(Source: Shutterstock.com)

A confluence of world events is depleting natural gas inventories, raising commodities prices and U.S. exports to record levels that will likely continue to grow throughout the rest of the year, according to analysts at the Federal Reserve Bank of Dallas.

And that could make the U.S. midstream industry a key beneficiary of the tumult.

Diminished general inventory and the geopolitical impact of Russia’s invasion of Ukraine are driving the commodity’s sharp rise in prices both global and domestic. In Europe, natural gas is trading at more than $30 per MMBtu in response to Russia’s aggression. Elsewhere, buyers chased the benchmark Japan–Korea marker for LNG to average $29 in April, the Dallas Fed said.

The soaring global extremes, coupled with limited U.S. production growth—a corporate response to activist shareholders—and strong domestic demand took Henry Hub to $6.60 in April.

This U.S. benchmark traded between $7 and $8 during the first half of May—more than double the average nominal price level for the trailing 10 years, but still a lagging amount relative to prices in Europe and Asia.

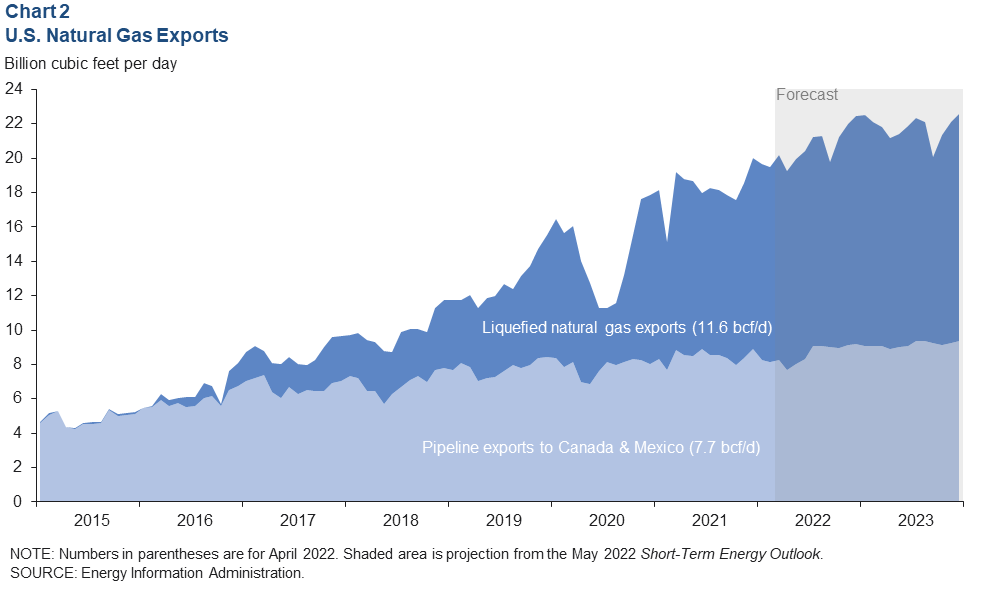

Moreover, Dallas Fed analysts forecast that U.S. exports of LNG, counted at 11.6 Bcf/d in April 2022, will continue to grow throughout the year before leveling off at 13.4 Bcf/d by year-end where volumes will hold until additional capacity comes online in 2024.

LNG pipeline capacity to Mexico is also projected to increase, taking total U.S. pipeline exports from 7.7 Bcf/d to 9.2 Bcf/d.

All told, the projected combination of 22.5 Bcf/d of gas exports in December 2022 will account for 21% of U.S. marketed natural gas production, a 3% increase from the same period last year, according to the U.S. Energy Information Administration.

Europe Minds the U.S. Midstream

Europe is now much more inclined to enter into long-term take or pay LNG contracts with U.S. exporters, suggesting long-term U.S. gains, said independent LNG consultant Guy Broggi during a Wells Fargo presentation on global LNG dynamics on June 7.

Moreover, he said, it will take years before Europe will manage to forego Russian gas, leaving several countries in Europe—especially Germany—at-risk in the event of a Russian effort to cut supply during the winter.

“U.S. LNG exporters directly benefit from Europe's long-term transition away from Russian gas,” said Well Fargo analyst Michael Blum.

Both Cheniere Energy and Energy Transfer in the U.S. have significant liquefaction capacity exposure. Broggi suggested Europe will be significantly more willing to sign long-term LNG contracts now than before the invasion of Ukraine.

“This bodes well for [Energy Transfer] to secure sufficient contracts to FID Lake Charles and for Cheniere (LNG) to supports expansions beyond Corpus Christi stage 3,” Blum said.

“Several midstream companies have gas pipelines that can be expanded at attractive economics to support the gas supply needs of new LNG export projects.”

In sum, it’s a sellers’ market and substantial expansion is needed to keep the gas flowing, said Wells Fargo’s Roger Read.

“This appears to have created and may sustain a multi-year global supply deficit of LNG deep into the 2020s. Through the middle of the decade, North America and the Middle East (Qatar) will likely lead the supply expansion while Europe and East and South Asia remain the biggest sources of demand,” Read said. “Term contracts appear likely to remain a core component of global LNG market.”

Recommended Reading

Kimmeridge’s Mark Viviano on Reshaping the Energy Sector, SilverBow-Crescent Deal

2024-05-16 - Kimmeridge Energy Engagement Partners’ Mark Viviano says the company is evaluating the Crescent Energy and SilverBow Acquisition and how Kimmeridge played a key role in transforming the shale sector in this Hart Energy Exclusive interview.

SUPER DUG: Shale 4.0 Era about Building Scale- Rystad

2024-05-16 - The Shale 3.0 era or capital discipline era will be followed by the Shale 4.0 era, which will see companies focused on building scale, according to Rystad Energy Senior Shale Analyst Matthew Bernstein.

Adkins: Attacks on Fossil Fuels, Overregulation Poised to Backfire

2024-05-17 - Raymond James’ J. Marshall Adkins tells Hart Energy’s SUPER DUG conference attendees demonizing oil and gas, strenuous regulations and continued inflation are bound to have unexpected consequences for E&P opponents.

AI Highs: Corva Predictive Drilling Powers Oilfield Efficiency

2024-05-20 - The energy sector is buzzing with talk of artificial intelligence, and Corva is capitalizing on its ability to synthesize complex data to optimize drilling operations with predictive drilling software.