A supply glut of LNG could result in a queue of floating cargos riding the waves as European storage fills and Asian demand lags, according to a report by Bernstein analysts.

“In the worst case, this would lead to a backup of LNG/gas to the U.S.,” Bernstein analyst Jean Ann Salisbury said in a July 11 report, “Will LNG be Stuck at Sea?”

“There has been significant interest and concern in whether there is a one-to-three-month ‘chaotic period’ in gas this summer due to [first] European storage filling well before the normal October period and [second] Asian demand being unable to redirect and absorb more gas that quickly,” Salisbury said.

At the same time, U.S. natural gas production reportedly reached a record 103 Bcf in June, though Goldman Sachs said the increase was driven by a sharp rise in Permian Basin volumes that analyst Samantha Dart suggested could be revised lower.

Last month, Morgan Stanley warned that U.S. LNG exporters could see cargo cancellations in the second half of 2023 amid strong European gas injections.

RELATED

Morgan Stanley: US LNG Exporters Could See Cargo Cancellations

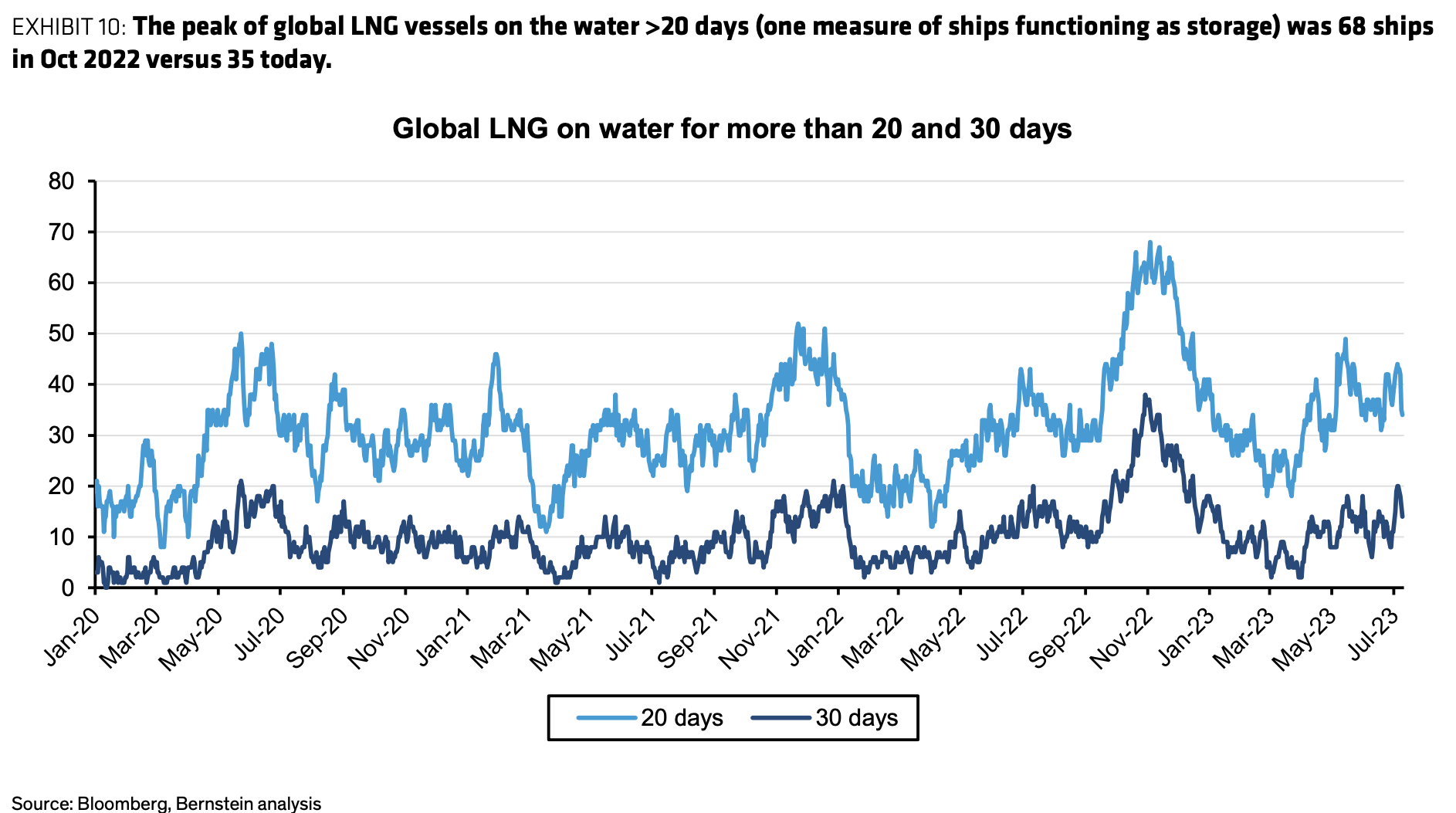

Approximately 35 LNG ships have been sitting on the water for more than 20 or 30 days. This compares to a peak of 68 ships in Oct. 2022, Salisbury said, but she added that even with this record number of ships, there was no back up to the U.S.

“To see vessels wait for a month, we need the inter-month price difference to exceed the value of shipping another cargo to Asia for 1 month, (it takes 2 months to go to Asia and back, so half the arb can be achieved in 1 month), which is ~$6/Mcf going into winter,” according to the Bernstein report.

Such a rise in the number of ships on the water functioning as storage wouldn’t be good for U.S. gas prices, Salisbury said.

“Normally, we assume $2/MMBtu as a sustained floor for Henry Hub, which has held for one month [plus] periods in the past, and is driven by the high lifting cost of old verticals,” Salisbury stated. “But given the already high storage levels and the speed at which this would unfold, we think U.S. gas could go into the mid $1s for a month or two (lowest one-month price in recent memory was $1.6/Mcf).”

Two main drivers to watch

Bernstein sees two main drivers to watch for this year: storage levels, especially in Europe, and Asia’s appetite to absorb more LNG cargos.

In Europe last year, prices skyrocketed amid Russia’s invasion of Ukraine. European markets were willing to pay high prices to secure LNG cargo amid wartime supply disruptions. More than a year after the war began, European gas inventories are near the five-year high and on track to fill up soon following a warm winter globally and weak year-to-date industrial demand.

Likewise, storage levels in the U.S., Japan and Korea are also well above the five-year averages for the same reasons, Bernstein said.

The second relates to “the waiting arb,” as Bernstein calls it.

The waiting arbitrage depends on the month-to-month uptick in prices required to make waiting on the water for a month worthwhile—versus delivering and returning to reload. That price is now around $6/MMbtu (in one month). Currently, the October to November arb is only $3/MMbtu,” Bernstein said.

“So, said another way, if Asia cannot pivot quickly enough to absorb more gas (our base case is still that they can), we would expect to see September/October TTF [Dutch Title Transfer Facility] fall to $10/Mcf and November to remain at $16/Mcf (i.e. the $6/MMbtu one-month waiting fee). This is more or less what happened last year on a smaller scale,” Salisbury wrote.

U.S. LNG supply, Permian revisions

Rystad Energy views U.S. LNG supply as robust but foresees some export declines emerging due to possible issues at Cheniere Energy’s Sabine Pass Train 3, the company said in a July 12 report. In Asia, LNG spot prices for August delivery are around $11/MMbtu.

“This has incentivized some players with U.S. free-on-board LNG cargoes to direct their LNG towards Asia rather than Europe,” Rystad said. “However, finding Asian importers may be difficult as some countries still face high inventory, subject to demand fluctuation during summer.”

U.S. gas production recently reached 103 Bcf for a few days in June, according to Wood Mackenzie, owing to rising Permian production after maintenance-related declines in late June, Goldman Sachs said in a July 11 report.

Goldman’s Dart said Permian production could be revised lower due to pipeline take-away capacity issues and limited room for additional exports to Mexico.

“We recently argued that, although the June rally in U.S. gas prices reduced the incentive for coal-to-gas (C2G) substitution, the resulting negative impact on gas demand wasn’t visible in the June data, and would likely unfold in subsequent weeks,” Goldman reported.

Goldman said the lag between a large price move and a visible demand response often happens because utilities opting to switch fuels “might want to wait a bit to test whether the shift in price is persistent.”

And they “typically rely on bid week towards the end of each month to change their gas nominations for the following month.”

Recommended Reading

US Raises Crude Production Growth Forecast for 2024

2024-03-12 - U.S. crude oil production will rise by 260,000 bbl/d to 13.19 MMbbl/d this year, the EIA said in its Short-Term Energy Outlook.

Iraq to Seek Bids for Oil, Gas Contracts April 27

2024-04-18 - Iraq will auction 30 new oil and gas projects in two licensing rounds distributed across the country.

For Sale, Again: Oily Northern Midland’s HighPeak Energy

2024-03-08 - The E&P is looking to hitch a ride on heated, renewed Permian Basin M&A.

E&P Highlights: Feb. 26, 2024

2024-02-26 - Here’s a roundup of the latest E&P headlines, including interest in some projects changing hands and new contract awards.

Gibson, SOGDC to Develop Oil, Gas Facilities at Industrial Park in Malaysia

2024-02-14 - Sabah Oil & Gas Development Corp. says its collaboration with Gibson Shipbrokers will unlock energy availability for domestic and international markets.