Attend an oil and gas conference and you’ll inevitably hear this mantra: “Oil and gas isn’t going anywhere.”

It’s meant to be an affirmation that fossil fuels will continue to be needed for a long time, not a complaint that pipelines have conked out.

Fun fact: It’s true. Oil and gas will continue to be essential for years to come.

Not-so-fun fact: Your oil and gas company might not be around for it.

“Many producers say they will be the ones to keep producing throughout transitions and beyond,” the International Energy Agency (IEA) said in a recent special report on the oil industry in net zero transitions. “They cannot all be right.”

Survival is never guaranteed in a free market, of course. For that matter, it’s not guaranteed in a controlled one, either.

And while a company the size of ConocoPhillips ($132 billion market capitalization) can afford to double down on its embrace of fossil fuels and be the last one standing in the oil patch, others may face a harsher reality if they choose that strategy. Or not.

The problem is getting a realistic handle on what is to come, and that’s not easy.

Mark Finley, fellow in global energy and oil at Rice University’s Baker Institute for Public Policy, likes to begin his presentations by quoting Yogi Berra, legendary catcher for the New York Yankees: “It’s difficult to make predictions, especially about the future.”

There is always a degree of aspiration behind outlooks, Finley told me a few months ago. “You have to consider that when you look at the person producing the forecast.”

Finley, former senior U.S. economist for BP, has spent a chunk of his career as that person. He led production of the “BP Statistical Review of World Energy” for 12 years, was responsible for short- and long-term oil market analysis at BP and contributed key oil market analysis for senior U.S. officials during the Gulf War as an analyst for the CIA.

For the past few decades, folks who have needed to know what’s happening next have saved (or could have saved) a lot of time in meetings by simply asking Finley. So, I asked Finley.

My questions were about the trajectory of oil prices, but he also touched on the nature of outlooks, i.e., they are written by real people.

Case in point: A few years ago, I watched Fatih Birol, executive director of the IEA, swat aside a question from a luncheon attendee who didn’t much care for the numbers he presented on historical oil and gas production.

“I cannot change the data,” Birol said. “It’s not an expectation. It is what has happened.”

Seems straightforward enough, but we all know that statistics are in the eye of the beholder.

“How much of [the analysis] is just objective numbers, and how much is what they want to happen?” Finley asked. “I mean, obviously OPEC would want there to be more oil consumption.”

In the case of the IEA, Birol presents scenarios of what would need to happen to achieve net-zero climate goals, given the stated goal of the Paris Agreement of achieving no more than a 1.5 C rise in global temperature by 2050.

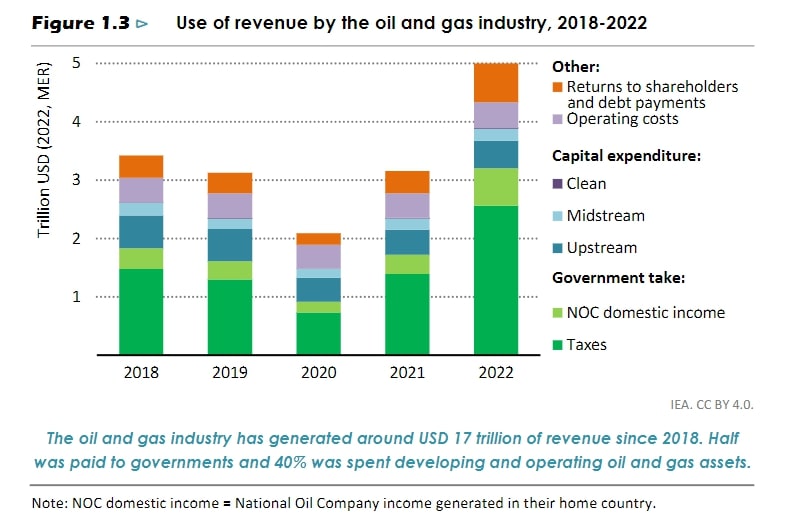

Topping the list: oil and gas companies would need to cut emissions from operations by 60% by 2030 and arrive at near-zero emissions intensity by the early 2040s. That’s not a prediction of what the industry will do, or a dictate of what it must do; it’s what the IEA calculates is a necessary step by the industry to keep the world on track to limit global warming.

But back to survival. “The volatility of fossil fuel prices means that revenues could fluctuate from year to year—but the bottom line is that oil and gas becomes a less profitable and a riskier business as net zero transitions accelerate.”

The IEA’s assessment isn’t all negative.

“Some 30% of the energy consumed in a net zero energy system in 2050 comes from low-emissions fuels and technologies that could benefit from the skills and resources of the oil and gas industry,” the agency says.

It comes down to oil and gas companies either bumping up annual investment in clean energy projects from $20 billion (2.5% of capital spending) to $400 billion (50%)—on top of Scope 1 and 2 emission reduction investments—or sticking with fossil fuels and preparing to wind down operations over time.

That’s a stark choice. Is the IEA correct that a moment of truth is fast approaching? Realistically, the choices to be made are probably going to be somewhere in the middle. The IEA’s scenarios are based on the 195 signers of the Paris Agreement actually adhering to the agreement. The likelihood of that is … c’mon, not a chance.

Which brings us to what happens next.

“The baseline expectation should be for a volatile and bumpy ride,” says the IEA.

Agreed.

Recommended Reading

Tech Trends: Halliburton’s Carbon Capturing Cement Solution

2024-02-20 - Halliburton’s new CorrosaLock cement solution provides chemical resistance to CO2 and minimizes the impact of cyclic loading on the cement barrier.

To Dawson: EOG, SM Energy, More Aim to Push Midland Heat Map North

2024-02-22 - SM Energy joined Birch Operations, EOG Resources and Callon Petroleum in applying the newest D&C intel to areas north of Midland and Martin counties.

Range Resources Expecting Production Increase in 4Q Production Results

2024-02-08 - Range Resources reports settlement gains from 2020 North Louisiana asset sale.

Sinopec Brings West Sichuan Gas Field Onstream

2024-03-14 - The 100 Bcm sour gas onshore field, West Sichuan Gas Field, is expected to produce 2 Bcm per year.

TotalEnergies Restarts Gas Production at Tyra Hub in Danish North Sea

2024-03-22 - TotalEnergies said the Tyra hub will produce 5.7 MMcm of gas and 22,000 bbl/d of condensate.