The midstream sector has been in a period of stability over the past year and, in the case of M&A, relatively quiet. (Source: Shutterstock)

MIDLAND, Texas — The midstream sector has brought in a lot of cash in 2023, but so far, its windfall is being used to pay down debt rather than capex or M&A. That may change soon, particularly as companies look for deals to expand scale.

For now, most midstream businesses are paying careful attention to cash flow, Stephen Lipscomb, a partner at private equity firm Tailwater Capital, said at Hart Energy’s Executive Oil Conference and Exhibition.

“It's all about capital efficiency. That's the name of the game for these guys right now,” said Lipscomb, who specializes in energy Infrastructure.

In 2023, the overall midstream sector is expected to log in $42 billion worth of free cash flow while lowering leverage to x4.3. Both stats are the best for the sector in the past decade.

“Free cash flow is at an all-time high for public midstream companies, but that free cash flow has not been deployed as much into growth capex as it's been used to pay down debt,” he said.

Since 2019, the midstream sector saw a drop of about 46% in capex spending. Lipscomb said many companies are focusing on distributing cash back to shareholders for various reason. For one, they are otherwise risk averse in starting large projects. And the sector does not have to spend a great deal on capex because most U.S. construction projects for long-haul transport and fractionation gathering and processing have already occurred.

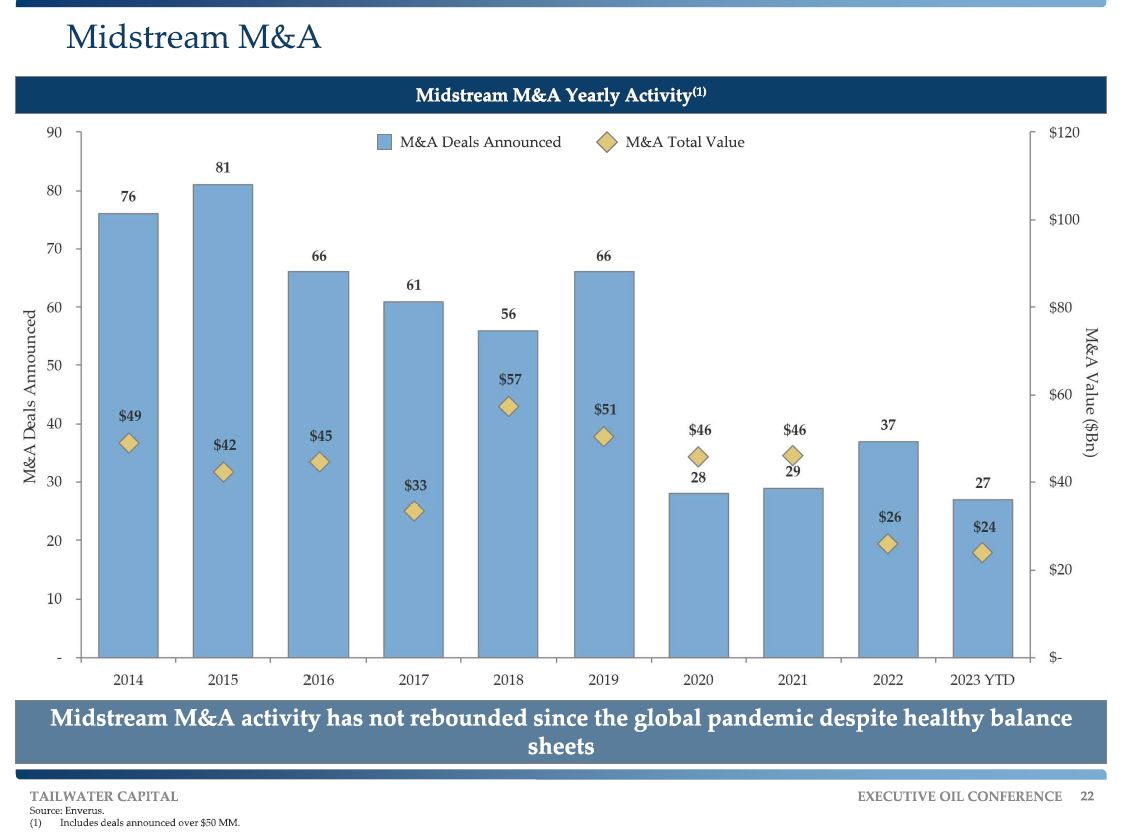

The midstream sector has been in a period of stability over the past year and, in the case of M&A, relatively quiet. While some major deals have transacted, including ONEOK’s $18.8 billion purchase of Magellan Midstream in September, M&A activity and deal values continued to slide.

Through 10 months of 2023, the midstream deal market hit a decade low, with 27 announced deals valued at a total of $24 billion. That comes on the heels of 2022, in which 37 deals transacted for $26 billion — a value that was the previous low for the decade.

However, the healthy financials of midstream companies may eventually kick M&A activity back into gear, particularly if companies can make the case that it adds to shareholder returns.

With much of the large-scale infrastructure needed in Texas is already in place, companies may start to consolidate for a better strategic space in the market.

“It's much easier to make an acquisition as an immediate step towards accretion in your distribution,” Lipscomb said. Investors will eventually be attracted back towards financially healthy companies for the next round of acquisitions.

Midstream growth by E&Ps

With a few major midstream projects underway, such as Equitrans Midstream's Mountain Valley Pipeline in West Virginia and Virginia, most sector growth would happen on an incremental basis in the Permian Basin.

And amid the reluctance by midstream companies to spend, Lipscomb said he’s seeing movement by upstream players.

Pipelines will follow the supply development, and the Midland and Delaware basins areas are driving growth, rather than seeing new major projects coming online.

RELATED

Targa Resources Weighs Whether Building Apex Pipeline is Best Move

Lipscomb cited a Goldman Sachs analysis showing that capex for “megaprojects” in E&P has declined from an average of $65 billion a year from 2018 to 2022, while spending averaged $108 billion from 2003 to 2017.

Instead, the U.S, has been the sole contributor to an increase in worldwide oil production — from 14 MMbbl/d since 2010 to 101 MMbbl/d in 2023 — mainly through the development of shale in the Permian.

However, as many productive fields become more gassy and less oily, the E&P sector is expected to move into less developed terrain and away from the basin’s core areas.

Lipscomb, citing energy research firm East Daley among other sources, said the Permian has about five years of the core Tier 1 inventory left. “Everyone can dispute that number. That's always a hot topic in our shop as well. But the truth is, Tier 1 inventory is finite,” he said.

E&P companies are already migrating from the core areas of the Midland and Delaware. That expansion should turn into a growth market for midstream companies that will be extending their current infrastructure.

Lipscomb also sees growth as E&P companies seek to avoid increased restrictions on flaring.

Production companies will need to seek out partnerships with the midstream segment, he said, as the market for equity to pay for large projects is tight.

“The unfortunate truth for upstream operators is, if you are wanting to build or have midstream infrastructure and solve any sort of flaring issues, then you're either going to need to build it yourself — which is not something I'm advocating — or you're going to have to work with the private midstream operators and help them from a risk-return standpoint.”

Recommended Reading

US Drillers Cut Oil, Gas Rigs for Third Week in a Row, Baker Hughes Says

2024-08-30 - The rig count is 8% below this time last year, according to Baker Hughes.

Helix Awarded Vessel Service, Charter Contracts Off Brazil

2024-08-28 - Helix Energy Solutions Group was awarded new three-year charter and service contracts, valued at an estimated $786 million, from Petrobras for Siem Helix 1 and Siem Helix 2.

Shell, Akselos Enter Enterprise Deal for Structural Performance Management

2024-08-28 - Shell Information Technology International will leverage Akselos’ structural performance management software to monitor the health and lifecycle of Shell’s critical assets in Qatar, Canada, the Gulf of Mexico and elsewhere.

From Exxon to APA, E&Ps Feel Need to Scratch Exploration Itch

2024-08-27 - Exxon Mobil is looking for its “next Permian,” which an executive said could be in Algeria.

E&P Highlights: Aug. 26, 2024

2024-08-26 - Here’s a roundup of the latest E&P headlines, with Ovintiv considering selling its Uinta assets and drilling operations beginning at the Anchois project offshore Morocco.