Despite large-cap publics such as Devon Energy, Diamondback and Marathon Oil dominating M&A in 2022, the overall deal count fell to the lowest level since 2005, according to Enverus. (Source: Shutterstock.com)

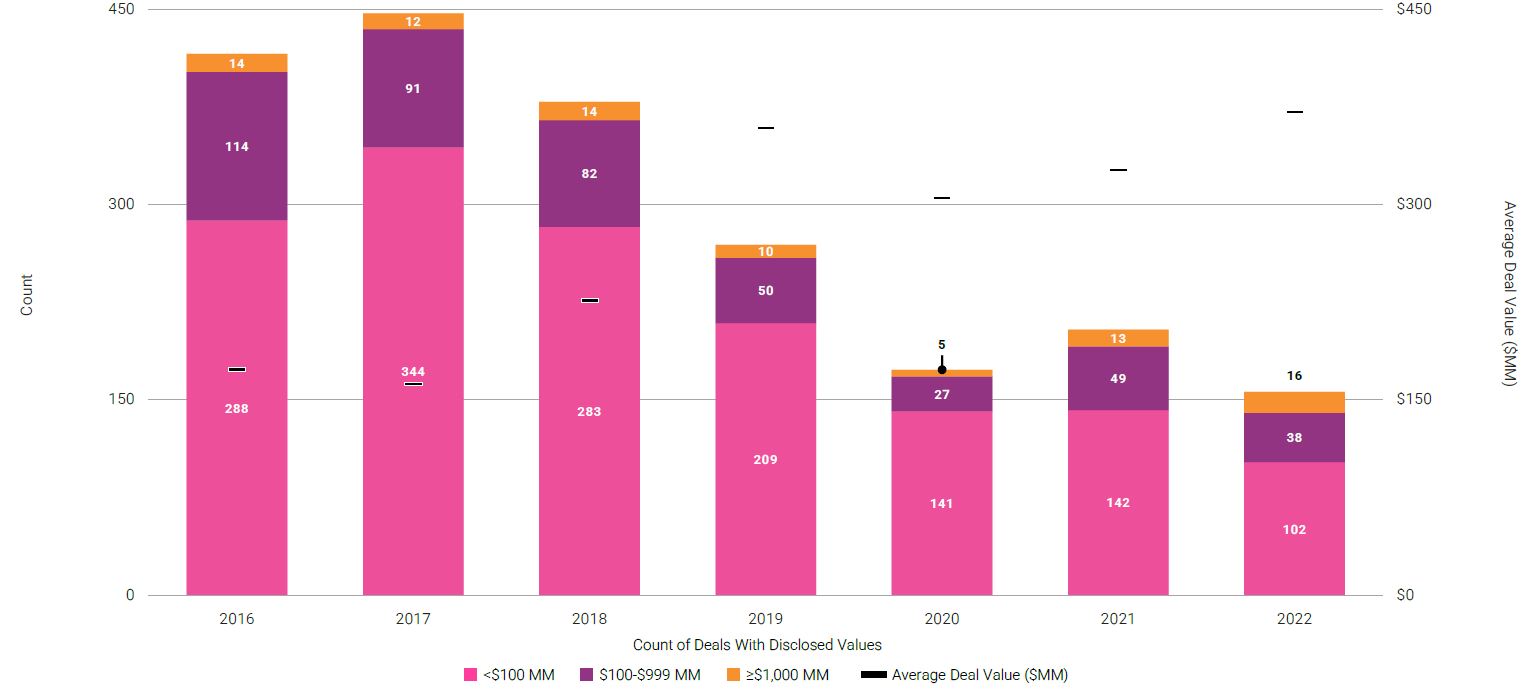

Upstream M&A stirred up a witch’s brew in 2022 with big deals helping to obscure a noxious year. Value plunged 13% year-over-year, while deal activity fell to the lowest level since 2005 and was down by 24% for the year, according to Enverus Intelligence Research.

Still, dealmakers found an occasional trigger to pull on transactions — particularly, large, independent E&Ps that shook loose acquisitions for smaller private companies in the Eagle Ford and Permian Basin in the second half of the year.

“Large-cap public companies like Devon Energy, Diamondback Energy and Marathon Oil dominated deal activity in the back half of 2022,” said Andrew Dittmar, director at Enverus Intelligence Research. “These buyers have the balance sheet strength and favorable stock valuations to take advantage of large, high-quality offerings from private sellers.”

RELATED

A ‘Strange and Broken’ Year For M&A

But the year also illustrated the widening mismatch between large-cap companies with attractive valuation and their smaller rivals, which are unable to compete for deals on an equity basis. Economic headwinds and commodity prices may also be at play in stifling M&A.

But in 2023, the persistent need to replenish inventory will likely keep E&Ps chasing deals.

Dittmar said that in 2022, large-cap companies were able to strike deals that were both accretive to current cash flow and extended their runway of drilling locations.

“For smaller companies, which are still having their equity value discounted, it is challenging to thread the needle of buying assets at accretive multiples and being able to pay for inventory,” he said.

Last year, deals appeared to split along two trend lines. Earlier in the year, transaction value was “heavily tilted toward production value as deals were focused on buying discounted production or modestly priced inventory,” Dittmar said.

By the fourth quarter, large-cap buyers were more willing to pay for inventory with valuations exceeding $2 million per location — including the deals by Diamondback and Marathon Oil.

“Given the need for inventory, we anticipate deals will continue to see more value allocated to the upside, both from paying more per location and targeting less developed assets with more development runway,” Dittmar wrote in the report.

Commodity prices, volatility dampen M&A

The slowdown in M&A may indicate that broader macro trends are at work, Dittmar said. The lessening of upstream M&A activity may be partly tied to a “broad, multi-industry M&A slowdown as central banks continue to tighten fiscal policy,” Dittmar wrote in a Jan. 18 report.

“We anticipate M&A could remain challenged this year until more clarity is reached on recessionary risks and the outlook for commodity prices,” Dittmar said.

Dittmar said deals also reacted significantly to prices and volatility.

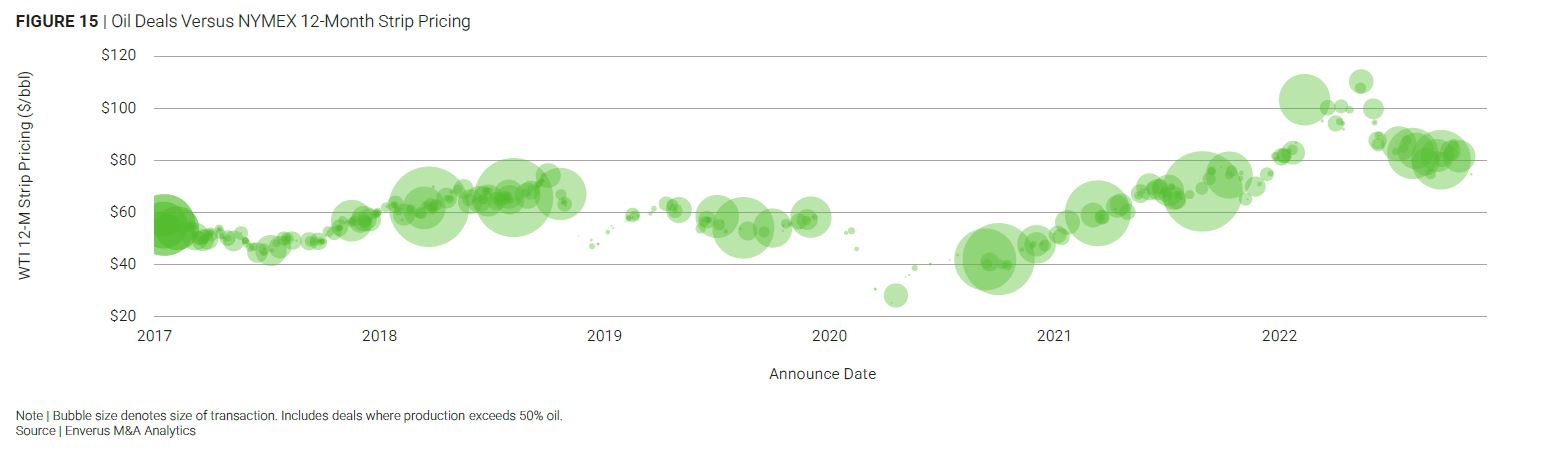

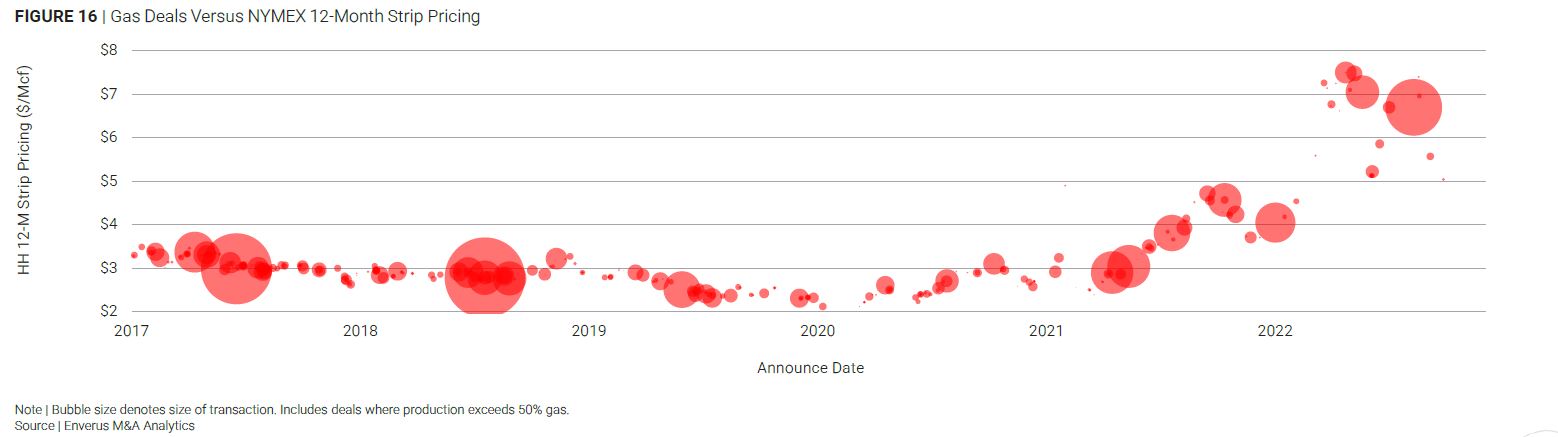

From July to December, spot WTI prices fell 25% at $25/bbl to end at an average $76.44/bbl. Henry Hub spot prices likewise lost 24% of their value, ending December at an average $5.53/MMBtu.

Following a spike in mid-2022, prices generally stabilized at $80/bbl for oil. Gas prices remained highly volatile, making deals tougher to negotiate, Dittmar said.

“In 2023, oil prices are likely to provide more support for deals, particularly in the first half of the year. The decline in gas prices likely provides an attractive buying opportunity, but asset holders may be reluctant to sell with relief for prices on the horizon in a few years from LNG buildout,” he said.

Inventory is life

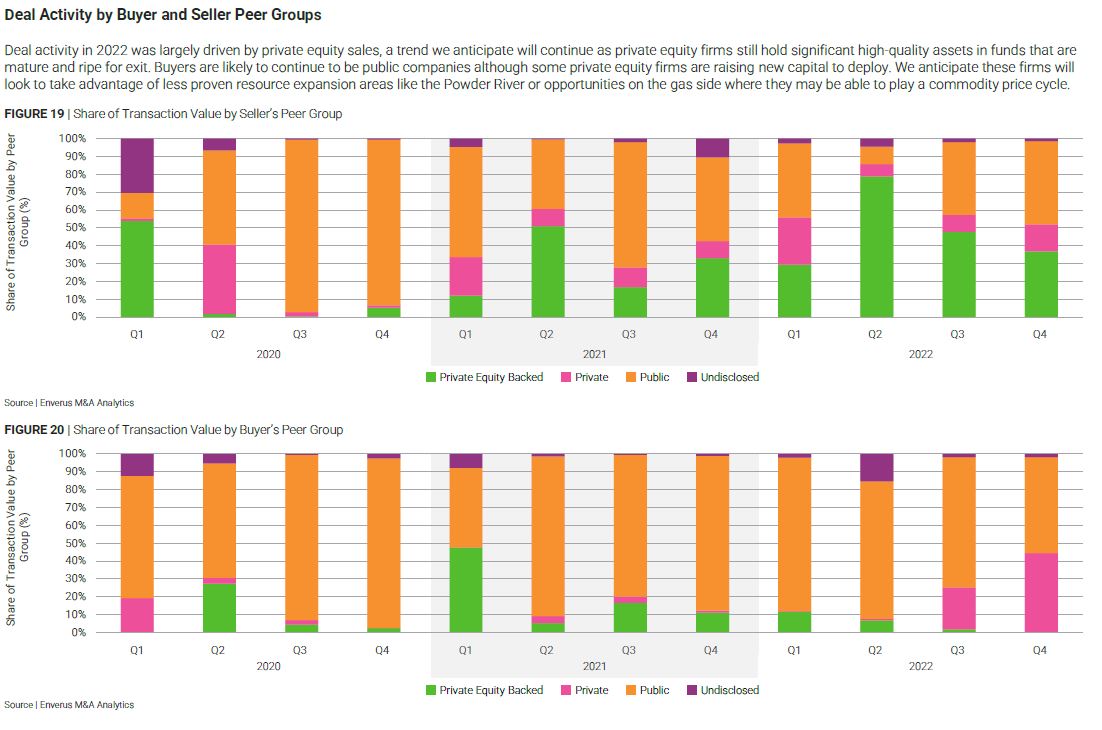

The need for public operators to secure inventory should provide a tailwind for M&A and private equity-backed sellers with high-quality asset packages.

Large-cap companies that have a premium valuation will “target the highest quality inventory in the core of plays—like the Permian and Eagle Ford for oil and Appalachia and Haynesville for gas,” Dittmar said. “Inventory in these plays is likely to continue to increase in value as fewer quality positions with scale remain.”

That disconnect hasn’t been lost on small- and mid-cap (SMID cap) E&Ps, such as Midland Basin operator HighPeak Energy Inc. On Jan. 23, the company, which has a market cap of about $3 billion, said it would explore a possible sale. Jack Hightower, HighPeak’s chairman and CEO, said the company is undervalued by the market — a point he effectively turned into a sales pitch.

“We believe our share price should move up the trading multiples currently realized by certain potential purchasers and large-cap pure play owners of Midland Basin assets,” he said.

Dittmar said SMID operators that need inventory but lack a supportive equity price may target less-proven areas, such as the Permian Rim and eastern Eagle Ford for oil and the Rockies regional plays for natural gas.

“A SMID-cap operator could test the market with a deal that is inventory accretive but dilutive to EBITDA multiples and free cash flow,” Dittmar said.

However, even if such a deal is strategically necessary, it may prove unpopular with investors over the short term. “Another option is a return to public-public M&A, either from SMID mergers seeking to garner a higher multiple from increased scale or to sell to a large-cap peer that is more attractive to investors,” he said.

‘The rich get richer’

For 2023, M&A dynamics appear likely to remain dependent on market capitalization and private sellers.

As in 2022, private equity is likely to continue to be the most active group of sellers in the deal market, Enverus said.

In part, capital providers still have substantial investments in oil and gas to unwind, either because they are coming up against the end of a fund life, for ESG reasons, or both. Public companies’ appetite for inventory is giving them an ideal window to sell.

However, there appears to be few “fire-sale bargains” to be had, and sellers are willing to walk away from a deal if none of the offers meet their minimum price, Dittmar said.

| Deal Values by Region and Type, 2022 | |||||

|---|---|---|---|---|---|

| Multi Region | 1Q22 | 2Q22 | 3Q22 | 4Q22 | % of 4Q22 |

| Multi Region | $0.3 | $3.5 | $2.2 | $5.2 | 39% |

| Permian | $4.4 | $6.1 | $1.1 | $4.2 | 32% |

| Gulf Coast | $0.0 | $0.6 | $2.0 | $3.1 | 23% |

| West Coast | $0.1 | $0.3 | $3.9 | $0.6 | 5% |

| Rockies | $7.3 | $1.4 | $0.1 | $0.1 | 1% |

| Midcontinent | $0.1 | $0.9 | $0.2 | $0.0 | 0% |

| Ark-La-Tex | $0.0 | $0.2 | $0.1 | $0.0 | 0% |

| Eastern | $2.7 | $0.0 | $6.0 | $0.0 | 0% |

| Gulf of Mexico | $0.1 | $0.1 | $1.2 | $0.0 | 0% |

| Total | $14.9 | $13.1 | $16.7 | $13.3 | 100% |

That further makes it challenging for small public companies.

“E&Ps of all sizes have proven to investors they can be profitable and pay dividends,” added Dittmar. “Now the key question is how long they can sustain profitable margins, determined by commodity prices which they can’t control and the quality of their drilling opportunities which they can control, at least to an extent.”

Inventory life is the substantial advantage large cap E&Ps have over smaller rivals, Dittmar said. Investors have recognized that by giving them a premium on their stock, he said.

“In turn, they can use that premium to buy more assets,” Dittmar said. “It is a market where the rich get richer.”

January M&A begins to thaw

After a slow start in January, E&Ps two megadeals were announced by mid-month.

Chesapeake Energy Corp. agreed to an initial sale of its Eagle Ford acreage for $1.425 billion — part of a larger divestiture of its assets in South Texas. In the Permian Basin, Matador Resources announced a bolt-on acquisition valued at $1.6 billion, excluding contingency payments.

Matador’s recent deal was, in part, a result of its status as SMID-cap with a higher share price than most of its peers. The company has also retained significant retained cash to make an acquisition.

Dittmar said Matador’s bolt-on acquisition of Advance Energy Partners Holdings LLC, an EnCap Investments portfolio company, appears to be a sensible bolt-on in the Delaware Basin core.

Matador was able to pay at multiples that were slightly accretive, Dittmar said, and add significant runway of high-quality locations that are immediately competitive in its portfolio for drilling capital.

“While not super cheap at about $25,000/acre, the deal prices in line with other recent M&A for core assets like Diamondback Energy’s buys in the Midland Basin in late-2022,” Dittmar said.

“Like some of the other recent buyers, it has also won the trust of investors with a successful track record on deals,” he said in Jan. 24 commentary.

Chesapeake Energy’s sale of its Brazos Valley assets to WildFire Energy I LLC advances its goal of being a pure gas producer focused on Appalachia and the Haynesville Shale, he continued.

Chesapeake’s hope is that the more specific focus raises its stock price, Dittmar said.

“The company is also unloading an asset that was no longer viewed as competitive in its portfolio, and the deal checks off one of Chesapeake’s widely telegraphed goals from last year,” he said.

Dittmar said the sales price at first glance looks “a bit underwhelming though, especially considering the company paid nearly $4 billion in the purchase of WildHorse Resource Development that brought these assets into its portfolio.”

The $1.425 billion purchase price also appears to be “a bit beneath the value of the production with no value attributed to the undrilled locations.”

The sales price likely reflects the limited buyer pool for this region of the Eagle Ford, and an overall challenging M&A market outside of the highest quality assets, Dittmar said.

“Chesapeake will likely continue to consider sales options for its remaining Eagle Ford assets, dependent on economic conditions and commodity prices,” he said.

Though the deal makes sense given Chesapeake’s goals, it is unlikely to kickstart any trend of public-to-private asset sales, Dittmar said.

“Most public companies will likely view the offers from private E&Ps as being insufficient to be worth giving up the cash flow from even non-core positions, and private companies are likely to stay conservative in their offers,” he said.

Recommended Reading

Dividends Declared in the Week of July 22

2024-07-25 - Second quarter earnings are underway, and companies are declaring dividends.

Endeavor Energy Founder Autry Stephens Dies at 86

2024-08-16 - Stephens created a legacy in the Permian Basin that Endeavor said will continue to shape the future of the company.

Viper Energy Offers 10MM Shares to Help Pay for Permian Basin Acquisition

2024-09-12 - Viper Energy Inc., a Diamondback Energy subsidiary, will use anticipated proceeds of up to $476 million to help fund a $1.1 billion Midland Basin deal.

Dividends Declared in the Week of July 15

2024-07-18 - Here is a selection of dividends declared in the week of July 15 for upstream, midstream and service and supply companies.

Dividends Declared Sept.16 through Sept. 26

2024-09-27 - Here is a compilation of dividends declared from select upstream, midstream and service and supply companies.

Comments

Add new comment

This conversation is moderated according to Hart Energy community rules. Please read the rules before joining the discussion. If you’re experiencing any technical problems, please contact our customer care team.