However, Stratas Advisors expects that the price of Brent crude will moderate and fall below $90, if the situation involving Ukraine is resolved without a major conflict, which the firm thinks is still the most likely scenario for several reasons, Stratas said in its latest oil prices forecast. (Source: Shutterstock.com)

Editor’s note: This report is an excerpt from the Stratas Advisors weekly Short-Term Outlook service analysis, which covers a period of eight quarters and provides monthly forecasts for crude oil, natural gas, NGL, refined products, base petrochemicals and biofuels.]

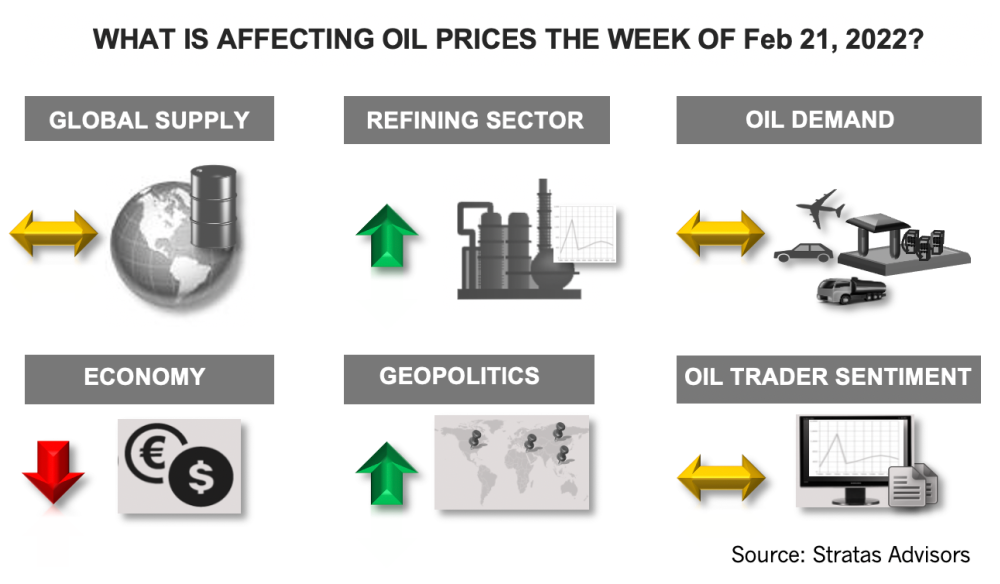

The price of Brent crude ended the week at $93.54 after closing the previous week at $95.10. The price of WTI ended the week at $91.66 after closing the previous week at $93.90.

As has been the case for the last several weeks, the impact of the Omicron variant continues to wane with cases from a global perspective decreasing by 38% and deaths by 6% over the last 14 days. Furthermore, cases are declining in all regions. Cases in the U.S. have dropped by 65% and the seven-day average number of cases now stands at 108,813, in comparison to the peak of 805,609 that occurred on Jan. 15. Deaths are also declining with daily average deaths falling by 13%. The world, as in 2021, seems to be poised for a six-month period with COVID-19 fading into the background.

However, we are expecting that the price of Brent crude will moderate and fall below $90, if the situation involving Ukraine is resolved without a major conflict, which we think is still the most likely scenario for several reasons. First, Russia has not assembled a large enough force to invade and take control of Ukraine. Such an objective would require a force several times larger. Second, Russia does not want to be viewed as an unreliable supplier of natural gas and oil. An invasion puts its hydrocarbon exports at risk. Third, there is little strategic value since it is obvious that Ukraine will not become a member of NATO, and the U.S. has agreed to negotiations pertaining to Russia’s concerns about the military capabilities being deployed by the U.S. and NATO in Eastern Europe. The wildcard is that Putin might hold the view that an invasion will result in a disagreement and fallout between the members of NATO, which will result in NATO losing credibility and effectiveness.

If there is an invasion, which results in extreme sanctions and significant disruption to Russian exports of crude oil and refined products (in the order of 6.5 million barrels overall and around 3 million bbl/d just in terms of export to Europe) oil prices will spike well above $100/bbl. Additionally, the impact on prices will last longer than was the case with the first Gulf War and the second Gulf War. During those conflicts, oil prices spiked, but then fell back quickly once the market realized that sufficient oil would still be supplied. During the first Gulf War, which lasted from Aug. 2, 1990 through Feb. 28, 1991, the oil market had significant level of spare supply capacity. During the second Gulf War, Iraqi production was already being sanctioned, so there was little impact on oil supply. The current situation is much different because of the magnitude of the potential loss of supply and that the oil market is in a much tighter supply/demand situation.

While we expect oil prices to moderate, we are still bullish on oil prices through the rest of this year and next year, with the average price of Brent crude remaining about $85. While an agreement between Iran and the U.S. would put downward pressure on oil prices, we remain skeptical that an agreement will be reach anytime soon. Iran is insisting on the removal of all sanctions before resuming compliance with the 2015 agreement. This demand cannot be met by the Biden Administration because a retreat of this nature does not have widespread support in the U.S. Additionally, Iran is unlikely to accept an agreement with the Biden Administration that is not effectively a treaty, which will need to gain two-third approval from the U.S. Senate. Without such an agreement, the next administration can reverse course, as did the Trump Administration. This requirement was highlighted by a group of 33 Republican Senators recently warning the Biden Administration that they would not support any agreement that did not involve Congress reviewing and voting on the terms. If an agreement is reached, Iran exports could increase back to around 2.5 million bbl/d, which would be an increase of around 1.3 million-1.7 million bbl/d.

The biggest downside risk to oil prices remains an economic slowdown, which could be triggered by some debt-related issue that arose during the pandemic. A downturn could also occur because central banks tightened too fast. The market is now excepting that the US Federal Reserve will move forward aggressively with multiple rate increases during 2022 and 2023. Additionally, the market is applying a high probability to the Federal Reserve increasing rates by 50-basis points at its next meeting on March 15 and 16. A key datapoint to watch out for is the Personal Consumption Expenditure Price Index, which will be reported on February 25, and is an important inflation metric for the Federal Reserve. Back in 2016, the Federal Reserve increasing rates eight consecutive quarters starting with fourth-quarter 2016 and ending in 4Q of 2018, with the Federal Fund Rate increasing from 0.50 to 2.5%. During that timeframe, the price of Brent crude increased from around $56 to $67, while the US Dollar Index fell from 102.21 to 97.28. The rate increases were not because of inflation concerns, but to get back to a more “normal” interest rate situation, which would provide the Federal Reserve with the ability to cut rates in the case of an economic slowdown. Another complicating factor is the balance sheet of the Federal Reserve. Currently, the Federal Reserve is reducing its monthly purchases of treasury and mortgage-backed security with the expectation that the purchases will end in March. In 2007, the balance sheet was only around $1 trillion. With the 2008/2009 economic crisis the balance sheet spiked to $2 trillion and then kept increasing to $4.5 trillion by 2014. The balance sheet then was reduced slowly and declined to $3.8 trillion by 2019. With the emergence of COVID-19 the balance sheet increased rapidly to $7.1 trillion by June 2020 and has continued to increase to $8.87 trillion. With respect to the economic growth, it would be more prudent to go slowly in shifting to a less accommodating monetary policy, but the concerns about inflation are pushing the Federal Reserve to act sooner than later—even though much of the inflation is resulting from supply chain issues, physical shortages and higher energy costs.

About the Author:

John E. Paise, president of Stratas Advisors, is responsible for managing the research and consulting business worldwide. Prior to joining Stratas Advisors, Paisie was a partner with PFC Energy, a strategic consultancy based in Washington, D.C., where he led a global practice focused on helping clients (including IOCs, NOC, independent oil companies and governments) to understand the future market environment and competitive landscape, set an appropriate strategic direction and implement strategic initiatives. He worked more than eight years with IBM Consulting (formerly PriceWaterhouseCoopers, PwC Consulting) as an associate partner in the strategic change practice focused on the energy sector while residing in Houston, Singapore, Beijing and London.

Recommended Reading

Russia Orders Companies to Cut Oil Output to Meet OPEC+ Target

2024-03-25 - Russia plans to gradually ease the export cuts and focus on only reducing output.

BP Starts Oil Production at New Offshore Platform in Azerbaijan

2024-04-16 - Azeri Central East offshore platform is the seventh oil platform installed in the Azeri-Chirag-Gunashli field in the Caspian Sea.

Tinker Associates CEO on Why US Won’t Lead on Oil, Gas

2024-02-13 - The U.S. will not lead crude oil and natural gas production as the shale curve flattens, Tinker Energy Associates CEO Scott Tinker told Hart Energy on the sidelines of NAPE in Houston.

What's Affecting Oil Prices This Week? (March 18, 2024)

2024-03-18 - On average, Stratas Advisors predicts that supply will be at a deficit of 840,000 bbl/d during 2024.

What's Affecting Oil Prices This Week? (March 11, 2024)

2024-03-11 - Stratas Advisors expects oil prices to move higher in the middle of the year, but for the upcoming week, there is no impetus for prices to raise.