The Southeast Asia region, primarily a net exporter of LNG, is increasingly eyeing a future where rising imports could revert the trend, according to Poten & Partners.

Overall, Southeast Asia is a major LNG-exporting region due to its gas-rich geology, but declining gas reserves are quickly pushing a number of countries to LNG imports, Irwin Yeo, Poten & Partners business intelligence senior LNG analyst, said June 21 during a webinar.

Yeo said LNG demand potential existed in Southeast Asia due to falling gas production and rising demand, but said there were external and internal headwinds to overcome.

Internal challenges range from alternative fuels and policy uncertainty to infrastructure issues, while external challenges involve competition between established buyers for term LNG, as well as renewables and green energy development, Yeo said.

“[The] current LNG price decline could offer a window of opportunity for new buyers—some have already moved to take advantage,” Yeo said, adding that firms needed to weigh the risks of importing LNG.

Firms want to avoid “overcommitting to expensive LNG, which could turn into a fiscal, political and even social hot potato, [while] missing the window to buy due to cautious evaluation, only for prices to rise again,” Yeo said.

RELATED:

Morgan Stanley: US LNG Exporters Could See Cargo Cancellations

Asian Companies Keen on US Gas Supply and LNG

Southeast Asia: major trading and maritime hub

Southeast Asia is comprised of eleven countries—Indonesia, Thailand, Malaysia, Philippines, Vietnam, Singapore, Brunei, Myanmar, Cambodia, Laos andTimor-Leste—with a population of nearly 688 million, about 8.6% of the global population, according to United Nations’ data.

The region is a major trading and maritime hub, due to its privileged West-East trading routes, also for LNG. As of April 2023, the region’s GDP was around $3.9 trillion or 3.7% of the global total, according to the International Monetary Fund (IMF).

Brunei, Malaysia and Indonesia are Southeast Asia’s principal LNG exporters. In 2022, the three countries exported over 47 million tonnes per annum (mtpa), which was about 12% of the global market, according to data in Poten’s LNG Market Outlook.

Other countries in the region, including Thailand, Vietnam, Philippines and Myanmar, are major natural gas producers; however, their production is mostly sold domestically or exported as piped-gas (intra Southeast Asia, China), according to Yeo. Timor-Leste and Cambodia are home to probable gas reserves, but none have yet to be commercialized.

On the LNG import side, Southeast Asia, more specifically Ta Phut, Thailand, imported its first cargo in 2011. Other countries such as Singapore, Malaysia, Indonesia, Myanmar and the Philippines followed thereafter. In 2022, the region imported over 20 mtpa, which was around 5% of the global market, according to Poten data. By the summer of 2024, these volumes will be on the verge of reaching 30 mtpa.

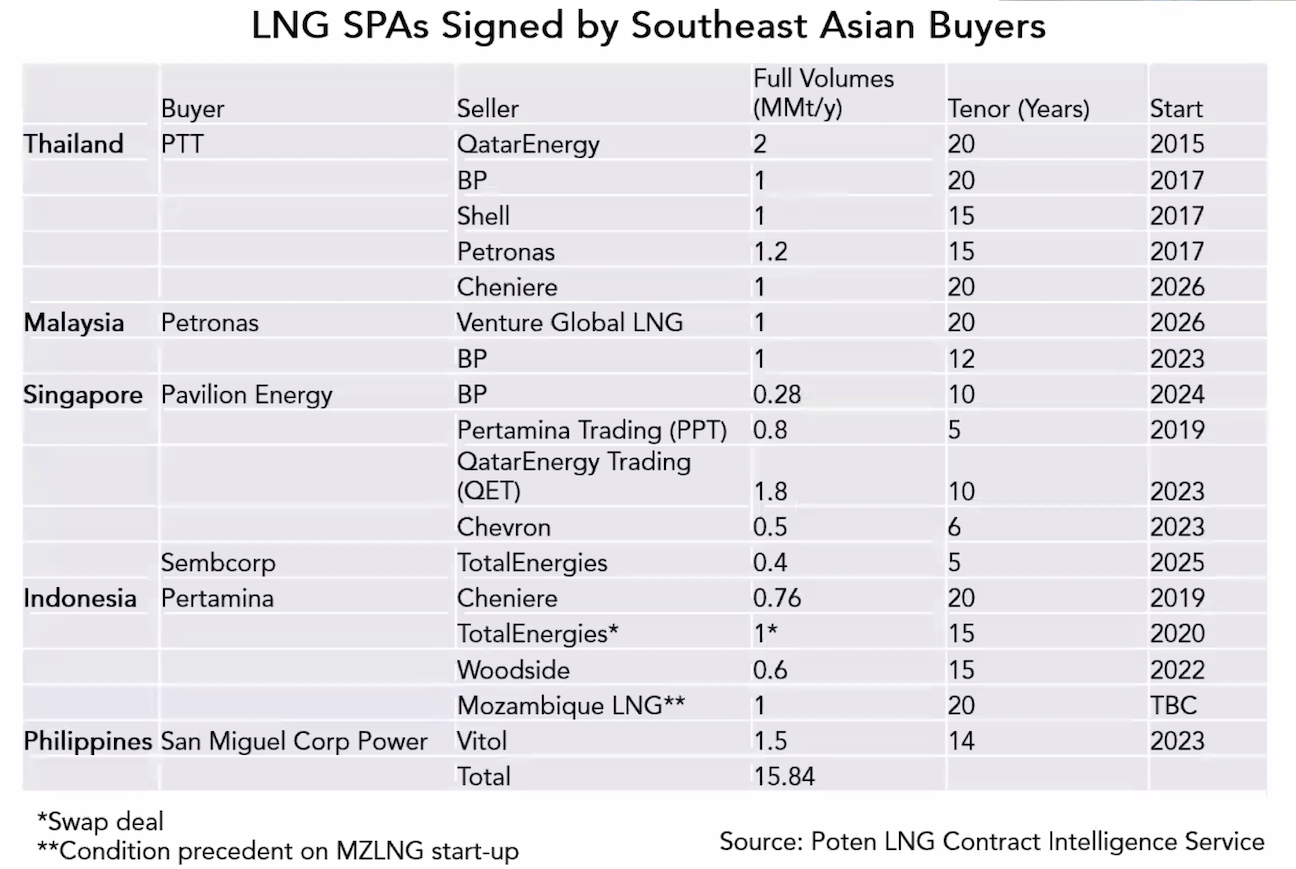

To date, Southeast Asian firms from PTT and Petronas to Pertamina have acquired nearly 16 mtpa of term LNG, according to Poten.

Overall, the Asia Pacific region is expected to import around 386 mtpa by 2032 compared to 268 mtpa in 2023, according to Poten data.

Vietnam, which is on the cusp of joining the importers' club, is eyeing its first discharge in July, while Myanmar, which received LNG between 2020-2021, has halted imports for the moment. Singapore remains well-positioned as a regional LNG hub while Malaysia and Indonesia have no import pressure yet, Yeo said.

Recommended Reading

Kissler: Mideast Tension Elevates Crude Prices—But for How Long?

2024-05-09 - Producers should be aggressive in locking in desirable crude oil prices on an abnormal market strength.

APA Corp. Latest E&P to Bow to Weak NatGas Prices, Curtail Volumes

2024-05-07 - APA Corp. plans to curtail gas and NGL production in the U.S. owing to weak Waha prices but remains confident it can deliver in the Permian Basin, CEO John Christmann said during a quarterly webcast with analysts.

What's Affecting Oil Prices This Week? (May 6, 2024)

2024-05-06 - Stratas Advisors forecast that oil demand for 2024 will increase by 1.41 MMbbl/d in comparison to 2023 and that oil demand will increase by 810,000 bbl/d in comparison to 2Q23.

TC Energy Preparing for Natural Gas Demand Surge

2024-05-06 - TC Energy executives expect data centers in Wisconsin and Virginia to drive as much as 8 Bcf/d of natural gas demand for power generation.

It’s Complicated: E&Ps Find Some Financial Tailwinds, But It’s Not All Smooth Sailing

2024-05-03 - Relatively stable WTI prices in the $80s/bbl provide some breathing room as companies allocate cash for operations, and pragmatism is seeping into the energy transition movement.