This blog was originally published on Evaluate Energy's website by Mark Young: http://blog.evaluateenergy.com/hedging-helps-canadian-oil-gas-companies-in-low-price-climate

Canadian oil and gas companies that hedged their oil production before the global oil price crash will be very relieved they did so. This CanOils study of 45 TSX-listed companies’ Q4 2014 results (see note 1) shows that many Canadian companies made large realized hedging gains as the oil price fell to around $50 by year-end 2014. This study agrees with a recent EIA article, written using Evaluate Energy data, showing the impact of hedging on U.S. companies during the same period.

Whilst hedging may have seemed over-cautious at the start of the year, with oil prices not having wavered from the $90-$100 mark for quite some time, hedging eventually proved to be a prudent strategy given the collapse of commodity prices by almost 50% towards the end of the year.

Hedging contracts (also known as derivative contracts) are a common risk management strategy for oil and gas producers. A producing company will agree with a buyer to sell future production at a certain price, thus potentially limiting revenues if prices climb, but simultaneously shielding the producer from excessive losses should commodity prices suddenly fall.

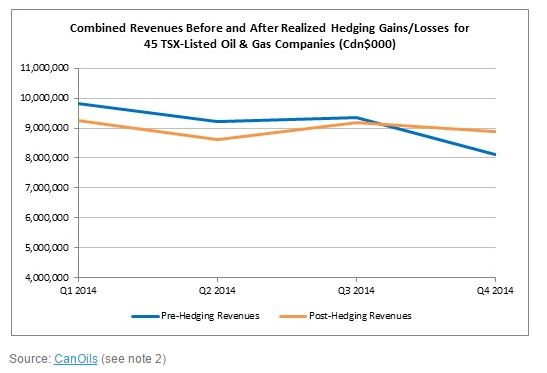

The chart below shows that the group of 45 TSX-listed companies, as a whole, experienced both sides of the hedging dynamic in 2014.

Whilst high prices were not realized by the 45 companies to their full potential in Q1 and Q2, hedging has clearly helped significantly lessen effects of the commodity price downturn in Canada towards the end of 2014. The graph is almost identical to that reported by the EIA for U.S. companies using Evaluate Energy data. The lines for pre- and post-hedging revenues are almost parallel in Q1 and Q2, begin to converge in Q3 and then switch over dramatically in Q4 as benchmark oil prices began to tumble.

Of the companies involved in the report (see note 1), the following companies reported the biggest realized hedging gains per boe on their production in Q4 2014.

The biggest gains on hedging in Q4 were clearly made by oil producers rather than gas producers; with the exception of Enerplus, all of these companies’ production portfolios are made up of over 75% oil. Exall (97% oil) and Arsenal (78% oil) made extremely significant gains due to their hedging contracts, rescuing around $22 and $15 per boe respectively.

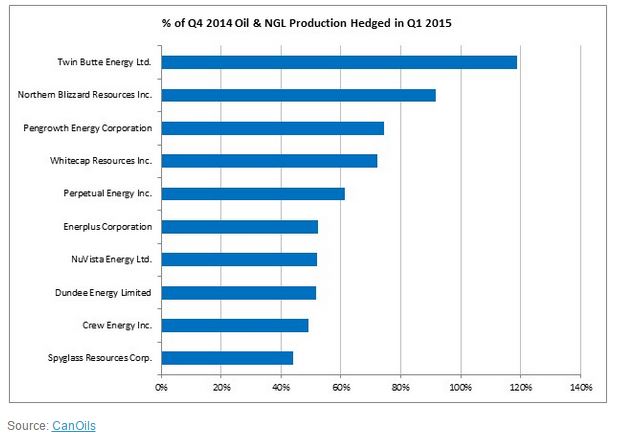

There is little to suggest the oil price will rebound any time soon, meaning that hedging positions will also play an important role in determining how successful a quarter Q1 2015 was for the 45 companies. The chart below shows the best hedged companies out of the 45 included in this study. The companies were identified as having the highest percentage of Q4 2014 oil and NGL production covered by hedging contracts that are valid in Q1 2015.

The CanOils database provides clients with efficient data solutions to oil and gas company analysis, with 10+ years financial and operating data for over 300 Canadian oil and gas companies - including all oil and gas hedging positions on a quarterly basis - as well as M&A deals, Financings, Company Forecasts, Guidance and an industry leading oil sands product.

Notes:

1) The 45 selected companies from the CanOils database fit the following criteria:

a) TSX-Listed

b) Has Canadian oil and gas production

c) Had oil hedges in place at the end of Q3 2014 that would be valid in Q4

d) Reported realized hedging gains on their income statements from Q1-Q4 2014

e) Non-oil sands producer (i.e. less than 10% of production portfolio made up of oil sands)

For a full list of companies included in the report, click here

2) All data in this chart is taken or calculated using the respective companies’ income statements. Post-hedging revenues refers to all E&P revenues plus realized commodity hedging gains or losses.

Recommended Reading

TGS Commences Multiclient 3D Seismic Project Offshore Malaysia

2024-04-03 - TGS said the Ramform Sovereign survey vessel was dispatched to the Penyu Basin in March.

TGS, SLB to Conduct Engagement Phase 5 in GoM

2024-02-05 - TGS and SLB’s seventh program within the joint venture involves the acquisition of 157 Outer Continental Shelf blocks.

AI in Oil: Revolution’s Coming, but Tech Adoption Remains Tentative

2024-04-05 - CERAWeek experts say AI will disrupt oil and gas jobs while new opportunities will emerge as the industry braces for an AI-driven workflow transformation.

Geothermal ‘Could Save the World,’ but Faces Familiar Subsurface Risks

2024-03-20 - CERAWeek panelists discussed hurdles to widespread use of Earth’s heat to generate power — problems familiar to oil and gas operators.

TotalEnergies Rolling Out Copilot for Microsoft 365

2024-02-27 - TotalEnergies’ rollout is part of the company’s digital transformation and is intended to help employees solve problems more efficiently.