Pierce Norton, president and CEO of ONEOK Inc., speaking during CERAWeek by S&P Global on March 20, 2024. (Source: CERAWeek by S&P Global)

After closing an $18.8 billion acquisition of Magellan Midstream Partners, ONEOK is eyeing ways to expand its takeaway capacity from the prolific Permian Basin.

Tulsa-based ONEOK Inc. already had a large portfolio of midstream assets for NGL and natural gas gathering and processing before acquiring Magellan Midstream Partners LP.

The Magellan acquisition gave ONEOK much greater scale in refined products, ONEOK President and CEO Pierce Norton told Hart Energy in an exclusive interview.

“Magellan has probably the premier refined products system in anywhere in the United States,” Norton said.

Magellan had access to nearly 50% of the nation’s refining capacity with its refined products system.

The Magellan acquisition also delivered exposure into a new market for ONEOK: crude oil pipelines.

Magellan owned interests in approximately 2,200 miles of crude pipelines—1,000 miles of crude pipe, a condensate splitter and 31 MMbbl of storage capacity was directly owned by the partnership.

“Crude was new to us—but that’s something we can enhance,” Norton said. “We are in the pipeline business. We move products, and crude is no different.”

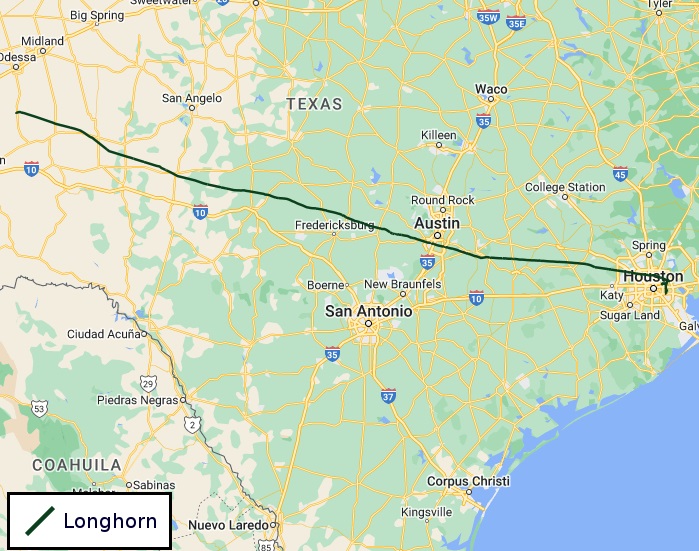

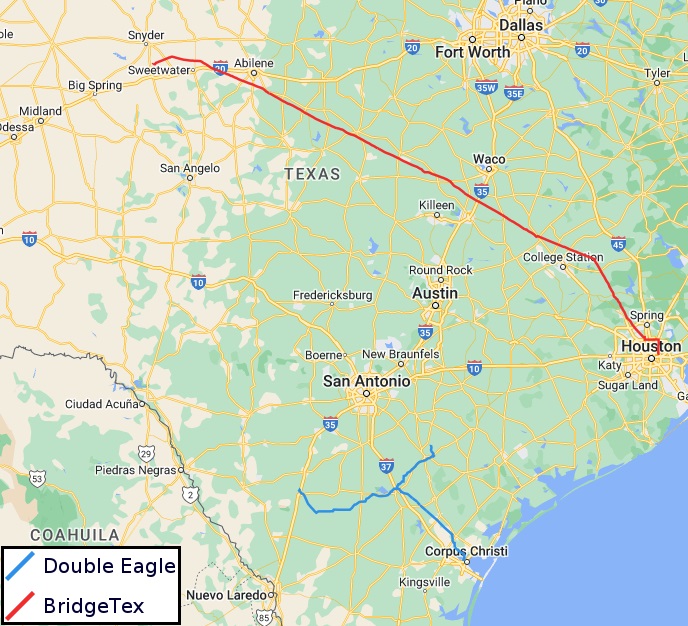

ONEOK now owns the 450-mile Longhorn pipeline, which transports around 275,000 bbl/d of crude oil from the Permian Basin to storage facilities and refining operations in Houston.

Magellan held a 30% interest in the BridgeTex pipeline, a joint venture with affiliates of Plains All American Pipeline LP and OMERS Infrastructure Management.

The 400-mile BridgeTex pipeline can carry 440,000 bbl/d of Permian crude to Magellan’s massive East Houston storage terminal.

Magellan also held a 50% interest in the Double Eagle system, a 200-mile pipeline transporting Eagle Ford crude condensate from South Texas to storage and refining markets around Corpus Christi, Texas.

Magellan’s crude pipelines are still quite new for ONEOK, but the company is evaluating ways to deepen its footprint in transporting Permian oil.

Norton is keeping an eye on drilling efficiencies employed by E&Ps in the Permian, the Williston Basin and other oil basins—where operators are using fewer rigs to drill longer-lateral wells deep underground.

It’s a story ONEOK has watched play out in the North Dakota Bakken Shale, where the company has a legacy portfolio of gathering and processing and NGL assets.

Around 7% of the wells drilled in ONEOK’s Bakken territory had three-mile horizontal laterals in 2022, Norton said. That figure jumped to 13% in 2023, and ONEOK is projecting for 30% of all Bakken wells drilled this year to have three-mile laterals.

“You can actually have less drilling rigs but end up drilling the same or more lateral feet,” he said. “That access is more volume, although you’ve got less rigs.”

That trend is also being replicated in the Permian Basin—the top oil-producing region in the U.S.—and is starting to hit oilfield service players.

And a more-production-with-less-drilling strategy could have implications for future crude takeaway capacity growth for midstream players in the Permian.

“I do think [crude is] going to continue to grow,” Norton said, “but it looks like there’s enough crude oil capacity right now to move the crude that’s out there and even into the near future.”

RELATED

Analysts: Permian Basin Rigs Plummeted on Record Upstream M&A

Fractionation station

Where ONEOK aims to move the needle today is on NGL takeaway capacity—from the Permian and other geographies.

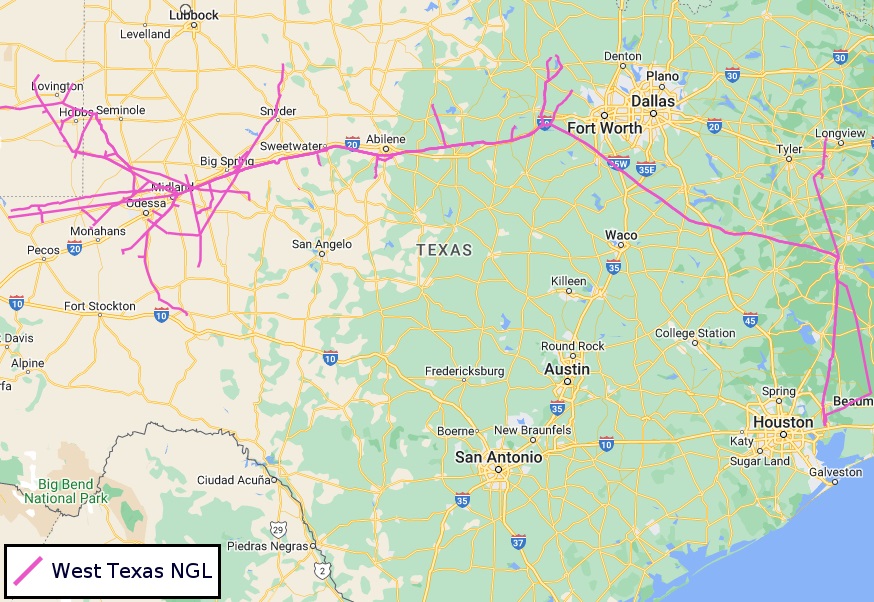

ONEOK is currently working to complete the looping of its West Texas NGL pipeline, a move that will more than double NGL takeaway out of the Permian.

ONEOK originally purchased the West Texas NGL pipeline system from Chevron affiliaes for $800 million in 2014.

The full loop is expected to be in service in the first quarter of 2025.

“That gives us a huge competitive advantage to pick up the next basically 400,000 bbl/d of NGL that’s coming out of the Permian,” Norton said.

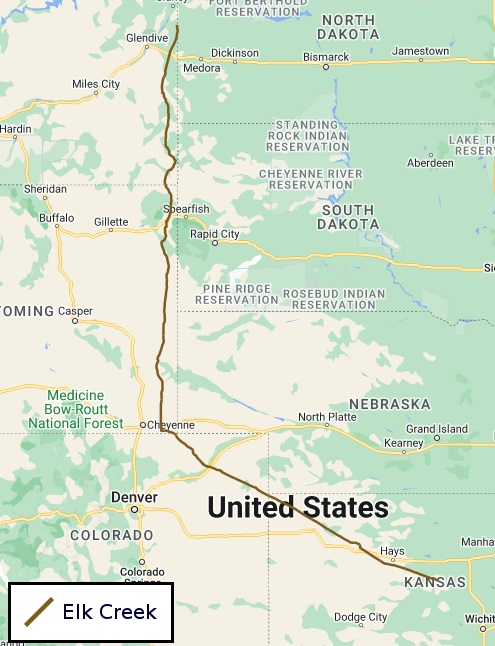

ONEOK is also growing its NGL footprint outside of the Permian. The company started initial work to expand its Elk Creek pipeline to 435,000 bbl/d to carry growing NGL volumes in the Rocky Mountain region.

The Elk Creek pipeline carries unfractionated NGL from ONEOK’s terminal in eastern Montana through liquids-rich regions of Wyoming and Colorado and into existing Midcontinent NGL facilities in Bushton, Kansas.

In addition to expanding its NGL transport capacity, ONEOK is spending around $550 million to construct a new 125,000-bbl/d NGL fractionator in Mont Belvieu, Texas.

RELATED

As ONEOK Digests Magellan, Sets Stage for More NGL Growth in 2024

Midstream M&A

The U.S. upstream sector has been consolidating at a red-hot pace, with some of the industry’s biggest and oldest names getting plucked off the playing board in a matter of months.

The lion’s share of the dealmaking deluge has fallen over the Permian, where cheap-to-drill acreage is trading hands for healthy premiums.

The biggest example is Exxon Mobil’s $64.5 billion acquisition of Pioneer Natural Resources, a deal that will reshape the future of the Permian’s Midland Basin.

Two other major Midland producers were also recently snapped up: Endeavor Energy Resources was taken out by Diamondback Energy for $26 billion, and CrownRock LP was carved out by Occidental Petroleum for $12 billion.

But midstream players are also jockeying for scale and combining alongside the rapidly combining upstream space.

ONEOK’s acquisition of Magellan was one example, albeit a big example, of midstream consolidation seen last year.

“The mantra of that deal was both companies could do more together than they could do apart,” Norton said.

Earlier this month, Appalachian gas giant EQT Corp. inked a $5.5 all-stock acquisition of Equitrans Midstream, which owns Mountain Valley Pipeline (MVP).

In January, Sunoco LP acquired liquids terminal and pipeline operator NuStar Energy LP for approximately $7.3 billion in shares.

Summit Midstream is selling its Utica Shale assets to an MPLX subsidiary for $625 million in cash—the culmination of a strategic review process undertaken by the Summit board of directors.

And Occidental is reportedly exploring selling interests in Western Midstream Partners, a pipeline operator with a market valuation around $20 billion.

Scale matters in the midstream space, just as it does in the upstream space, Norton said. But you don’t get bigger just for the sake of being big.

“But if that scale actually helps you—with your credit rating, or something like that—then that’s meaningful,” Norton said.

RELATED

Report: Occidental Eyes Sale of Western Midstream to Reduce Debt

Recommended Reading

Petrobras to Add Two FPSOs Offshore Brazil in Second-half 2024

2024-08-12 - Petrobras will bring online 280,000 bbl/d of production capacity in the second-half 2024 with the addition of two FPSOs offshore Brazil.

OPEC Gets Updated Plans From Iraq, Kazakhstan on Overproduction Compensation

2024-08-22 - OPEC and other producers including Russia, known as OPEC+, have implemented a series of output cuts since late 2022 to support the market.

EOG Testing 700-ft Spacing in Ohio’s Utica Oil Window, Sees Success

2024-08-05 - EOG Resources’ test at the northern end of its 140-mile-long north-south leasehold produced IPs similar to those from a nearby pad.

Exxon Surprises with Smaller FPSO for Guyana’s Hammerhead Project

2024-07-19 - Exxon Mobil Corp. announced plans for its seventh development offshore Guyana, Hammerhead, which will add 120,000 bbl/d to 180,000 bbl/d of production capacity starting in 2029.

In Ohio’s Utica Shale, Oil Wildcatters Are at Home

2024-08-23 - The state was a fast-follower in launching the U.S. and world oil industry, and millions of barrels of economic oil are still being found there today.

Comments

Add new comment

This conversation is moderated according to Hart Energy community rules. Please read the rules before joining the discussion. If you’re experiencing any technical problems, please contact our customer care team.