OPEC Ministers are meeting in Vienna to discuss extending or even deepening the current OPEC+ supply agreement, Stratas Advisors reported on Dec. 4. After swiftly convincing markets that an extension until June 2020 was virtually guaranteed, ministers have entered today’s meeting with markets now expecting cuts to be both extended and deepened from 1.2 million barrels per day (MMbbl/d) to as much as 1.6 MMbbl/d. In such a scenario Saudi Arabia would most likely need to bear the brunt of the cut, taking production well below 10 MMbbl/d for much of 2020.

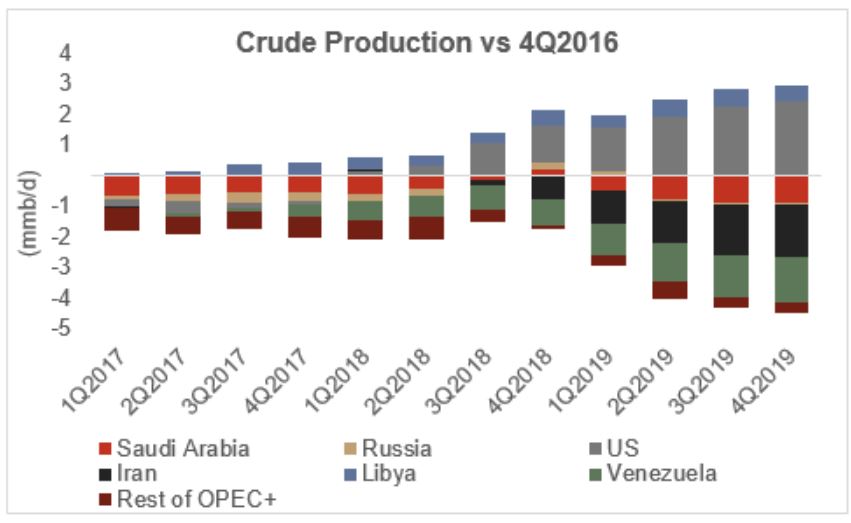

Stratas Advisors continues to believe that a flat extension until at least June of 2020 (if not December) is the most likely outcome, with continued emphasis on increasing compliance. Members are earning more money selling less crude than in the fourth quarter of 2016 when the agreement was struck. However, while OPEC+ members have benefitted from the supply agreement, so have U.S. producers with U.S. crude and condensate production in the third quarter of 2019 approximately 3.1 MMbbl/d above fourth quarter 2016 levels.

Stratas’ Global Hydrocarbon Supply team expects non-OPEC production growth to average 1.4 MMbbl/d in 2020 with increases seen in Brazil, Canada, Norway and potentially Mexico. The bulk of production growth in 2020 though will continue to come from the United States, albeit at a lower rate than in previous years.

Even if a deeper cut is agreed to and complied with, it might not be enough to raise prices substantially. A cut of 1.5 MMbbl/d would barely cover the expected growth in non-OPEC production, leaving markets in a similar situation to this year. However, negative expectations about global demand growth continue to be the dominant variable impacting crude oil prices. As discussed in Stratas’ last global economic outlook several measurements of market uncertainty are showing unprecedented levels, highlighting how pervasive uncertainty about global trade is among governments, traders, and consumers. While still not expecting a global contraction, analysts expect widespread pain and a slowdown in growth in several major countries. Risks remain skewed to the downside and several significant trade disputes remain unresolved heading into 2020.

Recommended Reading

Comstock Continues Wildcatting, Drops Two Legacy Haynesville Rigs

2024-02-15 - The operator is dropping two of five rigs in its legacy East Texas and northwestern Louisiana play and continuing two north of Houston.

To Dawson: EOG, SM Energy, More Aim to Push Midland Heat Map North

2024-02-22 - SM Energy joined Birch Operations, EOG Resources and Callon Petroleum in applying the newest D&C intel to areas north of Midland and Martin counties.

CEO: Continental Adds Midland Basin Acreage, Explores Woodford, Barnett

2024-04-11 - Continental Resources is adding leases in Midland and Ector counties, Texas, as the private E&P hunts for drilling locations to explore. Continental is also testing deeper Barnett and Woodford intervals across its Permian footprint, CEO Doug Lawler said in an exclusive interview.

Chevron Hunts Upside for Oil Recovery, D&C Savings with Permian Pilots

2024-02-06 - New techniques and technologies being piloted by Chevron in the Permian Basin are improving drilling and completed cycle times. Executives at the California-based major hope to eventually improve overall resource recovery from its shale portfolio.

Tech Trends: Halliburton’s Carbon Capturing Cement Solution

2024-02-20 - Halliburton’s new CorrosaLock cement solution provides chemical resistance to CO2 and minimizes the impact of cyclic loading on the cement barrier.