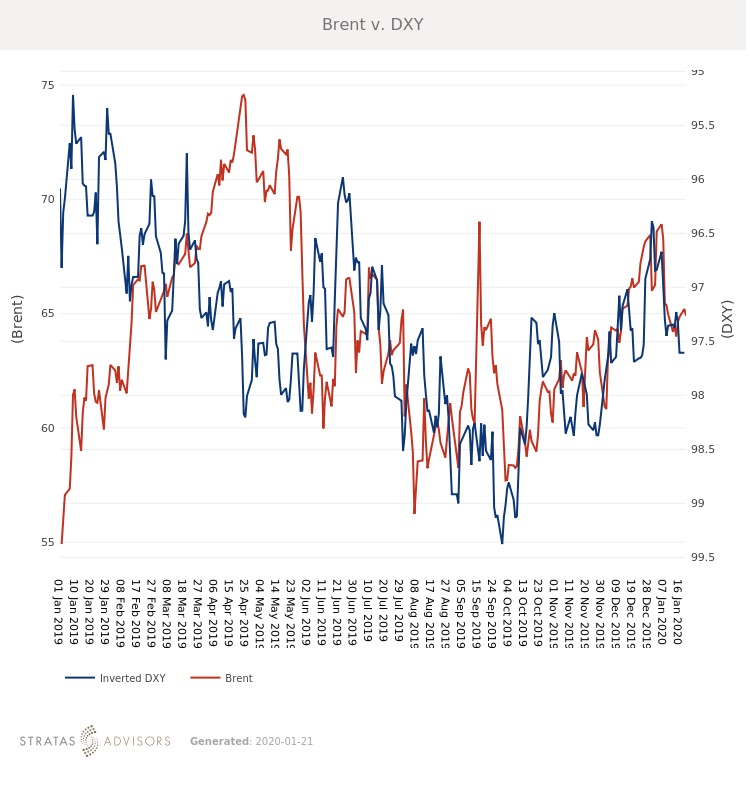

Brent fell $2.16/bbl last week to average $64.43/bbl, in line with Stratas Advisors' forecast. WTI fell $2.60/bbl to average $58.24/bbl. For the week ahead, Stratas Advisors expect Brent to continue drifting lower, likely averaging $63.50/bbl.

Little immediate bullish support for crude is present, but the recent signing of a U.S.-China trade deal helps provide a floor for prices. This week could see volatility in some Mediterranean-focused grades as Libyan supplies are interrupted once again. However, overall markets shrugged off the force majeure, as there is plenty of supply to fill the gap. Overall weakness in crude will likely continue through the first quarter per seasonal norms. The first quarter tends to see crude and product stock builds but any outsized movements in the U.S., Europe or Asia would still be viewed negatively. In China, Lunar New Year’s celebrations may entail less travel than usual as the country deals with outbreaks of a new coronavirus.

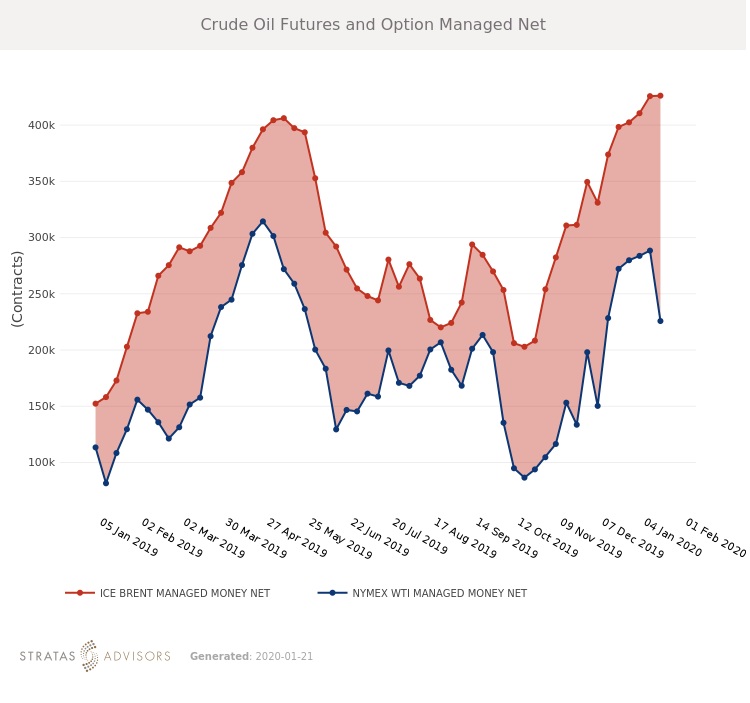

OPEC+ has been surprisingly silent about its plans for March. Some recent statements have indicated that there is room for an upside surprise in demand, but it is unclear how much that possibility is factoring into future actions. For now outages in Libya and Venezuela, along with generally decent compliance, are helping the organization meet its production goals. With Norway’s Johan Sverdrup field increasing deliveries, non-OPEC supply growth will be top of mind again and markets could be disappointed if stronger signals do not come from OPEC.

Geopolitical Unrest – Neutral

Global Economy – Neutral

Oil Supply – Negative

Oil Demand – Negative

Recommended Reading

No Silver Bullet: Chevron, Shell on Lower-carbon Risks, Collaboration

2024-04-26 - Helping to scale lower-carbon technologies, while meeting today’s energy needs and bringing profits, comes with risks. Policy and collaboration can help, Chevron and Shell executives say.

Solar Panel Tariff, AD/CVD Speculation No Concern for NextEra

2024-04-24 - NextEra Energy CEO John Ketchum addressed speculation regarding solar panel tariffs and antidumping and countervailing duties on its latest earnings call.

NextEra Energy Dials Up Solar as Power Demand Grows

2024-04-23 - NextEra’s renewable energy arm added about 2,765 megawatts to its backlog in first-quarter 2024, marking its second-best quarter for renewables — and the best for solar and storage origination.

BCCK, Vision RNG Enter Clean Energy Partnership

2024-04-23 - BCCK will deliver two of its NiTech Single Tower Nitrogen Rejection Units (NRU) and amine systems to Vision RNG’s landfill gas processing sites in Seneca and Perry counties, Ohio.