The Arkansas Western Gas Co. was founded in 1929 as a subsidiary of a larger Dallas gas player.

Fast forward 94 years, and the renamed Southwestern Energy Co., which was renowned for discovering the Fayetteville Shale natural gas play in Arkansas, is no longer even active in “The Natural State.”

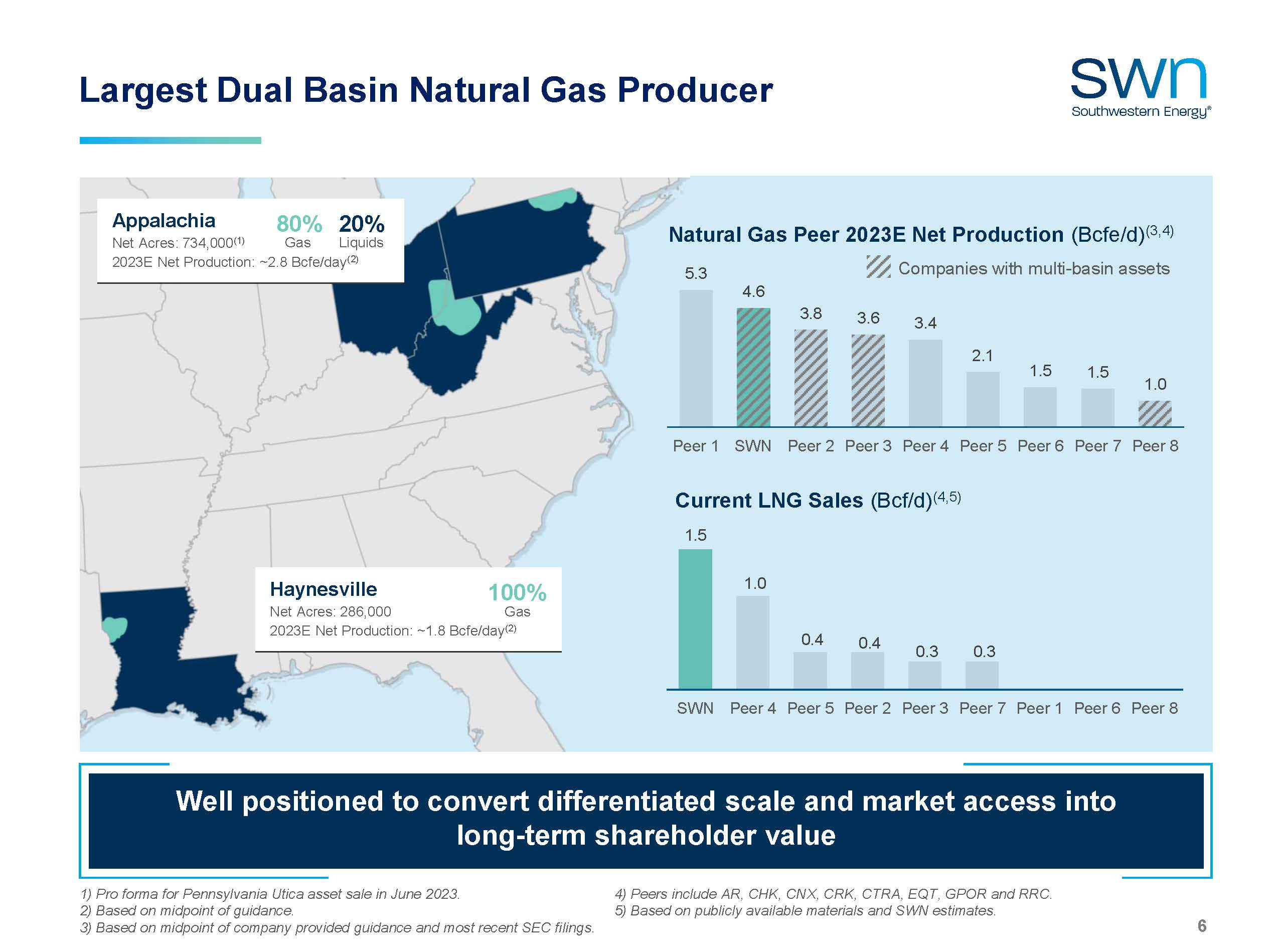

Instead, Southwestern last year transformed itself into the largest dual-basin gas producer in the country, focusing its attention on Appalachia and, most recently, the Haynesville shale gas plays with headquarters just north of Houston.

Southwestern, often pronounced in shorthand as “Swin” for the “SWN” stock ticker, aims to capitalize on the growing global LNG market now that it has established its Haynesville position and has the capacity to move its Appalachia gas to Louisiana via pipelines, and then to rapidly growing LNG hubs along the U.S. Gulf Coast.

In August, SWN reported second-quarter production of 4.65 Bcfe/d, down slightly from 4.81 Bcfe/d during the same time period last year. Likewise, profits fell from a whopping $1.2 billion in second-quarter 2022 to $231 million this year.

It’s a dramatic difference, but there were extenuating circumstances. Henry Hub spot prices for natural gas in August 2022 reached a sky-high average of $8.81/MMBtu; the price was hovering near $2.70/MMBtu in mid-August, according to the U.S. Energy Information Administration (EIA).

The bottom line is that SWN is keeping costs down, reducing activity slightly and remaining profitable while awaiting the next wave of global LNG demand as new U.S. export facilities come online and prices respond correspondingly.

Southwestern President and CEO Bill Way has overseen much of the recent transformation. A Houston native, Texas A&M University Aggie and the ninth of 12 children, Way made his bones working around the world with gas and LNG for ConocoPhillips and the BG Group before joining SWN in 2011 as the COO and taking over the CEO role in 2016.

SWN was growing a sizable Appalachia footprint during this time, having made big buys from Chesapeake Energy and others. But then the deal-making under Way took off.

First, in 2018, SWN sold its legacy Fayetteville position for nearly $2 billion, deciding to focus on the East Coast. And just as Southwestern was struggling with a stock price under $2 per share in 2019 and during the height of the pandemic in 2020, SWN bought bigger into the Appalachia with the purchase of Montage Resources for about $850 million.

Then the bolder and bigger, rapid-fire buys into the Haynesville unfolded in 2021 and 2022. First came Indigo Natural Resources for $2.7 billion and then, just five months later, GeoSouthern Energy’s GEP Haynesville for $1.85 billion. Quite abruptly, SWN was the largest Haynesville producer and the biggest dual-basin gas player.

With a rising market capitalization value above $7 billion as of mid-August, SWN holds more than four times the investment value it did from lows just prior to the pandemic.

Way sat down with Hart Energy to discuss the growth, challenges and the promising future.

Jordan Blum: You came from BG before it was acquired by Shell in 2015, so that turned out to be pretty good timing on a number of fronts, right?

Bill Way: When I was at BG, we bought half of Exco [Resources] so that we could learn how to do shale. So, I had an early entry into the Haynesville. Doing that at a major company is quite challenging because of the cost and the agility and the flexibility you need. But it was perfect having experienced that level of tension between a major global leader and ‘how do you get the economics and the margins to make shale work?’ And so it felt like a very natural fit to take what I had experienced at BG, where I had accountability for their shale development along with operations. Then I come here and keep us from growing into this cost-centered behemoth of a company like so many tried to do. You look back in the old days of shale, and the ability to drive margins up and costs down eluded a lot of large companies.

JB: Bigger picture, can you to talk about the transformation of Southwestern from a small Arkansas gas company so long ago to unlocking the Fayetteville Shale to no longer being in the Fayetteville, but having all this big Appalachia and Haynesville footprint now?

BW: The genesis of that came from better understanding margins. In the commodity business, margin is everything. Cost management is important, and you’ve got to invest in the properties that you own, or you have to ask yourself, why do you have them? I come here and am a part of the discussion of shifting our investment from Fayetteville, which we discovered. We had drilled thousands of wells. We had quite a mature business on our hands, and the economics for the Northeast were significantly ahead of the Fayetteville economics. So, we made a case for change and went to the board [of directors] and got approval to basically exit the Fayetteville, the foundational asset of the modern company, and to shift that capital to Appalachia and begin to accelerate the growth.

So, we began expanding our [Appalachia] footprint both from acquisitions of land all the way through drilling and completions and growing that spot.

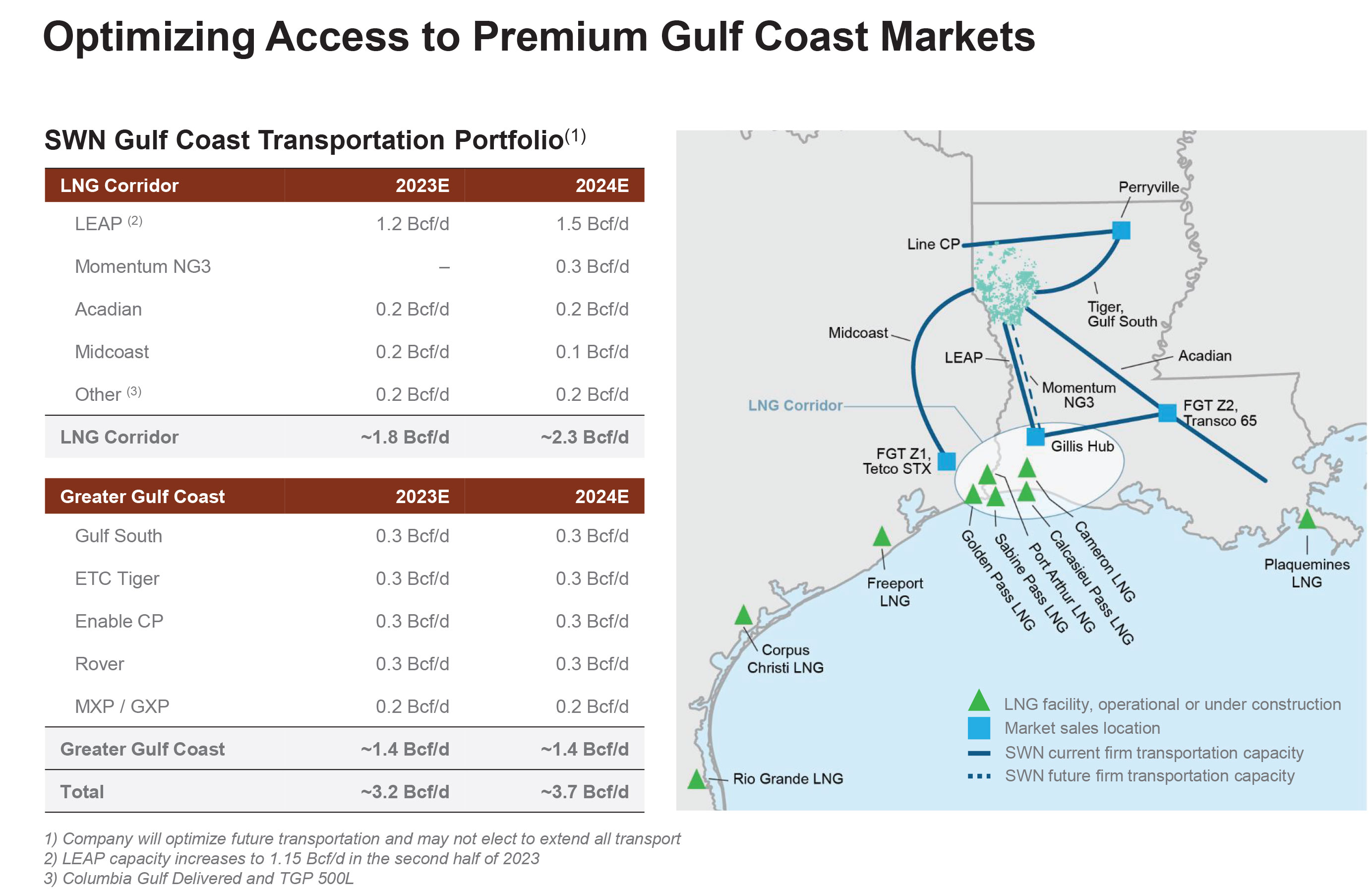

Now, in the Haynesville we have a core mandate, which is, you will have firm transportation from field to market of choice, or you will not acquire, or you’ll not develop a major piece of the business. Doing that enabled us to assure ourselves that we’re going to get the returns that we wanted because of the gas reaching the market.

Part of this was the pre-2019-2020 era of low share price, low gas price, COVID and all these other things that were going on. We examined our state of play, and while we had grown in the Appalachia to a degree, we were unable to continue to grow at the rate that one needs to build the scale to differentiate yourself in the pack. And so, during all of the things that were going on with COVID and everything else, we shifted our focus on how we build a growth strategy, and what do we want that to look like.

We had been a dual-basin supplier when we had Fayetteville and Appalachia. So, that wasn’t an issue for us. It was a question by a number of investors: Are you sure you want to go through a dual-basin kind of thing? And we said, ‘Well, we’re a gas company first and always, and if we’re a leading gas company, we ought to be in the two leading basins in the country.’ And so it was natural and logical for us to make that shift.

We picked the most prolific, the highest-return companies that we wanted, and we went after them in a very disciplined, very focused, very methodical way, so that we were making the right choice at the right time with the right economics. The process was transparent enough that our board could opine and approve, and our shareholders could vote for it, and they understood how we put it all together. Our entry into the Haynesville then jettisoned us from a meaty or robust player in Appalachia into a dual-basin, significantly larger enterprise with cost economies and access to markets we didn’t have. We’re the largest supplier of natural gas to the LNG sector today in the U.S.

JB: Are you looking now at doing more direct LNG contracts?

BW: As we look forward in time and study whether we’re going to be in the international LNG price market or whatever, we have a deep understanding from inside, and we’re spending time with current companies, including some of the major ones we supply, to learn more and more about the market should we choose to get in.

We don’t feel pressured. We have plenty of time, and we have plenty of volume and reserves co-located, so we’re advantaged—no matter what—when we get there. We have the ability to now get Appalachian gas to Louisiana, and Louisiana gas to the Gillis Hub, which was set in place and signed agreements before we closed.

We’re, as a company, right there with existing contracts in hand. They’re all Henry Hub-based for now. But, if we’re going to do internationally priced [contracts], it’s probably to some of the people that we’re already supplying.

JB: So, it seems like there’s an interest there?

BW: There’s interest there. We have an interest in understanding it. We would never build an LNG global price business off of a pricing peak. So, it’s getting past that and understanding what the real market looks like.

JB: Despite the lower gas prices now, you seem quite bullish overall?

BW: I do, and the reason I believe that is LNG is the defining moment for the gas supply industry in this country. The bulk of the facilities are all on the Gulf Coast in two of the friendliest states to our industry. So, we have all of that production. The interstate pipelines to bring our Appalachia gas down to the Gulf Coast, they’re already built. So we have assured flow from production to the market of choice for us.

We want a business that can generate free cash flow sustainably and get this debt down, and we see a path to get there as LNG picks up. The strategy made logical sense to us as long as we weren’t just trying to grow for the sake of growth. We’re excited about how we position the company when the real ramp of LNG occurs.

One of the things we needed to do was to educate our investors more deeply in the Haynesville. It’s LNG and it’s the technology advancements that have occurred over the years that have enabled us there. We’re in the hottest, highest pressure area in the basin, and we can drill and complete wells at a reasonable, but not reasonable enough, cost. We’re continuing to drive that down. It represents a significant opportunity to supply because we can repeat, highly repeat it to supply these very large numbers for LNG. In the very near term, I think this will continue to accelerate.

JB: Would you take me behind the scenes? How tricky was it to line up those back-to-back Haynesville deals with Indigo and GeoSouthern, not just timing wise, but in the heart of the pandemic as well?

BW: I’ll back up a little bit. During the heart of the pandemic, … we were also coming out of or right at the very lowest share price we had in a long time. But all of that was, quite frankly, really dwarfed by the loss of our CFO right in the middle of COVID and the acquisitions. Julian Bott’s passing [in January 2021] was very, very difficult on the team and very difficult on me. He’s a dear, dear friend. But it was a really, really strong testament to the leadership team. We couldn’t go and pay respects because of COVID, but we managed through it. We dug in and, in his honor and his spirit, we drove through low gas prices, low share price. We shifted and focused our strategy a bit more around making sure that we were controlling what we could control.

Thank goodness we had done Montage first. The Montage acquisition built credibility on how we do acquisitions with the discipline and the rigor. We jettisoned the parts of those acquisitions that we didn’t want right up front, so we never had to touch them. And it gave the board confidence, after they went through their analysis, to support the acquisitions.

I think the root of these two acquisitions began with relationships. I got to know [Indigo founder and Chair] Bill [Pritchard] very well, and I got to know [GeoSouthern President and CEO] Meg [Molleston] very well. We spent time with their entire teams and our entire teams, making sure that they knew who we were and what we stood for, and how we were going to go about it. I can tell you, in both cases, that their view of those pieces of the puzzle were instrumental in helping us win those. We weren’t in a competitive process, but there were competitors all around us. And we knew they were sitting there waiting to interlope if they could.

Meg is still one of our major shareholders today. And we worked through each piece. We understood the integrity of the data, and we understood what fair price would be. We have our own drilling rigs and frac fleets, so we could bring employees to Louisiana to learn from the same way they learned in Appalachia from Fayetteville, and learn deeply so that we could begin to drill these wells and have the performance that we built into the models and expected. And that happened.

JB: You touched on how tough things were in the pandemic, but 2019 was a really difficult, tough year too. Can you compare and contrast just how and why things were so tough pre-pandemic, and how things have transformed since then?

BW: I think that certainly gas markets have a role to play. It’s the effectiveness of your hedging program or whether you have a [cold] winter or not. LNG’s big demand pool hadn’t happened yet in a material way. So, what do you do to deal with that?

Well, we amped up our hedging program. We understood the importance of not overdoing it, but certainly providing that base of support for the business.

The fact that we kept driving forward on the acquisitions was critically important. We needed the scale; we needed to be able to manage the costs and grow the margins by owning those businesses. We were just undeterred. We spent a lot of time with our board helping them understand what we were trying to do. They understood from the days of exiting the Fayetteville that the advantages of well-executed scale increases would come to the company. We really never paused to say, ‘Is this the right thing?’ If you’re going to be a serious gas champion, you’ve got to have scale and why not have complimentary basins where you have incredible flexibility and agility built into your company.

And we’re now focusing on debt reduction. When we set out last year and this year, our capital allocation strategy is focused primarily on debt reduction. Whether there’s high gas price[s] or low gas price[s], carrying this level of debt is not competitive. We got a lot of questions about returning the money to the shareholders. And, we changed their minds, and they came back solidly in support of maintenance-capital level investment to keep production relatively flat. All of the available free cash flow after that goes to pay down debt. We’ve done one or two noncore small deals, and last year we paid down $1 billion of debt.

JB: On the macro side of things, can you elaborate on how gas has transformed from more of a domestic product to the growing global LNG demand with exports and all of the geopolitical conflicts?

BW: The advent of the shale boom showed the industry and the world that we had the depth of inventory and reserves to be able to participate from a supply standpoint in the growing LNG demand in the world. And you began to see the shift of massive growth in that sector that was going to really kind of reset demand.

I think the U.S. is the supplier of choice from a security of supply political position. In a very fast-growing LNG market, you’re expecting significant growth overseas. There’s a supply-demand gap. In Australia, they’re struggling with domestic gas, and Qatar and a number of other countries [have issues]. Then you have the U.S., that has ample reserves, ample ability in building these facilities.

The U.S. supply over the next several years will tend to outpace local demand. Having an outlet for that gas supply as LNG brings economics back to fields, brings economics back to companies. And it’s sort of a symbiotic relationship because the LNG industry needs the U.S. reserves, and the U.S. production companies need a ready market that is bigger than here. So, thus, you have additional LNG facilities ready to be sanctioned and started up over the next handful of years.

JB: With lower gas prices now impacting drilling and completions and maintenance-level capex, is it tough scaling back a little bit?

BW: To ensure this year that we invested within cash flow, we put together a program in the beginning of the year that would adjust downward if prices fell further. For us, we added, ‘what else can we do to generate cash flow?’ And it was an all-out assault on inflation. So, we were able to cut capital costs materially and not cut production because the unit cost to do things had come back down. We’re looking at a 5% to 10% inflation impact going forward instead of 15% to 20%.

The other piece is what we call the productive capacity of the company. Think of a flywheel and you have an investment decline, which will slow your flywheel down and maybe make it go backwards if it’s a big enough decline. We did that in 2016, the day after I became CEO, in a pretty big leadership moment. We said we’re going to tell the industry we’re going to stop. The problems of then don’t exist today, but the impact was a great learning opportunity. When we stopped, the flywheel started turning backwards and it took $500 million of investment to arrest the backwards and get it going back forward. What’s the big deal about that? Well we believe in a constructive view of the gas markets going forward. There’s going to have to be a price that will incentivize, at some point in the future, drilling and completion of wells to fill all of this LNG demand. Call it the 2024, ’25, ’26 time period.

We’ll watch that because better economics from higher prices also can mean paying down debt faster. If it works out the way we hope, you can end up with higher prices in the near term that can provide additional cash flow. Then, the ability to quickly ramp up–remember we own seven of the rigs that we actually use–we can move them at will, start them up, stop them at will. And so our spot time can be quite, quite quick. We estimate probably a $4/MMBtu gas price to incent enough activity to get the supply needed.

JB: So a lot of the plan now is positioning to be able to flip that switch quickly?

BW: I would call it that. We’ll have a little decline this year, and we do not plan on growing production next year. I think the fact that we’ve gotten inflation out and gotten more effective, we can lower our previously projected capital and not cut activity so much that we’re in the reverse flywheel kind of thing, which means we can come back fairly quickly.

JB: In the meantime, you haven’t scaled back much in the Haynesville, but you’re leaning a bit more on the liquids portions of the Appalachia, right?

BW: In the beginning of the year, we put an extra rig in our NGL-laden gas in West Virginia, and we’ve kept that there. Our overall allocation, 55:45, still favors Haynesville. But since we’ve owned Haynesville, everywhere we own, we’re doing some level of drilling, whether it’s Ohio or Pennsylvania or West Virginia. A well in Pennsylvania is a lot cheaper because you can drill 24,000-foot horizontals that are 6,000 feet deep. So, you’re talking about a 30,000-foot well. And we can do those highly repeatable to drive cost out. You can’t do that in Haynesville. It’s too high pressure, high temperature, even the units are not that long. But there are other ways to optimize. Haynesville is advantaged with very, very low differentials because you’re right there in the marketplace.

JB: Does the LNG focus play a big role in SWN’s investments in RSG (responsibly sourced gas) and methane emissions to satiate potential global buyers?

BW: I think that those are enablers. I’ve changed my view on this, and it’s probably based off of being deeply involved in understanding around our culture here. We focused on the components of ESG as core values that support our culture before that ESG acronym was cool. We built and designed our modern company to reflect the tenets of an RSG requirement. We use Project Canary for 100% certified gas, and we will be 100% monitored. We are the only producer in the country that replaces all the freshwater that we use. That’s, for us, a social aspect, not even environmental. We’ve basically put 16 billion gallons of freshwater back into the aquifers where we’ve removed them. We have low methane intensity, and we have GHG goals and 50% reduction targets.

My point is that we’ve been doing all of this because that’s how we operate and because it is the right thing to do.

Recommended Reading

Industry Consolidation Reshapes List of Top 100 Private Producers in the Lower 48

2024-06-24 - Public-private M&A brings new players to top slots in private operators list.

Beetaloo Juice: US Shale Explores Down Under

2024-06-28 - Tamboran Resources has put together the largest shale-gas leasehold in Australia’s Beetaloo Basin, with plans for a 1.5+ Bcf/d play. Behind its move now to manufacturing mode are American geologists and E&P-builders, a longtime Australian wildcatter, a U.S. shale-rig operator and a U.S. shale pressure-pumper.

Private Equity Looks for Minerals Exit

2024-07-26 - Private equity firms have become adroit at finding the best mineral and royalties acreage; the trick is to get public markets to pay more attention.

Baytex Energy Joins Eagle Ford Shale’s Refrac Rally

2024-07-26 - Canadian operator Baytex Energy joins a growing number of E&Ps touting refrac projects in the Eagle Ford Shale.

EOG Resources Wildcatting Pearsall in Western Eagle Ford Stepout

2024-07-17 - EOG Resources spud the well June 25 in Burns Ranch with rights to the Pearsall well about 4,000 ft below the Eagle Ford, according to myriad sources.