In the week since our last edition of What’s Affecting Oil Prices, Brent averaged $63.10/bbl last week with prices strengthening through the week.

For the upcoming week Stratas Advisors expect prices to trade range-bound until the OPEC meeting when prices will likely take a leg down as markets are inevitably disappointed by the outcome. Prices will average $62.75/bbl next week. Stratas Advisors expects the Brent-West Texas Intermediate (WTI) differential to average $5.40/bbl as Brent loses more support than WTI.

The supporting rationale for the forecast is provided below.

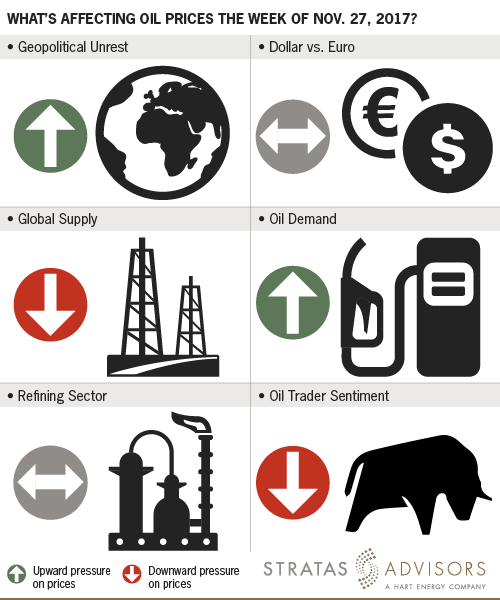

Geopolitical: Positive

Geopolitics as it relates to oil could continue to drive volatility, but is unlikely to have an additional immediate fundamental impact. However, the few active hotspots that bears watching are more likely to hamper oil supply, further helping prices.

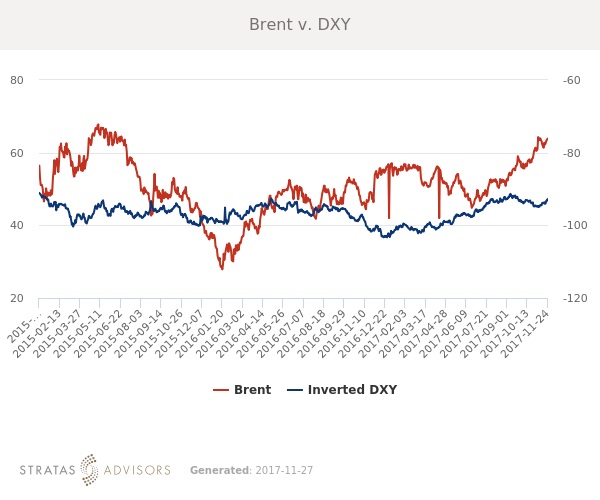

Dollar: Neutral

Crude oil and the dollar traded in line last week, but crude oil remains more influenced by fundamental factors and sentiment. The DXY is being driven by debate around tax reform as the deadline to pass legislation nears.

Trader Sentiment: Negative

Despite a small drop in managed money net longs last week, Brent positioning remains at record highs as traders await the outcome of this week’s OPEC meeting. As Stratas Advisors previously mentioned, the meeting is unlikely to end in a formal extension of the deal which is bound to disappoint and lead to a pullback in prices on negative sentiment.

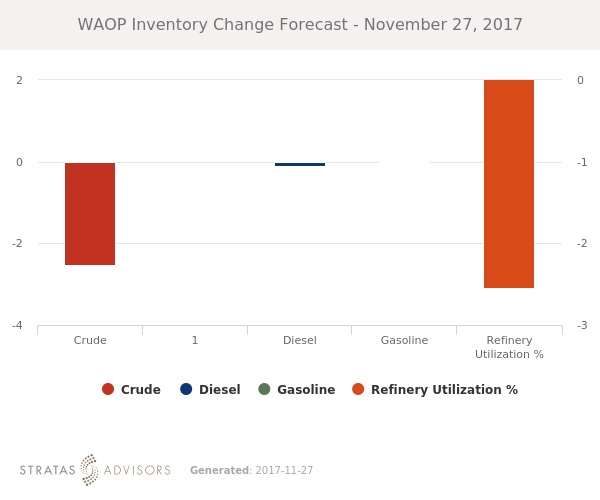

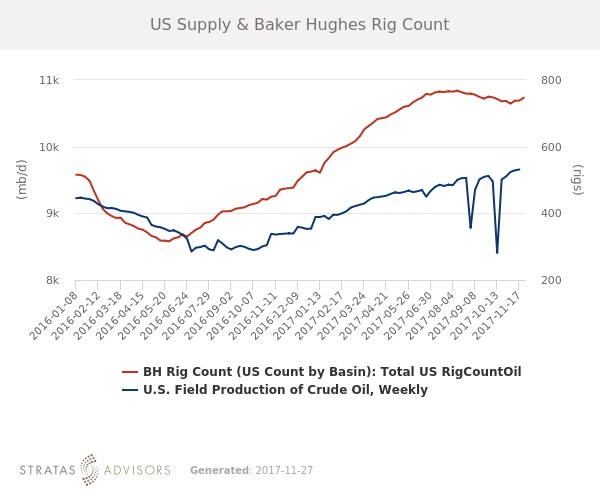

Supply: Negative

Last week the number of operating oil rigs in the U.S. rose by nine. U.S. oil rigs now stand at 747 compared to 474 in 2016. All eyes will be on the OPEC meeting later this week as markets anticipate an extension to the current supply deal. If a formal extension is not announced, markets will react negatively out of concern that oversupply could quickly return.

Demand: Positive

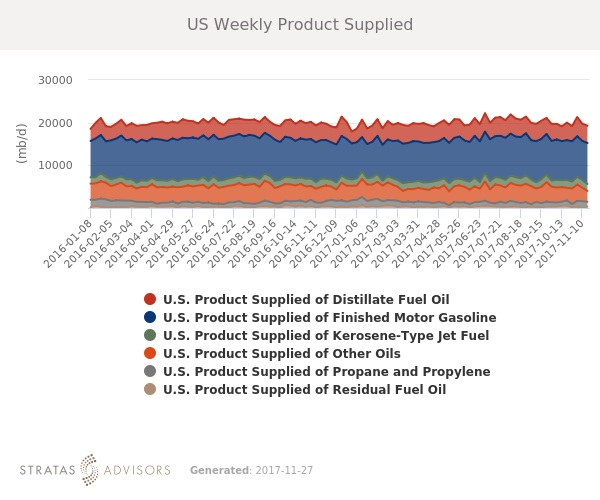

Demand remains healthy in the U.S., with strong product exports indicating a robust appetite elsewhere as well. Gasoline and distillate stocks are both below the five-year average on robust domestic demand and strong export flows. Demand is likely to remain strong through the end of the year on healthy holiday consumer spending and travel.

Refining: Neutral

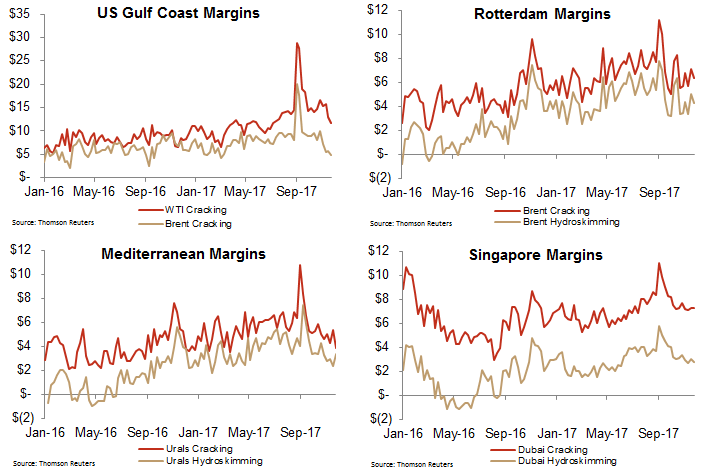

Margins were flat to down last week, but remain generally healthy. Combined with healthy global demand, current margins will continue to incentivize crude intake, but will not be enough to counteract negative sentiment out of the OPEC meeting.

How We Did

Recommended Reading

Elk Range Royalties Makes Entry in Appalachia with Three-state Deal

2024-03-28 - NGP-backed Elk Range Royalties signed its first deal for mineral and royalty interests in Appalachia, including locations in Pennsylvania, Ohio and West Virginia.

NOG Closes Utica Shale, Delaware Basin Acquisitions

2024-02-05 - Northern Oil and Gas’ Utica deal marks the entry of the non-op E&P in the shale play while it’s Delaware Basin acquisition extends its footprint in the Permian.

Chord Buying Enerplus to Create a Bakken Behemoth

2024-02-22 - Chord Energy said Feb. 21 it will acquire Enerplus Corp. for nearly $4 billion in a stock-and-cash deal to potentially create the largest producer in the Williston Basin.

Which Haynesville E&Ps Might Bid for Tellurian’s Upstream Assets?

2024-02-12 - As Haynesville E&Ps look to add scale and get ahead of growing LNG export capacity, Tellurian’s Louisiana assets are expected to fetch strong competition, according to Energy Advisors Group.

An Untapped Haynesville Block: Chevron Asset Attracts High Interest

2024-04-03 - Chevron’s 72,000-net-acre property in Panola County, Texas is lightly developed for the underlying Haynesville formation — and the supermajor may cut it loose.