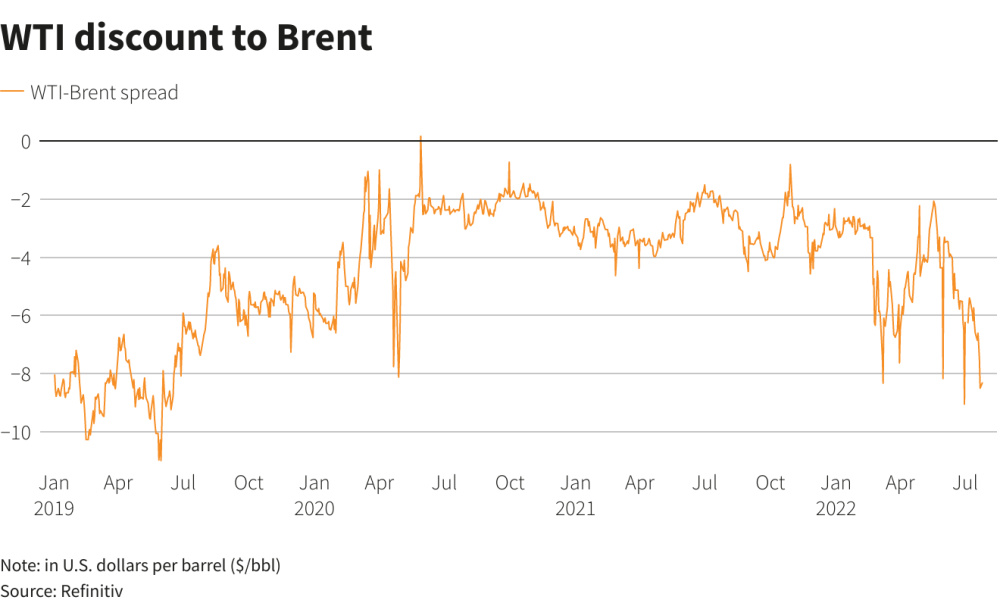

The gap between the two leading crude oil benchmarks has widened to levels not seen since June 2019 as easing gasoline demand in the United States weighs on U.S. crude while tight supply supports the international Brent benchmark.

Brent crude futures closed at an $8.50/bbl premium to WTI crude in the U.S. on July 22, the widest since June 2019 excluding spikes related to contract-expiry dates, Refinitiv data shows.

“Foreign demand for American crude should increase as WTI-linked cargoes become comparatively more attractive,” Stephen Brennock of oil broker PVM said.

The spread is closely watched by U.S. exporters as the wide difference makes U.S. shipments more attractive to global buyers.

“The arb is wide enough for U.S. exports to challenge the all-time record of 4.462 million [barrels per day] from December 2019 as early as this week,” Robert Yawger, director of energy futures at Mizuho in New York, said in a note.

Prices for light sweet grades on the U.S. coast have climbed this week, a signal of interest in U.S. barrels worldwide. The spread between light sweet crude at Midland and the Gulf coast widened to as much as 50 cents last week from an average of 30 cents earlier in the month.

“People are paying up for barrels at the coast,” one U.S.-based broker said.

Light Louisiana Sweet rose to a $3.50 premium to U.S. crude futures on July 22, highest in five months.

U.S. gasoline inventories posted a larger-than-expected build on weakened demand during the peak summer driving season, according to the Energy Information Administration.

“Gasoline accounts for half of total U.S. oil consumption and serves as a barometer for the health of the world’s biggest economy, hence the impact on the WTI crude benchmark,” PVM’s Brennock said.

Brent, meanwhile, is stronger due to tight supply resulting from the loss of Russian barrels after the country’s invasion of Ukraine and persistent underproduction from OPEC+, which includes OPEC and allies such as Russia. Buyers are concerned that OPEC is close to running out of spare capacity, limiting its ability to raise output further.

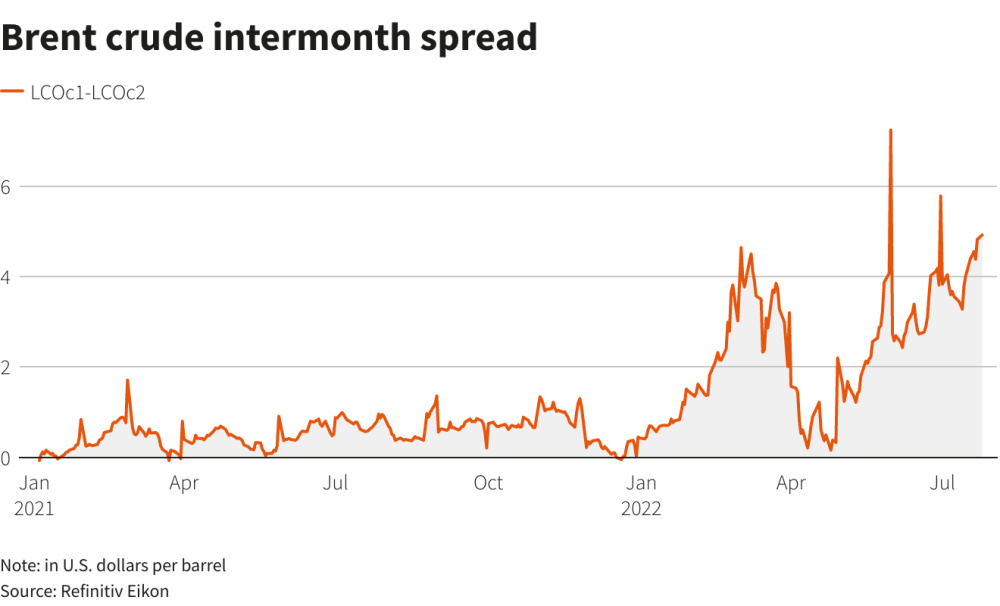

The supply tightness pushed Brent’s intermonth spreads to $4.82/bbl on July 22, the widest backwardation on record when excluding expiry-related peaks in the last two months. In a backwardated market, front-month prices are higher than those in future months, signaling tight supplies.

This compares with backwardation in WTI intermonth spreads of $2.27/bbl on July 22.

Recommended Reading

Equitrans Midstream Announces Quarterly Dividends

2024-04-23 - Equitrans' dividends will be paid on May 15 to all applicable ETRN shareholders of record at the close of business on May 7.

PrairieSky Adds $6.4MM in Mannville Royalty Interests, Reduces Debt

2024-04-23 - PrairieSky Royalty said the acquisition was funded with excess earnings from the CA$83 million (US$60.75 million) generated from operations.

Baker Hughes Awarded Saudi Pipeline Technology Contract

2024-04-23 - Baker Hughes will supply centrifugal compressors for Saudi Arabia’s new pipeline system, which aims to increase gas distribution across the kingdom and reduce carbon emissions

EQT Declares Quarterly Dividend

2024-04-18 - EQT Corp.’s dividend is payable June 1 to shareholders of record by May 8.

Matador Resources Announces Quarterly Cash Dividend

2024-04-18 - Matador Resources’ dividend is payable on June 7 to shareholders of record by May 17.