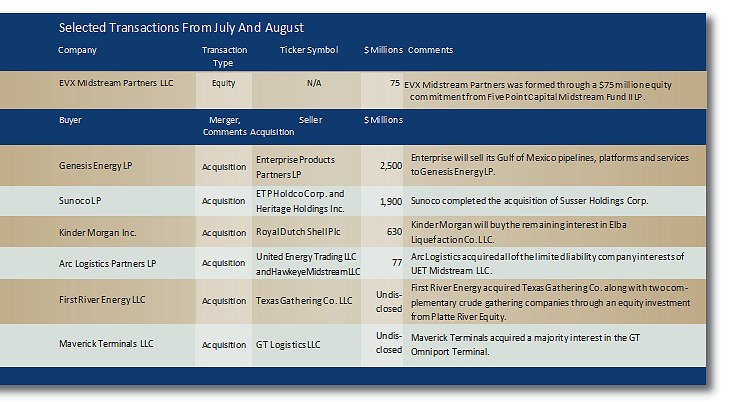

Our strategy is not just to be a dropdown story,” Gary Heminger, chairman of the board and CEO of MPLX LP, told Midstream Business last November. “We’re going to continue to be organic, and we would expect to continue to be acquisitive in how we would look at this type of business going forward. I think we have a very, very long growth profile in this space.”

MPLX took a very, very long step in that direction when it announced a $15.7 billion bid to acquire MarkWest Energy Part-ners LP in July. The unit-for-unit transaction carries an enterprise value of around $20 billion.

What happens when a company with market cap of $4.23 bil-lion tries to take over a company with market cap of $11.98 billion? In this case, investors bailed.

MPLX’s stock took a 14.5% hit the day the deal was an-nounced and by August was down 27.4%. MarkWest enjoyed a 14% hike initially but by August had shed 2.4% of its value.

J.P. Morgan analysts see the negative reaction as an overreaction.

“We believe the market’s response to the merger proposal is overdone,” they wrote after discussions with senior management of the companies. J.P. Morgan’s analysts acknowledge guidance of a lower trajectory for MPLX, but think that investors leaned too far to the downside and believe that parent Marathon Petroleum Corp. will do what it takes to support its MLP.

J.P. Morgan also warned of obstacles complicating the market environment, including the resumption of West Texas Intermediate’s price decline, challenged NGL supply-demand balance and possibility of rising interest rates. For MarkWest investors, the synergies of the deal that include MPLX’s northeast presence shield them from those risks. They note that the company backed off of some Utica opportunities and likely some in the Permian as well.

MarkWest unitholders “benefit from the increased size and scale of pro forma MPLX in both an upside and downside scenario,” the analysts write. It’s a good deal, end of story. Or at least this chapter.

Recommended Reading

Ithaca Deal ‘Ticks All the Boxes,’ Eni’s CFO Says

2024-04-26 - Eni’s deal to acquire Ithaca Energy marks a “strategic move to significantly strengthen its presence” on the U.K. Continental Shelf and “ticks all of the boxes” for the Italian energy company.

Apollo to Buy, Take Private U.S. Silica in $1.85B Deal

2024-04-26 - Apollo will purchase U.S. Silica Holdings at a time when service companies are responding to rampant E&P consolidation by conducting their own M&A.

Deep Well Services, CNX Launch JV AutoSep Technologies

2024-04-25 - AutoSep Technologies, a joint venture between Deep Well Services and CNX Resources, will provide automated conventional flowback operations to the oil and gas industry.

EQT Sees Clear Path to $5B in Potential Divestments

2024-04-24 - EQT Corp. executives said that an April deal with Equinor has been a catalyst for talks with potential buyers as the company looks to shed debt for its Equitrans Midstream acquisition.

Matador Hoards Dry Powder for Potential M&A, Adds Delaware Acreage

2024-04-24 - Delaware-focused E&P Matador Resources is growing oil production, expanding midstream capacity, keeping debt low and hunting for M&A opportunities.