The theory that long-term contracts ensure the profitability of midstream public companies no longer appears as convincing to investors, at least not in a post-Sabine world in which “covenants that run with the land” is not a certain guideline.

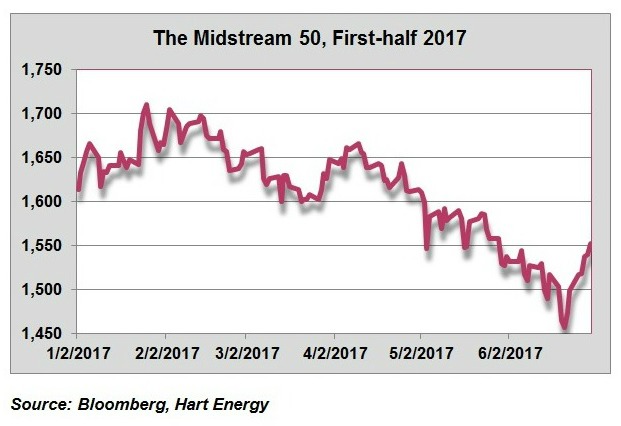

From its high to its low, the Midstream 50 index of leading companies in the sector suffered a 14.8% loss of value in first-half 2017, but a late charge near the end of June tempered the setback to only 3.8%.

Given the struggles endured by the rest of the oil and gas industry, most midstream operators won’t complain.

Given the struggles endured by the rest of the oil and gas industry, most midstream operators won’t complain.

Upstream brethren have been rocked so far this year. The S&P Oil & Gas Exploration & Production Select Industry Index tumbled by 23% in the first six months, and the broader S&P 500 Energy gauge showed a 13.8% drop in value. The Dow Jones industrial average rose 8.0% in the first half.

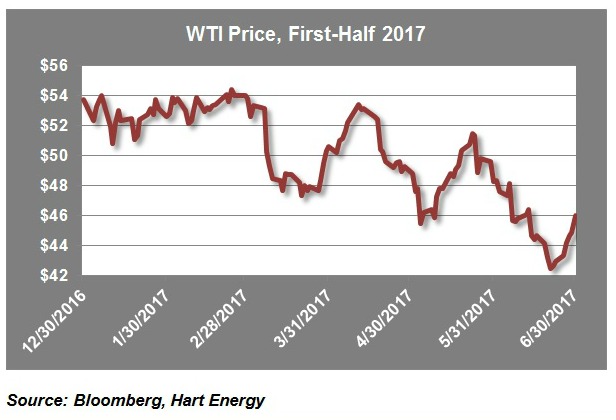

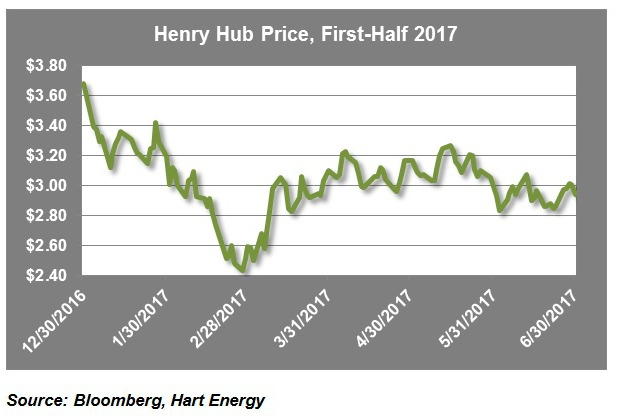

The industry has been gripped by volatile commodity prices that have periodically rallied from low points ($42.53 per barrel [bbl] in late June for West Texas Intermediate [WTI]; $2.44 per MMBtu in late February for Henry Hub natural gas) but not sustain those rallies.

During the first half of 2017, the price of WTI on the New York Mercantile Exchange fell by 14.3% to $46.04/bbl. The NYMEX price of Henry Hub natural gas took a 20% hit.

NGL, which tend to float between oil and gas, struggled even more. Hart Energy’s hypothetical NGL barrel based on prices at the Mont Belvieu, Texas, hub lost 21.5% of its value in the first six months.

NGL, which tend to float between oil and gas, struggled even more. Hart Energy’s hypothetical NGL barrel based on prices at the Mont Belvieu, Texas, hub lost 21.5% of its value in the first six months.

Notions of a rigged system afflicting the industry are not symptoms of paranoia but of the root cause of commodity price troubles: too many rigs are drilling in the U.S. with the unhappy result that “the U.S. industry has drilled itself right back into a lower price situation,” David Blackmon of DBEnergy Advisors wrote in Forbes.

Blackmon’s conclusion, what he terms the “pesky new reality for crude prices,” is a type of low-price paradigm on crude oil prices in which they seesaw between $40/bbl and $60/bblfor years.

Blackmon’s conclusion, what he terms the “pesky new reality for crude prices,” is a type of low-price paradigm on crude oil prices in which they seesaw between $40/bbl and $60/bblfor years.

More near term, Macquarie Research continues to be bullish about midstream infrastructure fundamentals but doesn’t expect EBITDA to increase until later in 2017. Macquarie points to new pipelines coming online now that won’t impact balance sheets for a while.

With the exception of the Plains All American Pipeline LP project from Midland, Texas, to Cushing, Okla., new projects, especially from the Permian Basin to Corpus Christi, Texas, will not get final investment decisions in the near future. Investors will hesitate, Macquarie said, out of fear of overbuilding during lean times and a reluctance to endure low returns.

Joseph Markman can be reached at jmarkman@hartenergy.com and @JHMarkman.

Recommended Reading

Eni Finds 2nd Largest Discovery Offshore Côte d’Ivoire

2024-03-08 - Deepwater Calao Field’s potential resources are estimated at between 1 Bboe and 1.5 Bboe.

Deepwater Roundup 2024: Offshore Australasia, Surrounding Areas

2024-04-09 - Projects in Australia and Asia are progressing in part two of Hart Energy's 2024 Deepwater Roundup. Deepwater projects in Vietnam and Australia look to yield high reserves, while a project offshore Malaysia looks to will be developed by an solar panel powered FPSO.

Cronos Appraisal Confirms Discovery Offshore Cyprus

2024-02-15 - Eni-operated block partner TotalEnergies says appraisal confirms the presence of significant resources and production potential in the block.

Deepwater Roundup 2024: Offshore Africa

2024-04-02 - Offshore Africa, new projects are progressing, with a number of high-reserve offshore developments being planned in countries not typically known for deepwater activity, such as Phase 2 of the Baleine project on the Ivory Coast.

Valaris Updates Fleet Status

2024-02-19 - The backlog of these contracts and extensions is valued at $1.2 billion.