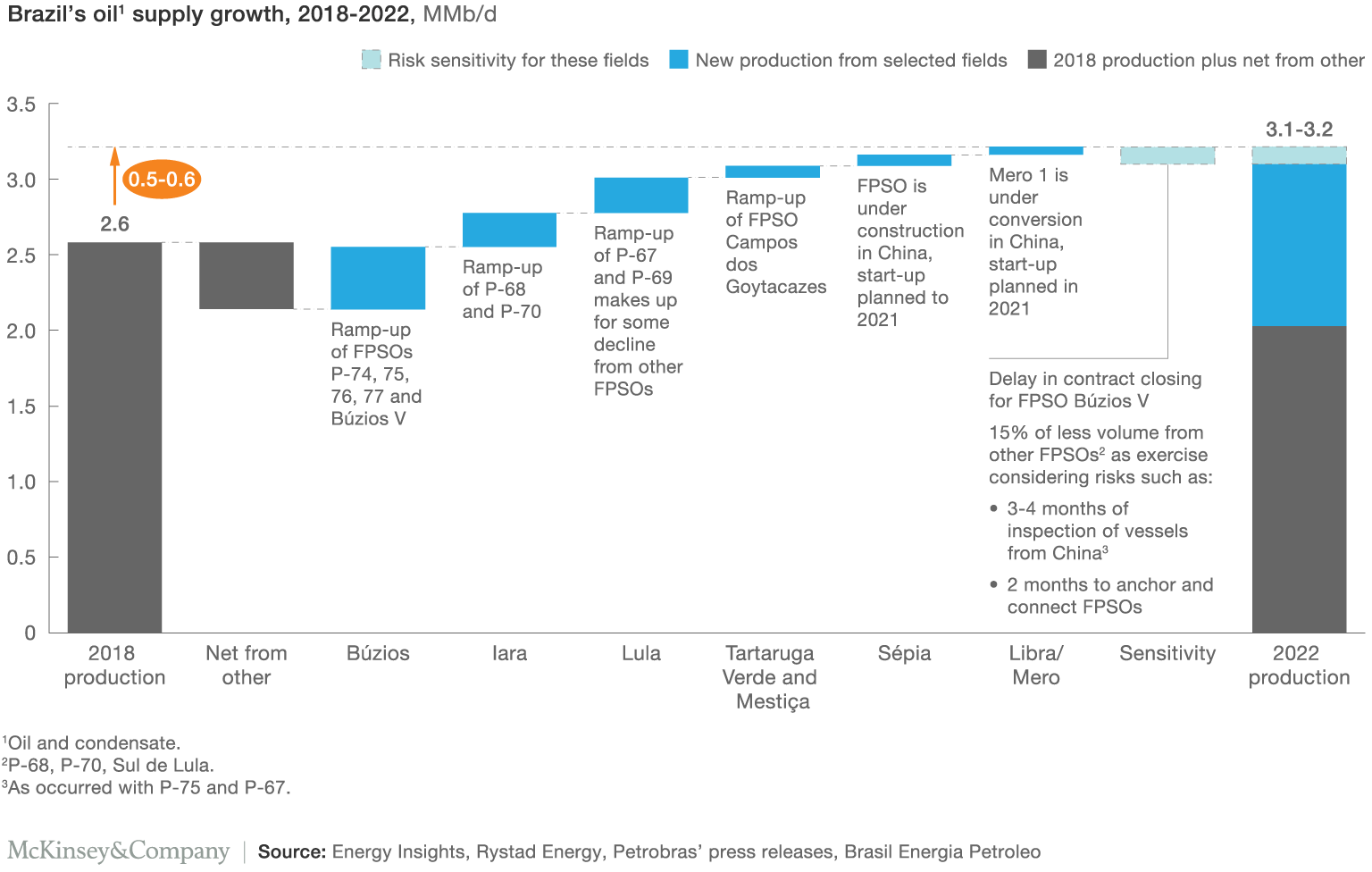

Brazil can look forward to some positive news when it comes to oil production for the next few years. After closing 2018 at nearly 2.6 MMbbl/d, production is slated to continue ramping up and post a 0.64-MMbbl/d increase (or about 25% growth) by 2022—with some downside risk, should contract closures be delayed.

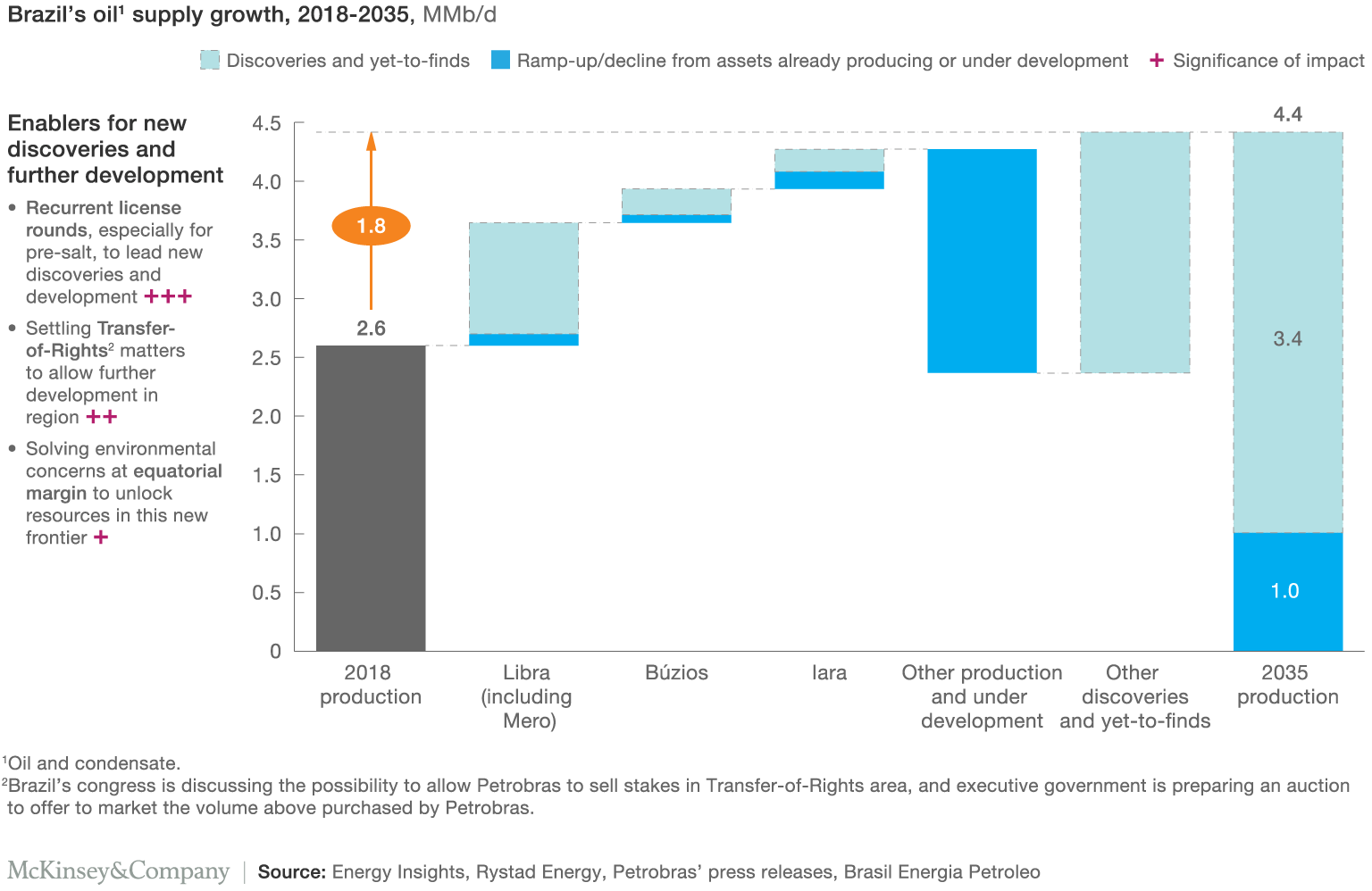

In the long term, Brazil also can potentially add 1.8 MMbbl/d in production by 2035, which is about a 70% increase compared to current levels. However, for this long-term growth to be realized, Brazil will need to create the right investment climate to allow assets to come online through either future discoveries or new development plans.

Brazil’s oil supply poised to grow to 2022

Brazil’s full-year 2018 oil production declined by 1% to 2.59 MMbbl/d, despite the continuous growth in presalt. Looking ahead to 2019 and beyond, McKinsey Energy Insights expects to see production increase steadily, thanks to activity ramping up from both existing FPSOs and new presalt FPSOs slated to be installed soon. All included, oil production should grow by 24% to 3.2 MMbbl/d by 2022. Interestingly, most of the growth will be again led only by a handful of key fields: Búzios, Lula, Iara, Sépia, Tartaruga Verde and Mestiça as well as the first barrels from the giant Mero. These fields, when combined, will add more than 1 MMbbl/d to the supply stack. The rest of Brazilian production together is net negative.

There is always the risk of delays in the implementation of Petrobras’ ambitious plans. While the company has reined in past delays associated with the rollout of its FPSOs, a high-level risk sensitivity analysis suggests that up to 0.11 MMbbl/d of production (about 3%) may not be achieved by 2022. Búzios has traditionally been hassled by timeline misses. A delay in contract closing for FPSO Búzios V puts about 0.08 MMbbl/d of volume at risk. McKinsey Energy Insights further anticipates that the industry could see up to 15% less volume from other FPSOs, driven by potential delays during the three to four months needed to inspect vessels from China and two months to anchor and connect FPSOs.

Policy and licensing developments

Long-term growth for Brazil hinges on policy and licensing developments. While the short-term perspective looks promising, the long-term outlook for Brazil’s production is more complex. As it stands, assets currently producing or under development are unlikely to be enough to keep oil production growing for the next few decades.

If the country is to sustain long-term growth, it will need to look beyond development and recovery enhancement of currently producing assets. This is evident in Petrobras’ new Strategic Plan 2040: Expex is now expected to account for 16% of total E&P investment in the next five years, growing to $11 billion from $7 billion in the last investment cycle (2018-2022). Holding recurring licensing rounds, especially for presalt blocks, will play a vital role in driving discoveries and, more importantly, new development.

Settling the Transfer of Rights contractual issues will allow further development in the region. Auctioning the rights to develop presalt resources, in excess of the 5 Bbbl granted to Petrobras in the 2010 Transfer of Rights contract, can only occur after the contract’s revision, which is now ongoing. In parallel, the Brazilian

congress is discussing permitting Petrobras to sell nonoperating (up to 70%) stakes in the fields covered by the Transfer of Rights contract to other companies. The move would allow Petrobras to spread development cost in the area to external partners and help the company diversify its portfolio.

Last but not least, there is also upside production potential related to unlocking resources in the equatorial margin, yet the associated environmental concerns need to be resolved first.

Should Brazil successfully address these issues, the country could achieve an output of 4.4 MMbbl/d by 2035—a 1.8 MMbbl/d, or 70%, increase from the 2018 baseline. The projection assumes that an incremental 3.4 MMbbl/d of production would come from discoveries. If the country continues to only rely on assets that are already producing or under development instead, production would decline to 1 MMbbl/d by 2035.

The outlook for Brazil’s oil production to 2035 will depend heavily on whether the country can open up for additional exploration and development in new fields and blocks. Companies other than Petrobras are poised to have a big role in making these investments happen.

Recommended Reading

BP Pursues ‘25-by-‘25’ Target to Amp Up LNG Production

2024-02-15 - BP wants to boost its LNG portfolio to 25 mtpa by 2025 under a plan dubbed “25-by-25,” upping its portfolio by 9% compared to 2023, CEO Murray Auchincloss said during the company’s webcast with analysts.

BP Restructures, Reduces Executive Team to 10

2024-04-18 - BP said the organizational changes will reduce duplication and reporting line complexity.

Kimmeridge Fast Forwards on SilverBow with Takeover Bid

2024-03-13 - Investment firm Kimmeridge Energy Management, which first asked for additional SilverBow Resources board seats, has followed up with a buyout offer. A deal would make a nearly 1 Bcfe/d Eagle Ford pureplay.

M4E Lithium Closes Funding for Brazilian Lithium Exploration

2024-03-15 - M4E’s financing package includes an equity investment, a royalty purchase and an option for a strategic offtake agreement.

Laredo Oil Subsidiary, Erehwon Enter Into Drilling Agreement with Texakoma

2024-03-14 - The agreement with Lustre Oil and Erehwon Oil & Gas would allow Texakoma to participate in the development of 7,375 net acres of mineral rights in Valley County, Montana.