PowerAdvocate

In the last 11 months, the world changed.

First came the sharp decline in oil prices and then followed other commodities, from steel and copper to chemicals and plastics.

While there’s been plenty of talk about the negative impact of the oil price decline on margin and growth, there’s also a much-less-talked-about opportunity to turn those commodity declines into significant cost reduction.

In this post, we’ll show you how a “typical” midstream firm with $1.5 billion in spend can capture $25 million in savings from just one of those commodity declines.

Market-driven savings often follow sharp declines in commodities. Steel, which dropped by 30+% over the last 11 months, has been one of the most drastic commodity downturns, offering a smoke signal that significant savings opportunities should follow.

But knowing that steel prices have dropped isn’t enough. To identify real savings opportunities, you also need to understand how that drop affects the costs of the things you buy. You can do that by using cost models: tools that pinpoint the exact cost components of an item or group of items.

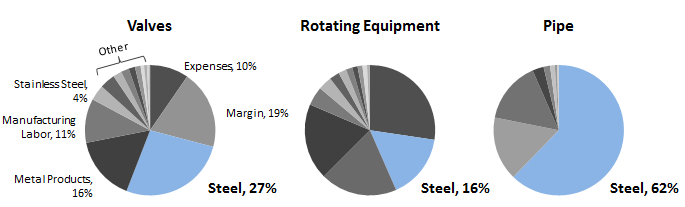

Below, we’ve used cost models to identify 3 major midstream cost categories that are significantly affected by steel. In each case, from valves to rotating equipment to pipe, steel comprises a significant component of overall costs, indicating a potential savings opportunity from the recent price declines.

The next step is to quantify how much the drop in steel prices (in combination with other cost drivers) impacts the cost of each item. This can be done by running a ‘should-cost’ analysis, which ties each of the input costs (metals, labor, plastics, etc.) to indices that move over time so that you can see what an actual item should cost relative to the market.

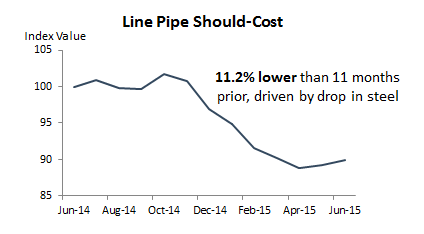

For instance, a 30+% decline in steel (along with movements in other cost drivers) should result in line pipe having dropped 11.2% over the last 11 months.

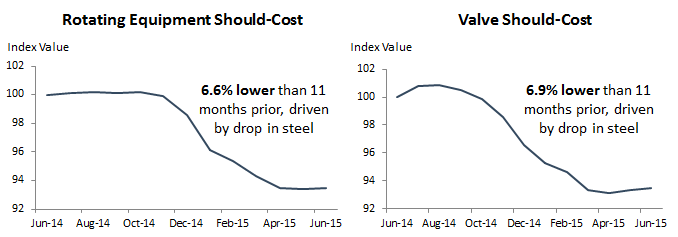

The same is true for rotating equipment and valves, each of which should have declined by 6+% over the last 11 months.

Has your pricing changed accordingly?

Because suppliers prefer to keep savings for themselves, it’s unlikely that you’ll see price changes naturally occur in the marketplace. To be proactive about capturing savings, you’ll need to drive supplier negotiations with market data in the form of market indices, cost models and should-cost analyses.

On average, the above three categories comprise 19.7% of midstream companies’ spend profiles, meaning that negotiations on just those categories can yield $25 million in savings for a company with $1.5 billion in spend.

The opportunity extends far beyond the three steel-heavy categories we’ve identified here. Declines in fuel, plastics, chemicals and metals have all opened up significant savings, not to mention supply & demand factors, which are currently favorable for many midstream cost categories.

Interested in other market-driven savings opportunities beyond steel? Click here to learn about fuel-based savings.

PowerAdvocate helps midstream companies tackle their toughest strategic challenges, from cost reduction to project estimation, with a combination of data, technology, and expert services. To contact us for more information on any of the topics in today’s post, email us at: costinsights@poweradvocate.com.

Recommended Reading

Keeping it Simple: Antero Stays on Profitable Course in 1Q

2024-04-26 - Bucking trend, Antero Resources posted a slight increase in natural gas production as other companies curtailed production.

Oil and Gas Chain Reaction: E&P M&A Begets OFS Consolidation

2024-04-26 - Record-breaking E&P consolidation is rippling into oilfield services, with much more M&A on the way.

Exxon Mobil, Chevron See Profits Fall in 1Q Earnings

2024-04-26 - Chevron and Exxon Mobil are feeling the pinch of weak energy prices, particularly natural gas, and fuels margins that have cooled in the last year.

Marathon Oil Declares 1Q Dividend

2024-04-26 - Marathon Oil’s first quarter 2024 dividend is payable on June 10.

Talos Energy Expands Leadership Team After $1.29B QuarterNorth Deal

2024-04-25 - Talos Energy President and CEO Tim Duncan said the company has expanded its leadership team as the company integrates its QuarterNorth Energy acquisition.