Many operators in the U.S. shale patch appear reluctant to substantially increase drilling beyond original plans based on much lower oil price expectations. (Source: Shutterstock.com)

Oil prices spiked above $100/bbl on Feb. 24 after Russia launched an invasion of Ukraine, piling pressure on a global economy already reeling from rampant inflation.

Since then oil prices have fallen back below $100/bbl but still remain high, which coupled with continued discipline from some OPEC members, is expected to lead to a global increase in drilling activity this year. However, in the U.S. shale patch, many operators appear reluctant to substantially increase drilling beyond original plans based on much lower oil price expectations, according to a new report from Westwood Global Energy Group.

U.S. independents, which account for more than 50% of shale production, are wary of ramping up activity to levels seen in the past, and have instead remained focused on returning capital to shareholders. For example, public operators like Pioneer Natural Resources and Devon Energy have announced limiting 2022 production increases to no more than 5%, compared to the 20% plus annual growth targets set pre-COVID.

“A high oil price, coupled with the increased focus on the most productive shale plays mean that they can achieve higher returns without the need to ramp up drilling activity to previous levels where 38,000 wells were drilled a year,” the report noted.

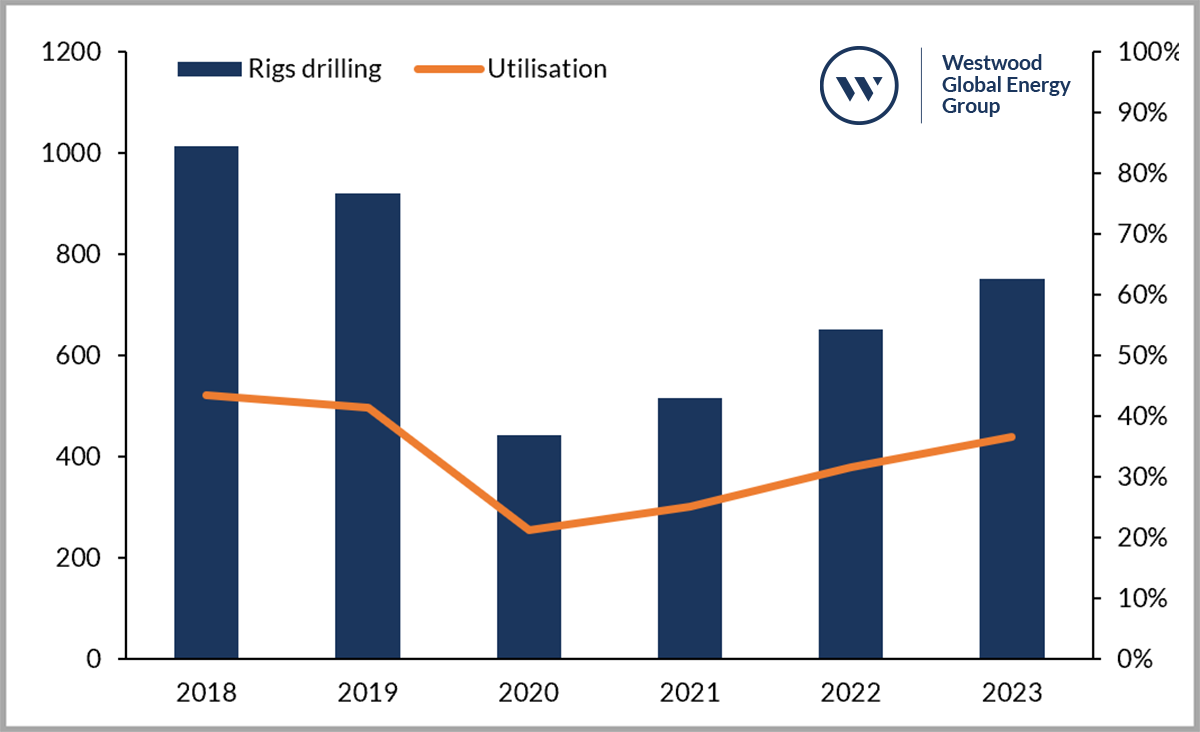

Westwood expects 13,000 wells to be drilled in 2022 followed by 15,000 wells in 2023. As a result, the number of rigs drilling in the U.S. is expected to average 650 in 2022 and 751 in 2023. While some smaller companies have already increased their 2022 rig guidance versus their 2021 average, many of the larger E&Ps intend to have similar rig counts this year, such as Pioneer who intends to run 23 rigs in 2022, the same as it did in 2021.

For E&Ps who have linked any increase in their drilling and completion (D&C) activity to changes in market fundamentals, sustained high commodity prices will be a true test of discipline.

“Targets such as a return to pre-COVID demand levels and diminished OPEC+ spare production capacity have been key targets for companies such as EOG and Devon Energy. Even if these criteria are met, several factors could limit E&Ps’ ability to effectively increase their production,” the report stated.

HHP utilization

U.S. has seen a significant increase in frac fleet hydraulic horsepower (HHP) utilization, which stood at 82% in the fourth quarter of 2021, including nearly 90% in the Permian, Westwood’s report noted.

HHP utilization is being exacerbated by backlogs in Tier 4 dynamic gas blending (DGB) engines, which are sought after by E&Ps for their reduced emissions and fuel savings because to their ability to displace 80% of diesel with natural gas compared to their non-DGB diesel counterparts.

“To meet a sudden increase in HHP demand, pressure pumpers would need to spend millions of dollars per fleet on their legacy diesel Tier 2 fleets. That is a cost which may be unjustifiable given that many pressure pumpers would prefer long-term contracts to re-activate fleets. Without such commitments, pressure pumpers will instead seek to hold steady their number of deployed crews in 2022,” the report said.

Takeaway capacity

Westwood’s report also noted that takeaway capacity could limit E&Ps’ ability to increase their D&C activity, especially in the Appalachian Basin where nearly 2.8Bcf/day of potential takeaway capacity has been removed through the cancellation of the Atlantic Coast and PennEast pipelines. Additionally, delays in the Mountain Valley Pipeline construction have kept 2 Bcf/d of takeaway capacity from being utilized.

“During EQT’s 2021 Q4 earnings conference call, CEO Toby Rice estimated that nearly 8 Bcf/d of takeaway capacity remains unrealized due to either cancellations or delays in the Appalachia basin region. That unrealized takeaway capacity is equivalent to 7.6% of the EIA’s projected 2022 marketed natural gas production in the U.S.,” the report said.

Recommended Reading

CEO: Devon Eyes 3-Mile Williston Wells With $5B Grayson Mill Deal

2024-07-08 - Devon Energy is digging deeper in the Williston Basin of North Dakota through a $5 billion deal with EnCap-backed Grayson Mill Energy.

It’s All Relative: Family Oil Companies Attract Huge M&A Attention

2024-07-01 - What role do firms controlled by descendants of the original Permian Basin wildcatters play in a sector increasingly dominated by scale?

Solaris to Acquire Mobile Energy Rentals, Rename to Solaris Energy Infrastructure

2024-07-10 - Following the closing of its deal to acquire Mobile Energy Rentals, Solaris Oilfield Infrastructure will also be rebranding to Solaris Energy Infrastructure to more closely represent its expanded solutions offerings.

Come Together: California Resources, Aera Merge for Scale, Drilling Runway

2024-07-10 - California Resources Corp. closed an acquisition of Aera Energy to become California’s top oil and gas producer. Now, CRC President and CEO Francisco Leon wants to grow from a one-rig to an eight-rig drilling program—but faces stiff pushback from regulators and environmental advocates in the Golden State.

Blackstone Buys Enagás’ Tallgrass Stake for $1.1 Billion

2024-07-11 - Spain’s Enagás is selling its Tallgrass Energy interests to Blackstone Infrastructure Partners in exchange for some needed capital.