The International Energy Agency reported in its World Energy Outlook 2017, “A new gas order is emerging, with U.S. LNG helping to accelerate a shift toward a more flexible, liquid global market.”

U.S. LNG exporters are certainly turning world markets topsy-turvy. Since Cheniere Energy Inc. began commercial operations at its Corpus Christi Train 1 in Texas in 2016, the U.S. has overtaken Malaysia as the third largest exporting country.

“The U.S. has truly been a game changer for the industry. We think that U.S. LNG competition has resulted in a more dynamic, more competitive and

more resilient trade system, which is good for everyone,” said Andrew Walker, vice president of LNG strategy and communications for Cheniere, at last

fall’s Gastech Conference in Houston. “It is making LNG more abundant, more affordable and more secure for buyers.”

Diverse customers

Cheniere now has 20 long-term customers. Walker noted that when looking at these customers, there are different types, including national oil companies, international oil companies (IOCs), trading houses and utilities as well as different geographies.

Most companies are generally in agreement on LNG trade. Shell said in its LNG Outlook 2019 that LNG trading reached 313 million metric tons (MMmt) in 2018. The company expects LNG demand to reach 384 MMmt this year.

China has emerged as the world’s largest gas importer with LNG imports doubling in two years. LNG exports grew by 27 MMmt with half of the growth

coming from Australia.

“Encouragingly for the long-term health of the global LNG market, the average length of contracts doubled from around six years in 2017 to about 13 years in 2018. There were more than 1,400 spot cargoes in 2018,” according to Shell.

“A rebound in new long-term contracting in 2018 could revive investment in liquefaction projects. There is a potential for a supply shortage in the mid-2020s unless more LNG production project commitments are made soon,” said the company.

In three short years, the industry has gone through a major transformation when it comes to contracts, indexation, pricing, gas supply, markets and players. More change is on its way.

Peak demand

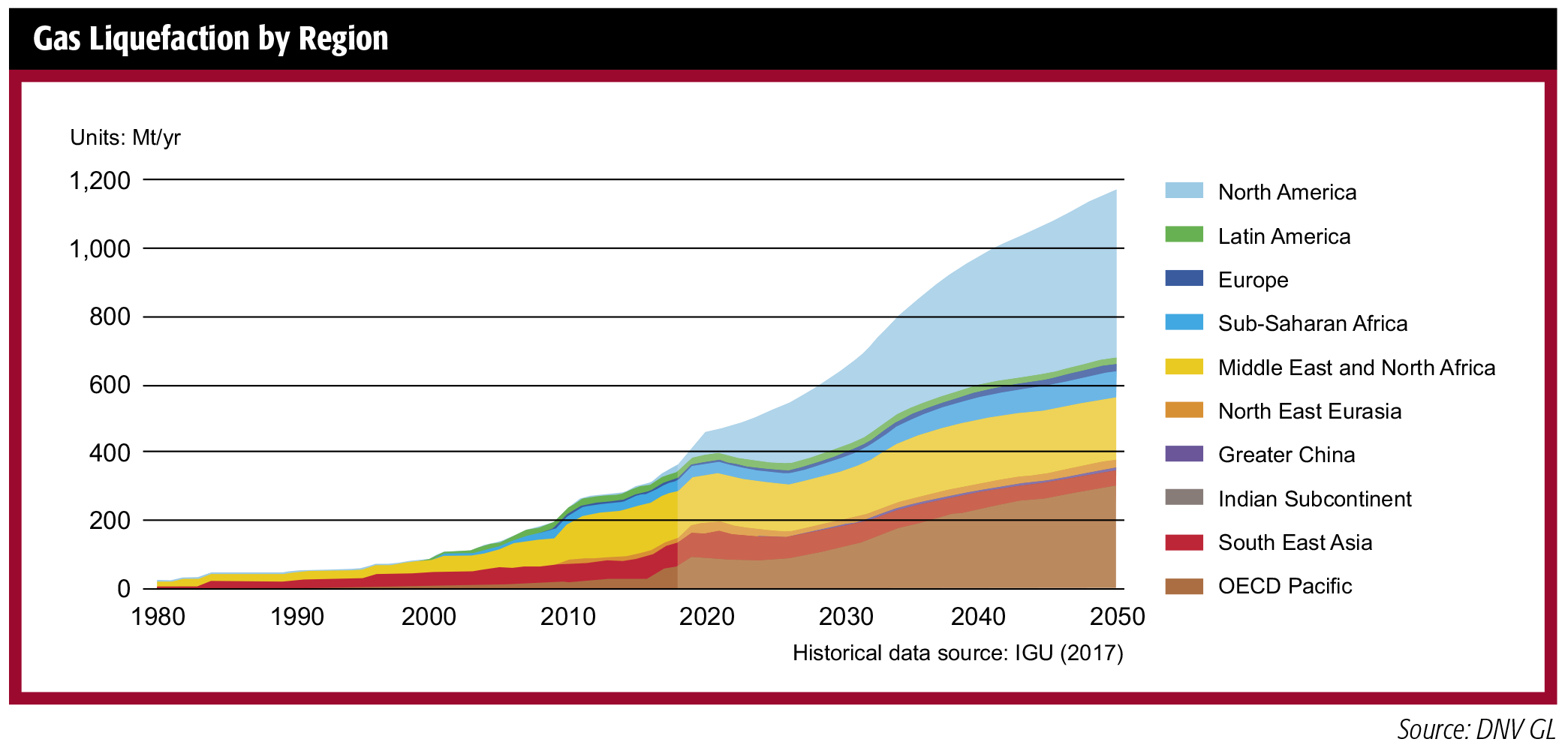

“Global gas demand will peak in 2033, then slowly decline to 2050 with some variation in supply sources. Conventional onshore gas production will peak in 2033 with offshore gas production peaking in 2040,” according to DNV GL’s Energy Transition Outlook 2019.

“Unconventional onshore gas is forecast to continue rising slowlyto [2050],” said Hans Kristian Danielsen, marketing and sales director, oil and gas, at DNV GL, in a recent presentation. “We see gas continuing to grow. It will actually surpass oil as the world’s primary energy source in 2026 and continue to grow into 2033.”

Demand for LNG will follow a similar trend. The company’s model shows that 298 MMmt of LNG were traded in 2018. For 2019, it predicted total trading of 320 MMmt. In 2050, the model predicts a little less than 1,200 MMmt.

The predictions point to a rosy future for U.S. LNG. There are now 42 LNG importing markets. A record for new sanctioned capacity is expected for the 2019-2020 period. “That’s over 100 million metric tons of new capacity … alone and quite a few of those have already reached final investment decision,” said Elizabeth “Betsy” Spomer, board adviser for Gas Strategies Group Ltd.

But there are some potential difficulties as with all complex negotiations. The new capacity “is going to have huge implications going forward as this market probably stays unbalanced to the buyers’ benefit,” she said.

Portfolio players

“One of the things that has allowed this to happen is a breakdown in the development of supply through the emergence of portfolio players—the big IOCs that take equity positions in these projects and then use their balance sheets to support sales and purchase agreements with or without designated markets. It will be interesting to see how this imbalance plays through the next several years,” Spomer continued.

“Gas Strategies projects the market is going to stay on into the late 2020s based on what’s been achieved to date. You have a 250 million metric ton variance between supply and demand in 2035. That’s massive,” she said.

At the Gastech conference, Spomer questioned, “Where are the deals? Why haven’t we seen a whole slew of deals announced? Where are all pending FIDs [final investment decisions]? I think uncertainty and current low prices have been a drag on all these things.”

Blackstone Energy Partners CEO David Foley said the developers of the next wave of U.S. LNG projects will face “tougher” market conditions for bringing new plants online at the conference.

“In terms of liquefaction capacity that gets FID from the U.S., the hit rate will be a lot higher on projects either sponsored by major oil companies or

expansions of existing facilities. I think the hit rate will be pretty low if you don’t have a customer that is willing to do a long-term offtake and its investment grade,” he said.

Permits might get tougher after the election this November, and pipeline construction might too, Foley noted.

“The hit rate will be a lot higher on projects that are either sponsored by major oil companies because they can contract themselves or are expansions

at existing facilities. You might have one or two new startups that might make it,” he said.

Blackstone committed $2 billion in equity to Cheniere seven years ago for liquefaction at Sabine Pass. “Cheniere has done a fantastic job in terms of

bringing those facilities on time and on budget—actually a little bit ahead of schedule—and delivering reliable service to the customers. The whole idea of the Henry Hub-based prices has really taken off globally,” he said.

“Getting long-term contracts from investment-grade companies that could stand behind the contract and provide a good sensible basis for project financing wasn’t easy then, but it seems to be even harder in the current market. LNG is in something of a glut right now, which makes it harder to sign up a long-term contract,” Foley added.

The new model

One of the major changes in the LNG industry has to do with increased competitiveness, according to DNV GL’s Danielsen.

“On the demand side, people are really looking for more flexible contracts. Many potential buyers don’t have the consumption or outlook to agree to 20-year, 1 million metric tons per year contracts,” he said.

In other words, there is a changing landscape in the LNG portfolio.

“We’re moving away from the old model with one operator controlling the full value chain—export, transport and import, like Shell, Petronas, etc.,” Danielsen continued.

On the international supply side, there’s plenty of activity in Australia. “Our forecast suggests that Australia’s competitiveness will lead to more LNG

trains,” he said. “Qatar is also starting to build more trains, which should bring capacity to 110 million metric tons. Russia is also high on the radar with Arctic LNG 2 and Yamal coming onstream.”

Where is the gas going? Look to China, which increased its imports by 38% from 2017 to 2018 to 56 MMmt.

In first-half 2019, “China had imported 28 million metric tons, which would lead to a 17% increase from 2018,” Danielsen said, adding that “we see a massive increase in demand from India.”

The market is definitely moving more toward flexible contracts. “Our forecast shows that North American LNG has become even more competitive,” Danielson said.

Competition’s benefits

This competition is helping the LNG marketplace. Buyers have more options to supply and manage their markets and more ability to choose the supply that suits them best, noted Cheniere’s Walker.

“We embrace competition. We think that U.S. LNG competition has resulted in a more dynamic, more competitive and more resilient trade system, which

is good for everyone. It is making LNG more abundant, more affordable and more secure for buyers,” he said.

The background to the whole story is U.S. resources.

“We have tripled the resource base over the past decade. The Potential Gas Committee released their assessment for 2018 for future gas supply at 38 Tcf [trillion cubic feet],” he said. “That also has been developed at reduced prices. Average gas price was over $8.50 per million British thermal units [MMBtu] in 2005. Today year-to-date the price is $2.66/MMBtu.”

Most markets and trades tend to evolve toward increasing competition. “LNG is doing that. We are in a very different business in the U.S. with that latent supply than we would be without it,” he said.

"Price diversification is something we offer in the U.S. that allows people to move away from the secondary indexation against oil. Destination flexibility has really changed the industry and is creating liquidity and a sustainable low-cost supply over the long run,” Walker continued.

The U.S. has increased industry diversification because the U.S. does not export as a national player. “It allows project-on-project competition unlike many exporters. We’re really seeing increased competition interproject, increased commercial competition, increased technology and cost innovation. It is going to drive liquidity,” he said.

“The U.S. is driving competition in the marketplace but more importantly driving liquidity. You can appreciate the impact this is having in the marketplace,” he added.

Premier provider

Sempra LNG said in an early 2020 announcement that its goal is to become the “premier” North American LNG company. The firm revealed an interim participation agreement with Aramco Services Co. for its Port Arthur, Texas, project.

“The measure of ‘premier’ for us is reaching 45 million metric tons per year,” said Justin Bird, president at Sempra LNG. “Our focus is really on building the infrastructure in North America so that we can export clean-burning U.S. natural gas to other countries around the world as they make a clean-energy transition.”

The company’s plan to reach that goal includes three trains at Cameron LNG, Phase 1 at Energia Costa Azul (ECA) in Mexico, the first two trains at Port

Arthur LNG, Phase 2 at Cameron LNG and Phase 2 at ECA.

The first step in the plan began last year with commercial operations with Train 1 at Cameron LNG. The second train started liquefaction operations in December 2019, with the third train coming online in second-quarter 2020. That will be the first 12 MMmt/year, Bird explained.

Sempra has much of its capacity under contract, memorandum of understanding or heads of agreement. "Cameron Phase 1 is fully contracted to Mitsui, Mitsubishi and Total. Total has signed an MOU to take up to 9 million metric tons per year of capacity of both Cameron Phase 2 and ECA LNG, which would be an expansion. It is likely the customers would be the same as Phase 1,” he said.

Getting it wrong

Sempra has learned quite a few lessons between the development of Cameron LNG as a regasification facility and its redevelopment into a liquefaction plant.

“We got regas so wrong, as did many others, but it became pretty attractive for liquefaction. I would say being able to take underperforming assets and

turning them into wonderful projects is a great experience. That really worked well,” Bird said.

Sempra has taken advantage of both Cameron LNG and ECA being brownfield projects. “Cameron Phase 1 was a regas asset that was being underutilized. What it allowed us to do is take a lot of that infrastructure and use it to see significant savings versus a newbuild. Some of the common facilities are in place. Right now the parties are figuring out what is the optimal design for the Phase 2 expansion to make it very cost competitive,” Bird said.

Port Arthur is a greenfield project.

“What’s really different there is that you have a site that is expandable up to eight trains. We have some parties that want a significant equity holding. Port Arthur is a project where they can have equity,” he added. “Saudi Services is interested in Port Arthur for three reasons: Sempra can build it economically, there is a large site capable of significant expansion and they can have a significant equity holding,” he continued.

Although Cameron LNG is a tolling facility, both Port Arthur and ECA will be based on sales and purchase agreement models. That means Sempra will be responsible for gas supply to the plants. “At ECA, we will basically use existing U.S. infrastructure, probably with adding a compressor or other minor upgrade. The pipelines in Mexico are operated by our affiliate IEnova,” Bird said.

For ECA Phase 2, Sempra would build a new pipeline from the Permian Basin to ECA, which would be located in either Mexico or the U.S.

“For Port Arthur, we see the Gulf Coast as a draw. We’re comfortable that the Permian revolution is what is underpinning a lot of the U.S. LNG. There are vast amounts of natural gas looking for foreign markets because it is associated gas. The options are to flare or stop oil production. Through our infrastructure, we can help that gas find a home around the world,” he said.

Bullish on LNG

The industry has a bullish 2020 forecast for FIDs, based on record numbers in 2019. The prognosis is generally good for mid-scale liquefaction.

“The preferred model, certainly for North American liquefaction and export, is mid-scale where total plant capacity is achieved through multiple modules

rather than a single large train. Mid-scale developers are specifying lower costs per metric ton of LNG produced and shorter project timescales versus traditional baseload,” said Paul Shields, director of marketing for Chart Industries Inc.

At the opposite end of the LNG chain, small-scale import terminals, like the Klaipeda, Lithuania, floating storage and regasification unit, are proving the economic and technological viability of smallscale LNG storage and distribution. Standardization and modularization are crucial in reducing cost and timescale, and small-scale terminals also provide operational flexibility.

Integrated systems, comprising storage, vaporization and delivery, bring natural gas power to off-grid locations through the LNG virtual pipeline. Chart

has experience with both large projects, such as powering generator sets at mines, through to enabling small/medium enterprises to switch to natural gas from other liquid fuels.

In the marine sector, new International Maritime Organization regulations mandate that sulfur content in marine fuels has to be reduced from 3.5% to 0.5% and to 0.1% in emission controlled areas. LNG achieves this. Consequently, there has been a large increase in the number of LNG-fueled vessels on the water, under construction and ones classed as marine ready.

That means that greater investment is needed in the bunkering infrastructure, and there are a number of new facilities in operation or being built, both landbased and bunkering vessels.

In Europe, there are a number of companies investing in developing the refueling infrastructure for LNG trucks. Main drivers promoting LNG over diesel

are environmental and, in particular, the elimination of particulates.

Scott Weeden is a Houston-based writer specializing in oil and gas industry topics.

Recommended Reading

Developer Seeks Permit to Send US Gas to Mexico for LNG Exports

2024-05-22 - The project is the latest in a series of developments to convert U.S. gas into LNG and export it from Mexico's Atlantic and Pacific coasts to meet global demand.

Firm Building QatarEnergy-Exxon LNG Plant in Texas Files for Bankruptcy

2024-05-21 - Exxon, which owns a 30% stake in the project, plans "to continue to fully support Golden Pass LNG through completion," a spokesperson for the company said.

WoodMac: Permian Producers Eye Mexico’s Saguaro Energía LNG FID for Takeaway Relief

2024-07-17 - Wood Mackenzie expects Mexico Pacific to take FID on the first phase of its Saguaro Energía LNG project in either the second half of 2024 or early 2025.

Texas Freeport LNG NatGas Flows Fall to Near Zero Ahead of Hurricane Beryl

2024-07-08 - With Freeport down, gas flows to the seven big U.S. LNG export plants, including Freeport, was on track to drop to an 11-week low of 11.0 Bcf/d on July 8.

Canada’s Pembina Pipeline in No Rush to Invest in TMX

2024-05-14 - The Trans Mountain Pipeline’s toll structure has too much "uncertainty," said Pembina CFO Cameron Goldade on an earnings call.