Independence Contract Drilling Rig 211 shares surface acreage in the Permian with a West Texas yucca. (Source: Hart Energy)

It’s hard to shine a spotlight on the constantly evolving Permian Basin, but new analysis illustrates the outsized influence the massive, stacked play has had on A&D in 2016, Evaluate Energy said Oct. 26.

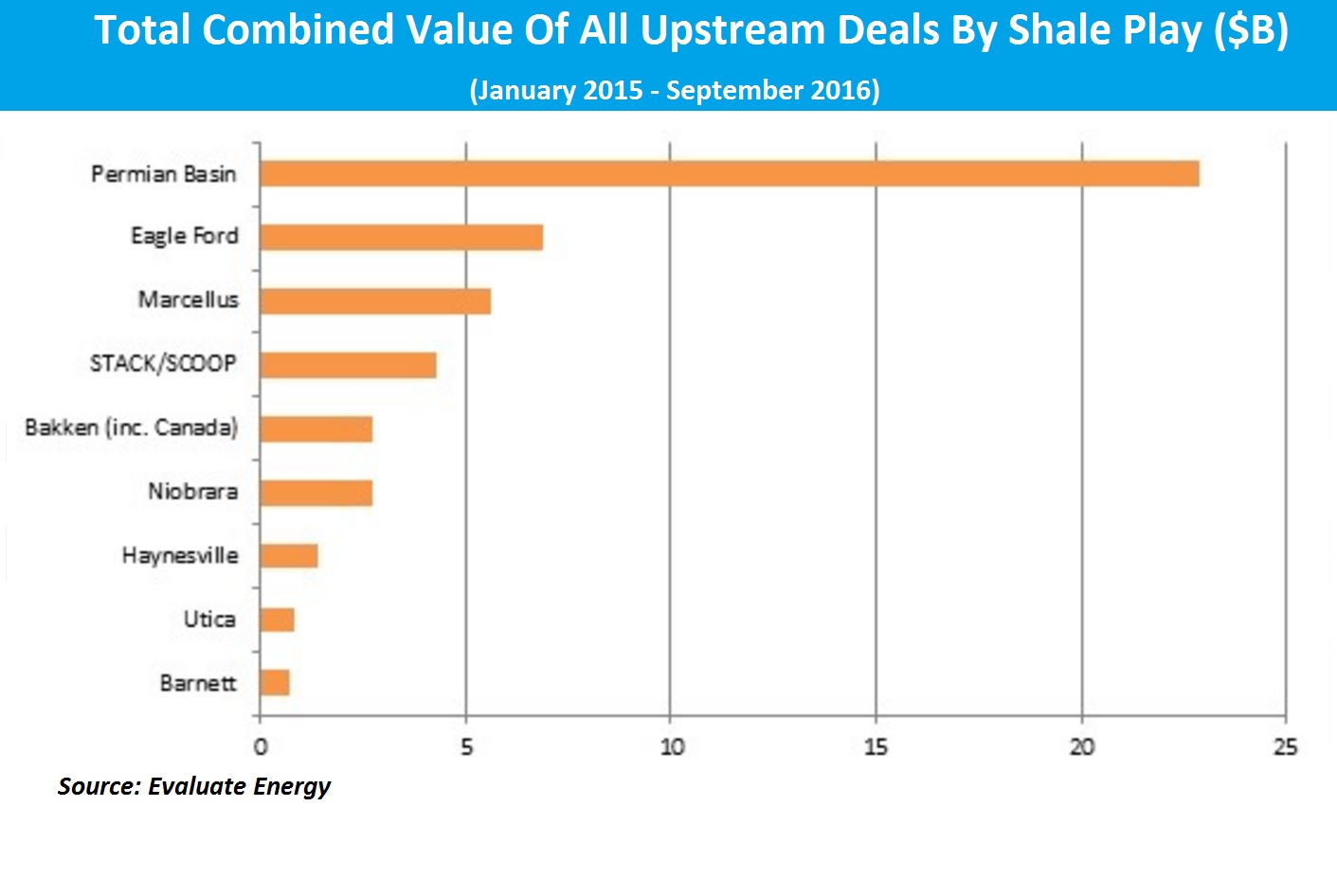

Permian M&A transactions have reached nearly $23 billion over the past 21 months—about $16 billion more than its nearest rival, according to Evaluate Energy data. Out of all upstream deals worldwide in the third quarter, 33% focused upon the Permian Basin alone.

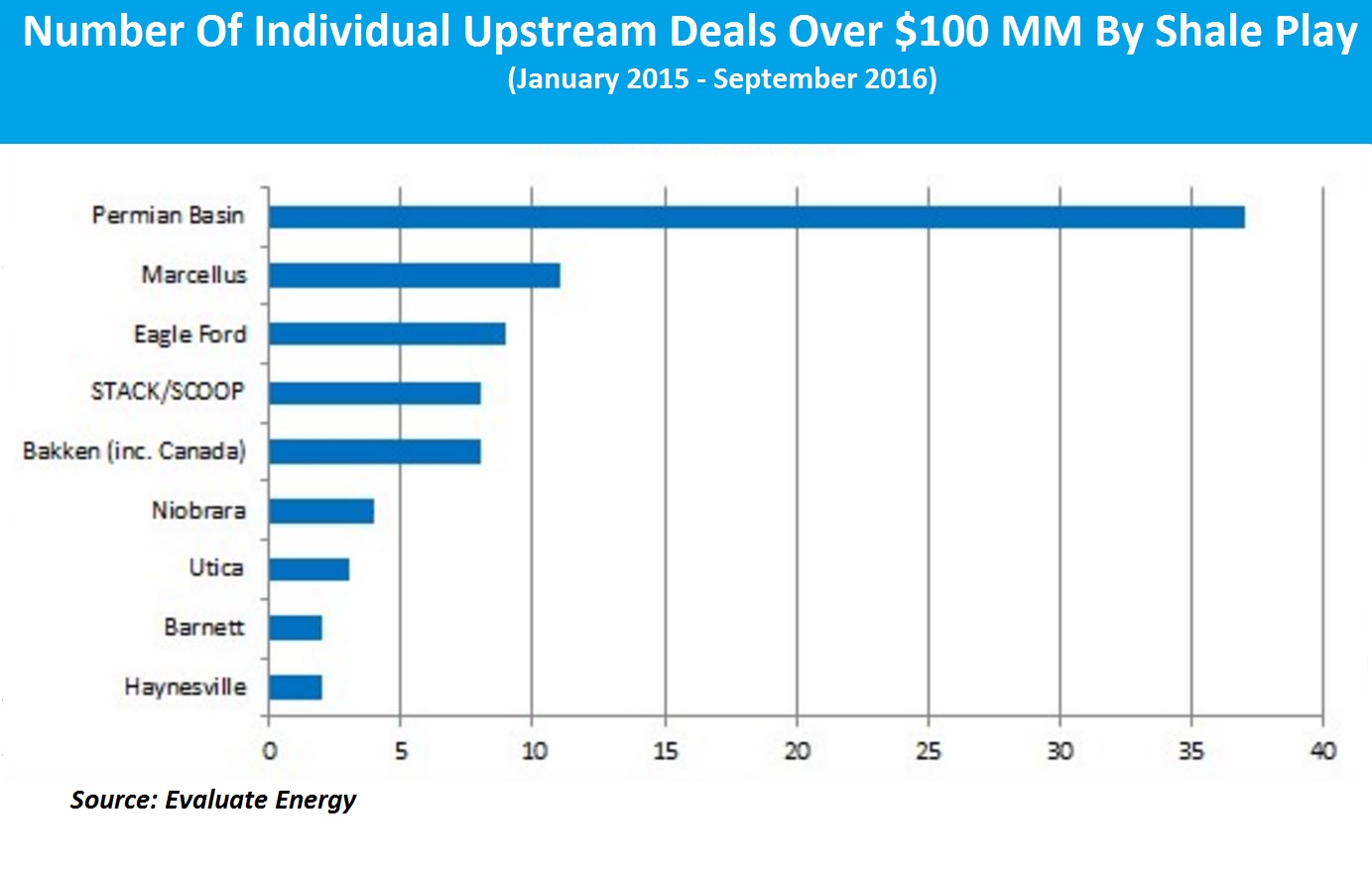

And this conclusion is not because of one megadeal—a transaction of at least $1 billion—skewing Evaluate Energy’s data. In 21 months, 37 deals each had values of at least $100 million, demonstrating higher levels of confidence in the Permian as a long-term investment option over other U.S. onshore producing regions.

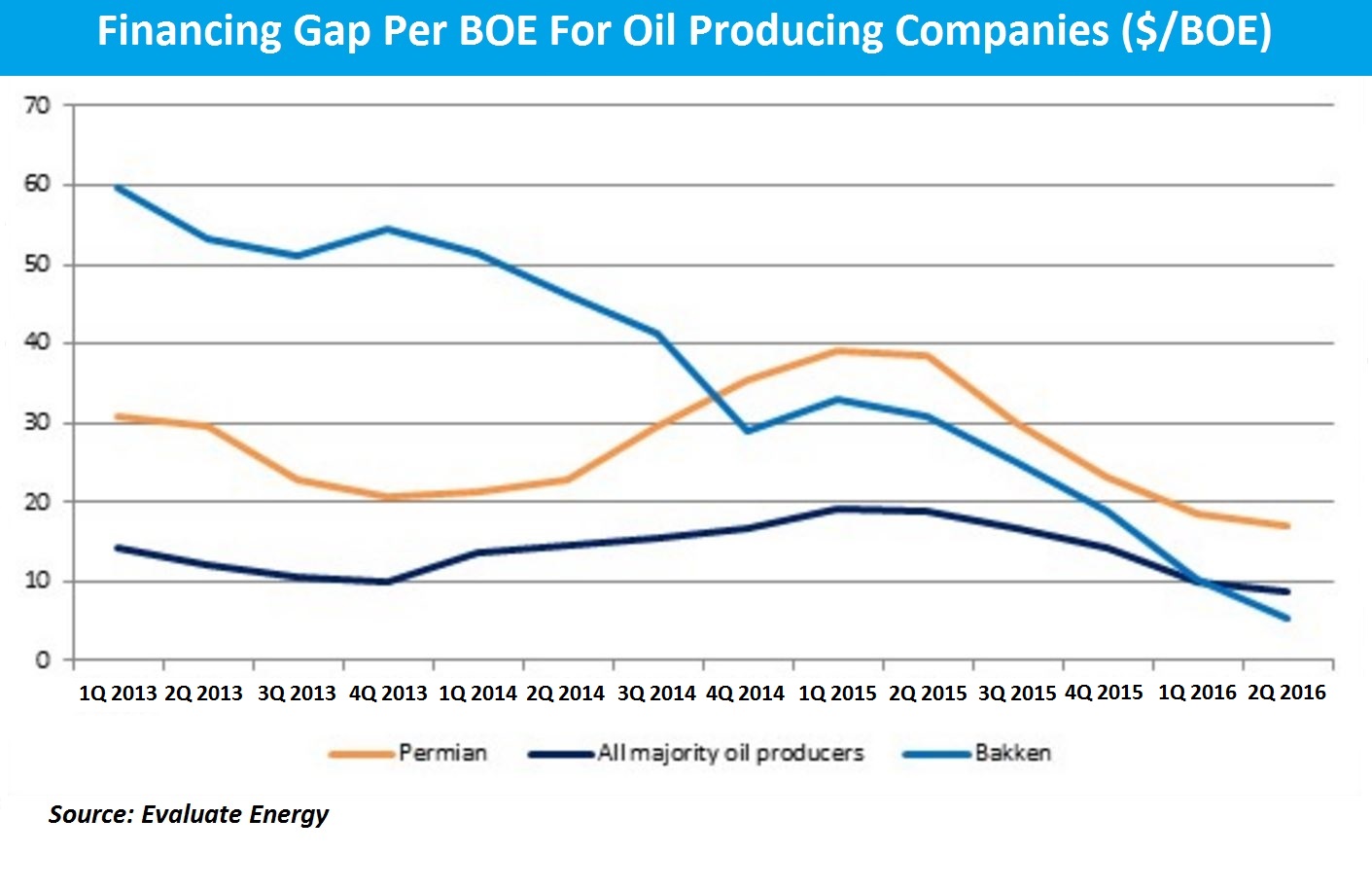

The confidence in the Permian compared to other oil-heavy regions—and the Bakken in particular—is not only illustrated in M&A activity, but also in how much companies are currently willing to invest in their own future.

In second-quarter 2016, the internal financing gap—the difference between capex and operating cash flow—was far greater for the Permian than all other oil-producing U.S. regions Evaluate Energy examined in its latest study.

Permian companies recorded an average financing gap per barrel of oil equivalent (boe) of $17/boe in the second quarter, the highest regional average in the U.S. This used to be how Evaluate Energy would describe the Bakken, but that picture has changed dramatically since commodity prices crashed.

In the second quarter, Bakken companies recorded a financing gap per boe of only $5/boe.

The large financing gap in the Permian is driven primarily by extremely robust capex spends. For, while total spending has fallen in the Permian over time, it has done so at a dramatically slower rate than other U.S. oil producing areas. This reveals how confident the operators must be feeling, Evaluate Energy said.

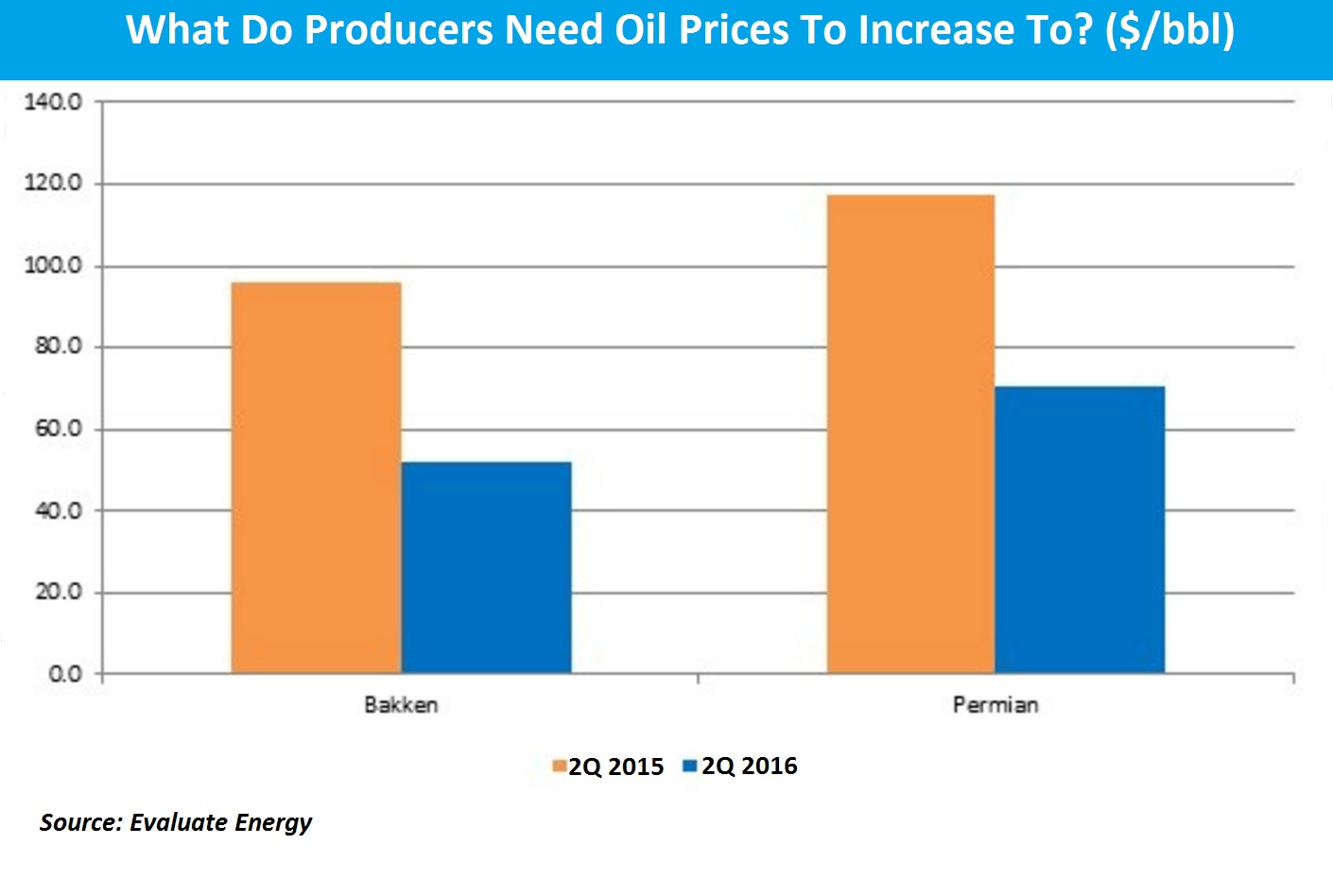

To reinforce this narrative, in Evaluate Energy used current financing gaps to calculate what oil producers across the country needed the benchmark WTI price to be in order to cover the entirety of their capex spends using only operating cash flow.

In the case of the Permian, the companies would need a $71 West Texas Intermediate (WTI) price to do this in second-quarter 2016. For the Bakken, that price is only $52. In the second quarter, WTI only averaged $44.86.

This figure should not be considered a breakeven number, not least because capex spending is optional, for the most part. Rather, it’s a barometer of operators’ confidence in their own long-term prospects.

Clearly, capex plans are lower and less bullish than a year before, as low prices continued to bite. But Permian operators are undoubtedly still displaying a greater level of confidence in being able to fund robust capex spends than their rivals.

This article was submitted by Evaluate Energy.

Recommended Reading

Analyst Questions Kimmeridge’s Character, Ben Dell Responds

2024-05-02 - The analyst said that “they don’t seem to be particularly good actors.” Ben Dell, Kimmeridge Energy Partners managing partner, told Hart Energy that “our reputation is unparalleled.”

Marketed: Delta Minerals Non-producing Sale in Colorado

2024-05-02 - Delta Minerals LLC has retained EnergyNet for the sale of non-producing minerals in Bent, Cheyenne and Kiowa counties, Colorado.

Phillips 66 Weighs Divestments, Targets Renewable Fuel Increase

2024-05-02 - Phillips 66 looks to boost renewable fuels production by 67% through the end of the second quarter 2024 at its Rodeo complex in San Francisco while weighing a potential divestiture of its retail marketing businesses in Austria and Germany.

Chouest Acquires ROV Company ROVOP to Expand Subsea Capabilities

2024-05-02 - With the acquisition of ROVOP, Chouest will have a fleet of more than 100 ROVs.

Chesapeake Stockpiles DUCs as Doubts Creep in Over Southwestern Deal

2024-05-02 - Chesapeake Energy is stockpiling DUCs until demand returns through growth from LNG exports, power generation and industrial activity.