John Kemp, Reuters

OPEC’s output accord in Algiers last month was initially greeted with enthusiasm by oil market bulls but much of that euphoria is now dissipating as traders question whether it will make an actual difference.

The agreement, coming after many observers had written off the possibility of a deal, initially pushed crude prices sharply higher.

Flat prices and timespreads firmed as traders concluded the accord would accelerate the rebalancing of supply and demand.

For many oil market veterans, the agreement showed OPEC was back in business after being dormant for several years.

“Saudi Arabia has decided it wants higher prices and is working with the rest of OPEC, and quite possibly Russia, to achieve them by curbing production,” hedge fund manager Andy Hall wrote a few days after the deal.

“It’s a brave person who bets against this combination of factors,” Hall said in a letter to investors in his Astenbeck hedge fund, which is fairly typical of the thinking among bullish traders.

But over the past couple of weeks enthusiasm has given way to doubts about whether the agreement will make any real difference to the supply-demand balance next year.

Familiar concerns have emerged about OPEC’s willingness and ability to cut production in order to push prices higher.

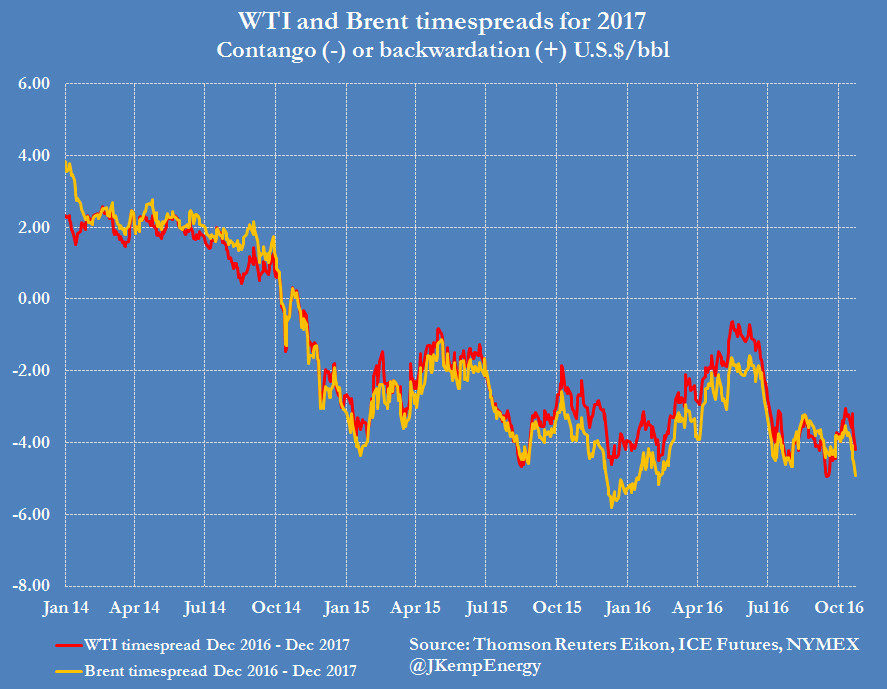

Brent futures prices have been gently sliding since peaking on Oct. 10 while timespreads for 2017 have been softening.

The spread between December 2016 and December 2017 Brent contracts closed at $4.91 per barrel contango on Oct. 24, the weakest since February, suggesting rebalancing is still some way off.

Production Limits

OPEC’s agreement was vague about how much it would actually restrict production, for how long, and how the restrictions would be shared out among the organization's members.

Difficult decisions about production allocations were left to OPEC's next ministerial conference in November.

The Algiers agreement was deliberately silent about allocations to provide flexibility for some countries to raise their production even while others agreed to freeze or cut.

Saudi officials indicated there could be some limited flexibility for Iran, Libya and Nigeria, which claim their output has been temporarily disrupted, to pump more in the months ahead.

But Iraq has since claimed its output has been undercounted in the past and indicated that they want higher allocations.

Iraq and Iran have rejected any attempt to restrict their production and attempts to recover historical market share.

And Russia remains coy about whether it would be prepared to restrain its own production to support an OPEC output freeze.

If there is to be a deal, Saudi Arabia and its close allies Kuwait and possibly the UAE will have to do almost all the freezing and cutting, while other OPEC and non-OPEC countries will be free to produce as much as they are able.

Saudi Burden

The result is familiar to anyone who has followed OPEC history.

Saudi Arabia and its allies shouldered most of the production cuts in 1983-1986, 1999 and 2009, with only symbolic cuts by other OPEC and non-OPEC countries.

The 1999 agreement between OPEC and certain non-OPEC countries is often cited as a prime example of cooperative cuts to push prices higher. The real story is different.

“The only country that reduced production voluntarily ... is Saudi Arabia, with marginal help from Kuwait and the UAE, while all other oil producing countries were forced to reduce their production because of technical, political, or natural factors,” Alhajji and Huettner wrote shortly afterwards.

Commentators have often mistakenly assigned the market power of Saudi Arabia and its allies to OPEC as a whole.

“Recent developments are best explained by the continuing dominant producer role of Saudi Arabia, capacity limitations in several OPEC and non-OPEC countries, and not by OPEC maturing into a successful cartel,” according to Alhajji and Huettner.

Much of the commentary about OPEC and output agreements tends to obsess about personalities and the negotiating process.

In practice, Saudi Arabia and other members of the organization face structural constraints which dictate their strategy and choices that have not changed much over the last four decades.

The difficult strategic choice confronting Saudi Arabia’s current rulers (how much production to sacrifice in exchange for higher prices while risking growth in rival supplies) is the same as it has been since the 1980s.

Swinging Again

Between 2014 and June 2016, Saudi policymakers insisted the kingdom would not reprise its swing producer role and reduce its own output unless other OPEC and non-OPEC producers joined the cutbacks.

But faced with continued low prices and a deteriorating budget situation, the kingdom has found itself in a familiar predicament, contemplating limits on its own output while other countries pump as much as they can.

Saudi Arabia, alone among the oil-producing countries, has always had an effective choice between maximizing output and seeking higher prices.

After pursuing an output-based strategy between 2014 and June 2016, the kingdom now appears to shifting towards a price-based strategy. But it will likely have to pursue that strategy on its own.

The kingdom’s readiness to pursue significant output restraint, as opposed to simply reversing its normal summer production surge, remains untested.

Iraq, Iran and Russia all aim to increase their output in 2017, and higher oil prices are triggering an increase in shale drilling in the US.

The kingdom seems to be gambling that if it restrains its own production, other countries will struggle to increase their own output for technical, commercial and political reasons.

Saudi Arabia will have to practice production restraint alone, with limited support from Kuwait and the UAE, and risk giving up some market share to achieve an improvement in prices.

In the circumstances, many traders are skeptical about whether the kingdom can engineer a large and sustained price rise.

With shale firms ramping up their drilling programs, there is plenty of skepticism about how far prices can rise before shale output starts increasing again significantly.

Recommended Reading

Kinder Morgan Nominates Deloitte’s Amy Chronis to Board

2024-04-03 - Amy Chronis, currently a senior partner with Deloitte, will stand for election along with Kinder Morgan’s current directors at the company’s annual meeting on May 8.

Canadian Natural Resources Boosting Production in Oil Sands

2024-03-04 - Canadian Natural Resources will increase its quarterly dividend following record production volumes in the quarter.

OGInterview: Building EIV Capital’s Midstream Investment Strategy

2024-05-01 - Midstream-focused EIV Capital has added non-operated assets and transition projects to its portfolio as a sign of the times.

Valaris’ 1Q Sets Positive Tone for Offshore

2024-05-06 - Coming out of first-quarter 2024, drilling contractor Valaris expects a sustained upcycle for the offshore drilling industry supported by demand growth, OPEC+ production cuts and supportive commodity prices.

Buffett: ‘No Interest’ in Occidental Takeover, Praises 'Hallelujah!' Shale

2024-02-27 - Berkshire Hathaway’s Warren Buffett added that the U.S. electric power situation is “ominous.”