In the week since our last edition of What’s Affecting Oil Prices, Brent averaged $58.06/bbl; however, prices slipped throughout the week and ended $1.48/bbl lower than they started. Fundamental and geopolitical variables remain generally supportive, but with technicals only slightly off of overbought levels a price correction is still possible.

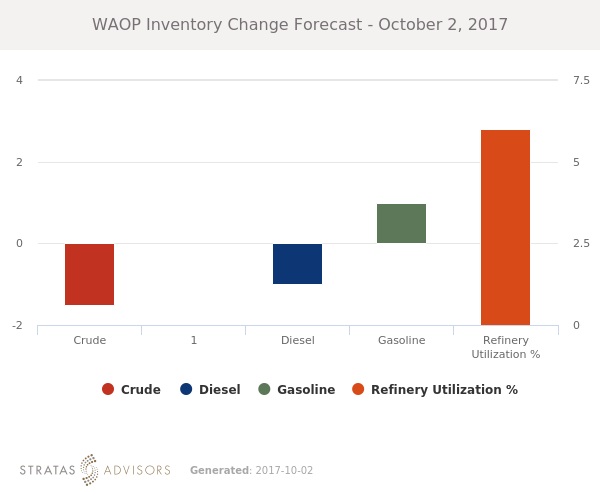

For the upcoming week, Stratas Advisors expects prices to average $56/bbl and crude stocks to fall 1.5 MMbbl. Stratas Advisors also expects the WTI-Brent differential to average about $5.75/bbl as Brent prices moderate slightly.

The supporting rationale for the forecast is provided below.

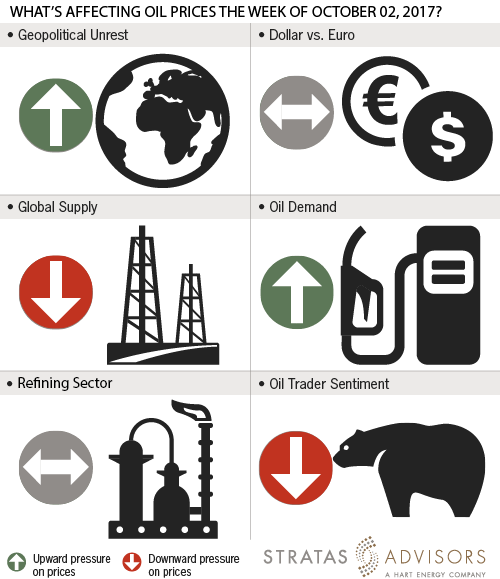

Geopolitical: Positive

While there were no major developments, geopolitics will continue to drive volatility with the few active hotspots that bear watching more likely to hamper oil supply, helping prices. The referendum in Kurdistan unsurprisingly led to a “yes” vote. Stratas Advisors continues to expect this will have no immediate impact on crude although the situation does bear watching due to the crude production and transportation infrastructure in the region. Stratas Advisors expects there could be further noise around the vote as Iran and Turkey impose various restrictions on the Kurdistan region, but see no immediate complications.

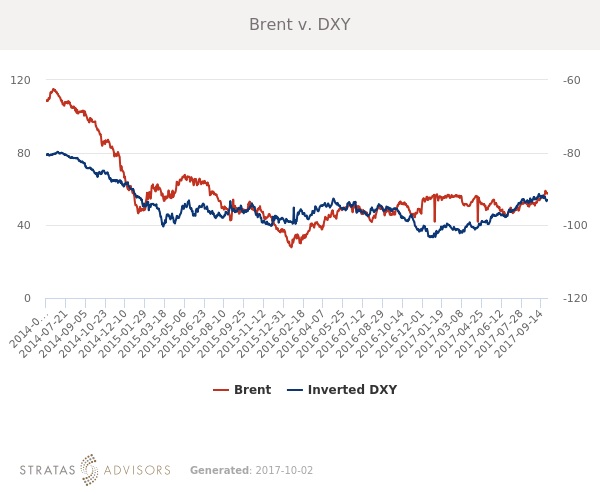

Dollar: Neutral

The dollar’s relationship with crude remains strong. The dollar will continue its slow gains, removing a leg of support from crude prices, but not yet strong enough to counter crude’s bull-run. President Trump has reportedly begun interviewing candidates for Federal Reserve Chair, with former Federal Reserve governor Kevin Warsh an apparent front-runner. Warsh is considered more hawkish than current Chair Janet Yellen and this could mean interest rates are normalized more quickly.

Trader Sentiment: Negative

Prices will lose some support from trader sentiment this week, with headlines showing an increased concern for the global supply picture. While the global supply picture is little changed from last week, market participants appear more cognizant of the ongoing level of oversupply and the time still needed to achieve fundamental rebalancing. NYMEX WTI and ICE Brent managed money net longs both increased while ICE WTI net longs fell in the latest data reported.

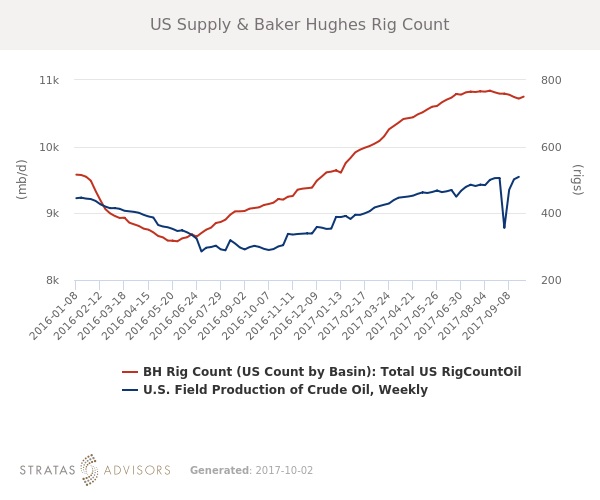

Supply: Negative

Last week the number of operating oil rigs in the U.S. increased by six, according to the weekly report from Baker Hughes (NYSE: BHGE). This marks the first increase in six weeks. U.S. oil rigs now stand at 750 compared to 325 at the same time in 2016. This increase is not necessarily part of a trend, as these blips have occurred before and it could even just be a result of ongoing hurricane recovery. Estimated U.S. production increased last week; the gains were split nearly evenly between reported Alaska volumes and onshore US estimates. The EIA’s Petroleum Supply Monthly report also indicated 141 MMbbl/d of production growth between June and July. Despite recent positive sentiment, these physical metrics will likely bring some market participants back to reality and emphasize that while rebalancing is proceeding, it is still a slow process.

Demand: Positive

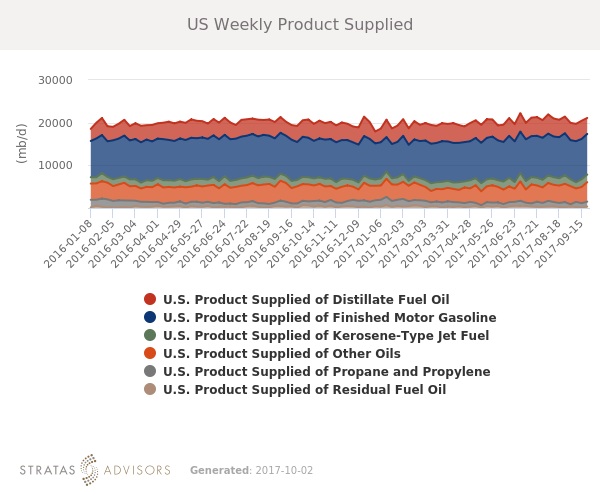

Demand remains healthy, with U.S. gasoline and distillate demand both well above seasonal norms. The latest monthly data from the EIA shows that gasoline, distillate and jet fuel demand remain healthy. All are either in line with or slightly above 2016 levels, despite some month-on-month declines. Weekly demand data will likely start to show seasonal declines, but still generally trend above 2016 levels.

Refining: Neutral

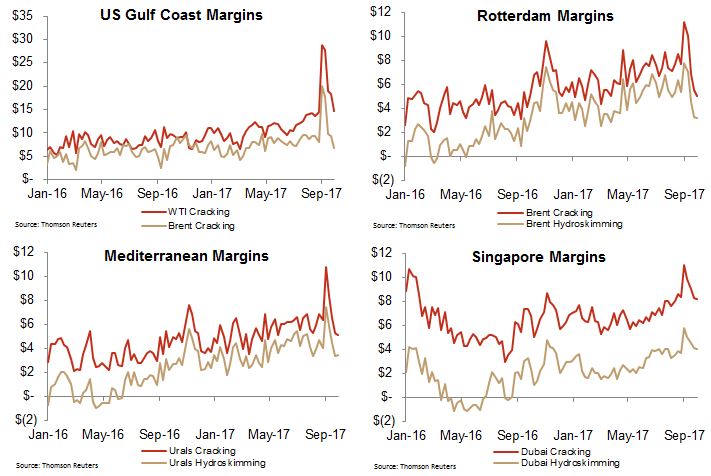

Margins fell in the Gulf Coast, but held fairly steady in the rest of the world. WTI cracking on the Gulf Coast fell $3.53/bbl. In Rotterdam, Brent cracking fell $0.51/bbl vs. a fall of $1.37/bbl the week before. Margins should hold fairly steady, with some room to downside as summer demand winds down. However, they remain healthy enough to continue incentivizing crude runs.

How We Did

Recommended Reading

US Drillers Cut Oil, Gas Rigs for Fourth Week in a Row-Baker Hughes

2024-04-12 - The oil and gas rig count, an early indicator of future output, fell by three to 617 in the week to April 12, the lowest since November.

US Raises Crude Production Growth Forecast for 2024

2024-03-12 - U.S. crude oil production will rise by 260,000 bbl/d to 13.19 MMbbl/d this year, the EIA said in its Short-Term Energy Outlook.

Sangomar FPSO Arrives Offshore Senegal

2024-02-13 - Woodside’s Sangomar Field on track to start production in mid-2024.

US Gas Rig Count Falls to Lowest Since January 2022

2024-03-22 - The combined oil and gas rig count, an early indicator of future output, fell by five to 624 in the week to March 22.

CNOOC Finds Light Crude at Kaiping South Field

2024-03-07 - The deepwater Kaiping South Field in the South China Sea holds at least 100 MMtons of oil equivalent.