretary Jennifer Granholm, speaking during the CERAWeek by S&P Global conference earlier this month, suggested the certification pause “will be well in the rearview mirror” a year from now.

“Our no-impact answer to the LNG pause question assumes that the pause is lifted within the next year,” a respondent said. “With a longer pause or a future ban, we would expect a negative impact to U.S. natural gas pricing.”

RELATED

CERAWeek: Energy Secretary Defends LNG Pause Amid Industry Outcry

Recommended Reading

CAPP Forecasts $40.6B in Canadian Upstream Capex in 2024

2024-02-27 - The number is slightly over the estimated 2023 capex spend; CAPP cites uncertain emissions policy as a factor in investment decisions.

Air Liquide to Add CO2 Recycling at Plant in Germany

2024-02-08 - In a supply agreement, Air Liquide and Dow plan to add a new CO2 recycling solution to two air separation units and one partial oxidation plant.

1 Fatality in Equinor Helicopter Training Accident Offshore Norway

2024-02-29 - Equinor employee died following the helicopter accident, the cause of which has not been reported.

Equinor Resumes Helicopter Flights on NCS Following Fatal Accident

2024-03-01 - Operator also announced it is expanding its helicopter fleet by 15 through contracts with Bell and Leonardo, with the first two helicopters slated for delivery in about a year.

Coalition Launches Decarbonization Program in Major US Cities, Counties

2024-04-11 - A national coalition will start decarbonization efforts in nine U.S. cities and counties following a federal award of $20 billion “green bank” grants.