Source: Shutterstock.com

[Editor's note: A version of this story appears in the November 2019 edition of Oil and Gas Investor. Subscribe to the magazine here.]

Mineral and royalty buyers are often required to assign value to miscellaneous, lower dollar-value, nonproducing minerals. Buyers know how they want to price producing royalties and properties in attractive areas likely to get developed in the near term, but they rarely have confidence assigning value to mineral tracts that may be unleased and located in a county where there is little ongoing oil and gas development.

Historically, the market has used an approach referred to as the multiple of lease bonus method (MLBM). The MLBM suggests that the value of nonproducing minerals may be equal to a multiple of 2.5x to 3x a representative lease bonus. For example, if minerals in an area are being leased for $200 per acre, the MLBM suggests the minerals are worth $500 to $600 per net mineral acre. The MLBM is based on the logic that a mineral owner may lease and re-lease (upon expiration of the earlier lease) the subject minerals multiple times over the course of an assumed holding period, earning a lease bonus payment upon each new lease.

However, as is widely known, there are many shortcomings to the MLBM approach. The 2.5x to 3x range is somewhat arbitrary, and lease bonus income is not the sole source of mineral income. Also, the amount of lease bonus paid by a lessee is often contingent on or interrelated with the royalty rate so the MLBM would theoretically overvalue minerals where the lessor negotiated a high lease bonus rate at the expense of a lower royalty rate. Moreover, it can be difficult to define a representative lease bonus rate, especially during periods of rapidly changing lease bonus rates.

We considered market evidence to evaluate the accuracy of MLBM. We analyzed transaction data for 87 nonproducing mineral properties (lots) sold by EnergyNet from January 2013 to October 2018. EnergyNet is a major player in this marketplace. In 2018, EnergyNet sold over 2,300 separate lots (of all property types, including nonproducing minerals) with an aggregate sales value of approximately $2.2 billion.

EnergyNet provided us with confidential and anonymized data on more than 500 nonproducing mineral transactions during this period. We added other data points to this data set, including drilling permit counts, rig counts by county and lease bonus information, to create the master database described in this article.

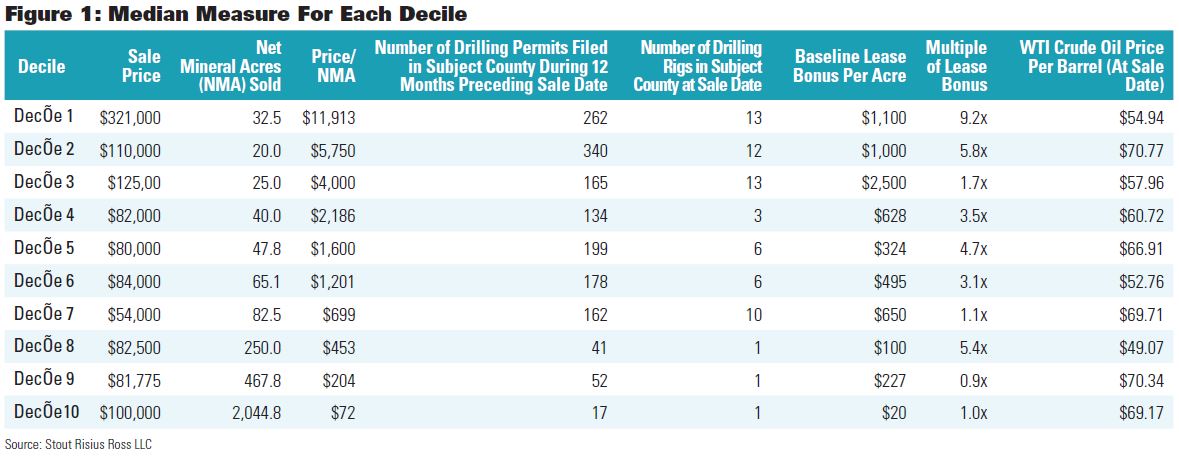

Nonproducing mineral transaction database

The 87 transactions were sorted by selling price per net mineral acre (price/NMA) from highest to lowest and categorized the data into deciles. For each decile, we calculated a median, as shown in Figure 1. The data points include sales price, net mineral acres sold, price/NMA, baseline lease bonus and the other items shown.

The main takeaway from the market study is that the actual price/NMA was widely divergent from the values predicted by the MLBM. Less than 5% of the 87 transactions had an MLB between 2.5x and 3x. About 23% of the transactions had an MLB of less than 1x.

A market-based valuation framework

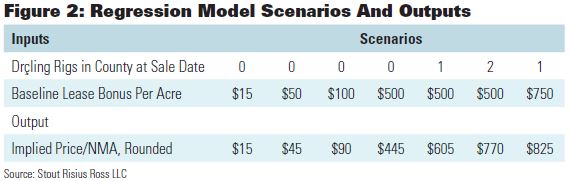

So, if the MLBM is not a reliable nonproducing mineral valuation model, can the market data be used to develop an alternative valuation approach? Using multiple variable regression, we attempted to develop an equation that could be used to predict nonproducing mineral values.

We recognized going into the analysis that there are multiple factors that impact mineral valuation, and our independent variables were based on more general, countywide data rather than data on a more specific area surrounding the subject minerals (such as a 5-mile radius).

After running the regression analysis, we found that the baseline lease bonus and drilling rig count (independent variables) were significant drivers of mineral value but other factors should be considered in developing value. A sample output from the model is shown in Figure 2.

The predicted values from the model could be high or low relative to true market value, depending on other factors not captured in the regression model. The most important other factor is the specific location of the minerals within the subject county. For example, mapping may show that the subject minerals lie far from or just outside a clearly defined permitting and development area, in which case the model’s value likely would need to be adjusted downward.

Other factors that influence nonproducing mineral value and should be considered in the valuation include oil and gas lease terms (royalty rate, gross or net royalty provisions, acreage retention language and continuous drilling clauses), the technical capability and drilling budget of the lessee or operator, the status of the minerals (for example, whether the subject minerals are HBP or recent permits have been filed directly on or close to the subject tract), size of the mineral tract, outlook for commodity prices, takeaway infrastructure in the area, and political or environmental issues.

Mineral valuation in high-value, rapidly developing areas

The framework discussed in this article is not highly useful for high dollar-per-acre minerals. High-value areas include promising geological areas where lease bonus rates, drilling permits and drilling rig counts are high.

A current example would be the Midland and Delaware sub-basins of the Permian Basin where nonproducing minerals are selling for $10,000 to $20,000 per NRA (net one-eighth royalty acre). For high-value, rapidly developing areas, the valuation process typically involves an Income Approach based on an engineering drill-out analysis as well as a market approach based on price-per-acre data.

In these areas, transaction data are more readily available (but still very difficult to obtain) because of buying by publicly traded mineral buyers as well as other funds which may be required to report the data. In these areas, the market approach is based on a price/NRA basis rather than a price/NMA basis.

A defensible approach

Mineral valuation cannot be mechanized or boiled down to a formulistic approach. Many variables are involved in the process, and professional judgment is required. The regression model discussed herein is based on market transaction data and should be a more defensible valuation approach for miscellaneous, nonproducing minerals if used as a starting point as compared to the commonly used MLBM.

___________________________________________________________________________________

Alan Harp Jr. is a managing director in the valuation advisory group of Stout Risius Ross LLC’s Houston office. The author wishes to thank EnergyNet for its assistance and for providing the market transaction data used to develop this article, and Stout interns Phillip Schwartz and Joel Ompendoguelet for their research and other assistance.

Recommended Reading

Exclusive: Chevron New Energies' Bayou Bend Strengthens CCUS Growth

2024-02-21 - In this Hart Energy LIVE Exclusive interview, Chris Powers, Chevron New Energies' vice president of CCUS, gives an overview of the company's CCS/CCUS activity and talks about the potential and challenges of it onshore-offshore Bayou Bend project.

Exclusive: Tenaris’ Zanotti: Pipes are a ‘Matter of National Security’

2024-04-12 - COVID-19 showed the world that long supply chains are not reliable, and that if oil is a matter of U.S. national security, then in turn, so is pipe, said Luca Zanotti, U.S. president for steel pipe manufacturer Tenaris at CERAWeek by S&P Global.

Exclusive: As AI Evolves, Energy Evolving With It

2024-02-22 - In this Hart Energy LIVE Exclusive interview, Hart Energy's Jordan Blum asks 4cast's COO Andrew Muñoz about how AI is changing the energy industry—especially in the oilfield.

Chesapeake, Awaiting FTC's OK, Plots Southwestern Integration

2024-04-01 - While the Federal Trade Commission reviews Chesapeake Energy's $7.4 billion deal for Southwestern Energy, the two companies are already aligning organizational design, work practices and processes and data infrastructure while waiting for federal approvals, COO Josh Viets told Hart Energy.

Exclusive: Sabine CEO says 'Anything's Possible' on Haynesville M&A

2024-04-09 - Sabine Oil & Gas CEO Carl Isaac said it will be interesting to see what transpires with Chevron’s 72,000-net-acre Haynesville property that the company may sell.