By Phoebe McMellon, Elsevier Geofacets

To offset diminishing oil output from Pemex, Mexico’s state-owned oil giant, the Mexican government started implementing landmark energy reforms in 2014, ending 75 years of state monopoly by opening up one of the world’s largest oil and gas reserves to foreign investment.

Through a series of private auctions, the government ultimately plans to open up 17% of currently producing oil fields to foreign exploitation and allow foreign companies to bid for the development rights to 79% of Mexico’s reserve fields. While the state will retain ownership of the resources, successful foreign companies will be awarded with either a license, a production-sharing deal or a profit-sharing deal.

According to the original schedule for Round One, 169 blocks—of which 60 are production blocks—are to be auctioned by October, although there could be some slippage in the timetable in reaction to the cutbacks in exploration that oil majors have announced. However, preliminary bidding rules for 14 shallow water exploration blocks were issued in December, and the auction scheduled for July will most likely go ahead (it is expected to generate about $14 billion in investment).

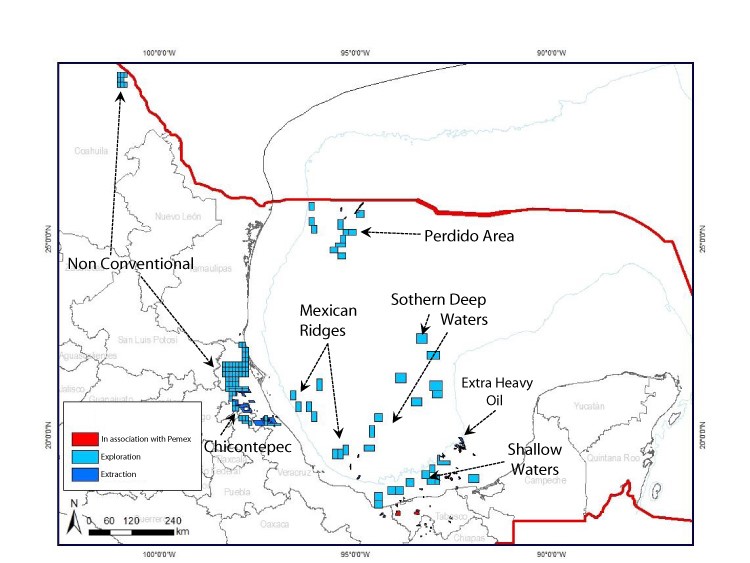

Round One, timetabled for 2015, offers a succession of three distinct opportunities for bidders in three regions. The first commences with the 14 exploration oil and gas fields in shallow waters located near the supergiant Cantarell and Ku-Maloob Zaap oil fields. Later in the year comes the more costly-to-develop shale rock Chicontepec formations and tight oil blocks. And, at year-end, blocks in the mostly unexplored deepwaters of the Gulf of Mexico (GoM) will be offered. Taken together, these 169 blocks cover 28,500 sq km (11,002 sq miles).

Round One alone offers bidders the opportunity to make a claim to an estimated 3.8 billion barrels of oil reserves and 14.6 billion barrels of prospective reserves at an estimated annual investment of $8.5 billion over four years. Each of these regions represents a significant and diverse investment opportunity that includes producing areas, new and largely unexplored areas in both shallow and deepwater areas, covering both conventional resources and unconventional fields with high prospective potential.

Map of Mexico's Round 1

The first 14 shallow water blocks remain on schedule since they have the lowest projected development costs at around $20 a barrel and are, therefore, profitable even at current oil prices. In mid-January, it was reported that the energy ministry, in response to low oil prices and cutbacks in exploration budgets, may limit the shale oil and gas and tight oil offer to only the most attractive unconventional resources since extraction is expensive. A decision on what areas to offer and the final timetable is expected in April.

In contrast, the deepwater blocks have both huge potential and high investment costs, if the American experience on its side of GoM waters is any guide. However, since it will take at least eight years to develop a field from scratch—and oil majors have long time-horizons—it is likely that bids will be invited as planned at year-end.

Lack of information is the universal challenge to all exploration activities.

The

The challenge of these offers is that companies need dependable geological information to identify the best license blocks on which to bid and even more geological data to target blocks that will have the greatest potential for an economically viable petroleum system with the lowest exploration and production risk. Unfortunately, much of that information is not readily available, accessible or even digestible in its current form. Nevertheless, the attraction of a prospective 115 billion barrels of oil equivalent may, despite the lack of information, prove this round to be potentially one of the most expensive bid rounds in history. Companies will be focused on the long-term strategy of their investments when bidding and are prepared to heavily quantify that commitment. For such a resource, bidders will be in it for the long game.

Another factor influencing this gold rush is the history of success in Mexico’s shallow waters, most notably the presence of the supergiant Cantarell Field, which was for many years the second largest oil field in the world due to the area’s favorable petro-geology. In Mexico, deltas with beach sands have proven to be very strong locations for finding oil. The highest success rates—exceeding 25%—have historically been in the shallows where such sands are located. This knowledge further fuels the frenzy and justifies higher and higher bids.

In part two, we will examine the many challenges that face any company wishing to participate in Round One; particularly the lack of definitive information that means decisions are being guided by guesswork.

Phoebe McMellon is director of product management for Elsevier Geofacets.

Recommended Reading

Moda Midstream II Receives Financial Commitment for Next Round of Development

2024-03-20 - Kingwood, Texas-based Moda Midstream II announced on March 20 that it received an equity commitment from EnCap Flatrock Midstream.

Sunoco’s $7B Acquisition of NuStar Evades Further FTC Scrutiny

2024-04-09 - The waiting period under the Hart-Scott-Rodino Antitrust Improvements Act for Sunoco’s pending acquisition of NuStar Energy has expired, bringing the deal one step closer to completion.

Enbridge Advances Expansion of Permian’s Gray Oak Pipeline

2024-02-13 - In its fourth-quarter earnings call, Enbridge also said the Mainline pipeline system tolling agreement is awaiting regulatory approval from a Canadian regulatory agency.

OGInterview: Building EIV Capital’s Midstream Investment Strategy

2024-05-01 - Midstream-focused EIV Capital has added non-operated assets and transition projects to its portfolio as a sign of the times.

Oil and Gas Chain Reaction: E&P M&A Begets OFS Consolidation

2024-04-26 - Record-breaking E&P consolidation is rippling into oilfield services, with much more M&A on the way.