If you’re a glass half-full person—and most scions of the proud wildcatter tradition certainly subscribe to that philosophy—financing options for top performing oil and gas producers appear full of opportunity with a capital “O,” even if it means getting a little creative.

Natural gas prices remain low, even by the standards of that market, restraining both gas and oil-weighted producers. U.S. domestic politics also create uncertainty. And capital just isn’t available in the quantities it used to be.

Energy’s current share of the S&P 500 is well below historical levels. Or put another way, the combined market cap of the 23 constituent energy companies of the S&P 500 ($1.78 trillion) almost equals Amazon’s market cap.

Cautious capital

With discipline being the watchword, upstream operators looking to tap the capital markets need to be circumspect, and even a little bit creative.

It is ironic, given the general financial health of the sector, said Jeff Nichols, partner and co-chair of Haynes and Boone’s energy practice group.

“The industry is as bankable as it’s ever been,” he said,

Most top producers have “very lean balance sheets from a historical standpoint,” said Michael Bodino, managing director of investment banking at Texas Capital Bank, pointing to the financial discipline companies are showing. And, for oil-weighted companies, current pricing levels definitely help.

“There’s a robust level of cash flow out there these companies are generating,” he said.

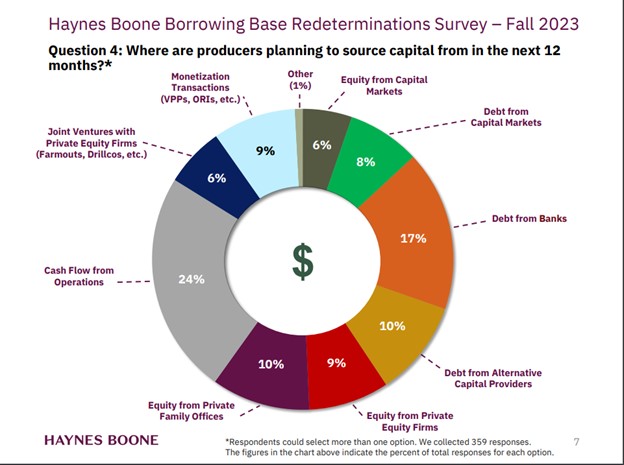

Cash flow from operations is the single greatest capital source, according to the Haynes and Boone’s biannual Borrowing Base Redeterminations Survey.

Meanwhile, traditional capital sources, such as bank debt, have seen their role diminished through a combination of factors.

Lenders are assigning “significantly lower” advance rates for non-producing wells and proved undeveloped (PUD) wells for reserve-based lending (RBL), said Jackson O’Maley, partner in Vinson & Elkins capital markets and M&A practices. Additionally, upstream firms find the uncertainty around borrowing base redeterminations disquieting.

Prices may be stable now, but companies haven’t forgotten that in volatile times, borrowing bases can be cut dramatically. “You don’t want to rely solely on the borrowing base for your liquidity,” O’Maley said.

Furthermore, many foreign banks withdrew from the RBL space, pushing upstream companies to look elsewhere for capital, added Haynes and Boone’s Nichols.

Bodino acknowledged the structural shifts in the marketplace, such as lower advance rates. The upshot is that E&P companies have moved away from using bank debt as a permanent source of capital in favor of other options, and it now forms a smaller piece of the overall debt stack.

But winds of change might be coming.

Although foreign banks withdrew from the market to reduce their exposure to energy over sustainability concerns, other lenders want back in. Owing to financial industry consolidation, many bank portfolios are now underweight to energy.

“We’re seeing a lot more interest from the bank community broadly to get new credits in their portfolios,” Bodino said.

Pensions and insurance companies chasing yield have also been eyeing the upstream sector more closely, Nichols said.

Debt options

But don’t count reserve-based loans out just yet. Though their status is diminished, Bodino said, they “play nicely in the same sandbox” with other instruments, such as leveraged loans, and have a complementary role in providing working capital.

The leveraged loan market has seen quite a bit of activity, Bodino noted. Such loans are “a better fit with companies that may have some complexity, or need an extra layer of diligence done” to get investors comfortable with an asset, he said

In September 2023, Texas Capital served as administrative agent for a $1.2 billion senior secured term loan credit agreement for HighPeak Energy. The proceeds were used to repay two outstanding senior note issuances and its outstanding borrowings on its reserve-based credit facility, according to a company press release. As a result, HighPeak was also able to enter into a $100 million super senior revolving credit facility.

The HighPeak leveraged loan had an “unbelievable level of interest,” Bodino said.

A few months later, Texas Capital also served as administrative agent for Mach Natural Resources for an $825 million term-loan credit agreement to fund the acquisition of EnCap Investments-backed Paloma Partners IV, said Bodino. On top of that very large facility, Mach also entered into an RBL, he said.

Leveraged loans are not the only market segment experiencing a surge.

The high-yield debt market has “come back pretty robustly in the last 12 months,” said O’Maley. Companies are taking advantage of the current stability in prices to “opportunistically” use high-yield debt to term out debt and create liquidity under their RBLs.

They also will be motivated to act ahead of the U.S. presidential election to avoid additional uncertainty, O’Maley said.

When traditional bank loans, leveraged loans or high-yield offerings don’t meet corporate needs, however, E&P companies must explore more exotic alternatives.

Securitizations begin to shine

With the pullback in the RBL space, companies seeking options discovered the fit of a PDP asset-backed securitization (ABS). Since 2019, dozens of ABS deals have been completed in the upstream space, said Haynes and Boone’s Nichols, whose team has advised on a number of such transactions.

Private companies have been the primary beneficiary of ABS deals, but public companies have made use of them, too.

For example, Diversified Energy, an onshore producer focused on the Appalachia Basin but with positions in the central regions of the U.S., has undertaken multiple securitizations. Until last year, Diversified had been publicly listed only on the London Stock Exchange. In December, the company began trading on the New York Stock Exchange under the ticker symbol “DEC.”

In 2022 alone, Diversified completed four securitizations totaling $1.1 billion, including a $460 million ABS done with Oaktree Capital Management for co-owned assets in Oklahoma, the company said in a news release. Diversified planned to use the funding to repay borrowings under a sustainability linked loan. The note had a fixed coupon of 7.50% owing to the BBB+ investment-grade rating assigned by Fitch Ratings.

With ABS deals, assets are dropped down into a special purpose vehicle and production is protected with hedging out five to seven years, Nichols said. That hedging enables ABS deals to secure a better rating from the ratings agencies, resulting in a lower interest rate.

Thanks to that hedging, the advance rate can be as high as 80% to 90%, said Nichols. In contrast, the current advance rate for RBLs is more in the 40% to 50% range, he said. Of course, the cost of hedging an ABS so many years out is not insubstantial.

On Diversified’s ABS deal with Oaktree, Haynes and Boone advised the trading affiliate of an undisclosed financial institution as a secured commodity hedge provider.

Securitizations definitely has some advantages, said Texas Capital’s Bodino. The upstream company retains its interest in the wells and continues to operate them, and once the ABS fully amortizes, the ownership of the wells reverts back to the company.

But investors in ABS want to avoid concentration risk and want “a lot” of well diversification, he said. No single well can account for more than 1% to 2% of production. He noted that one securitization involving Raisa Energy included over 9,000 wells.

Bodino observed that most of the companies that have completed ABS deals are “very gassy” and there hasn’t been as many oil-weighted producers. Some of that bias can be attributable to different operational characteristics of natural gas wells, which experience fewer mechanical issues and produce more steadily. But another significant factor is the different pricing dynamics of natural gas, he said.

Equity in the wings

While yield is spurring investors to re-evaluate energy debt financings, driving a rise in deal flow, equity offerings have remained relatively muted. The activity that has occurred is the result of the wave of M&A that has taken place over the last five years, O’Maley said.

Many private equity-backed companies were acquired by publics and took equity as part of the consideration. In the last year, the bulk of equity issuances have been secondary offerings by investors looking to monetize that stock, he said.

Recent examples include Permian Resources offering 48.5 million shares in March, sold not by the company but by multiple private equity firms whose portfolio companies had been acquired. Sellers included EnCap Investments, NGP Energy Capital Management, Pearl Energy Investments and Riverstone Investment Group. It was preceded by a similar offering last December of 39.4 million shares by NGP Energy Capital Management, Riverstone and EnCap. Vinson & Elkins advised on both offerings.

Meanwhile, primary common stock offerings have been scarce. But they could make a return.

The recent consolidation trend among producers is producing the newly scaled-up companies that will inevitably look to shed assets for cash—and cash only, Bodino said. Private equity-backed portfolio companies will be ready and willing to pony up, and any public company looking to compete with those buyers will also require cash. That need could lead to an increase in equity offerings, he said.

Additionally, there could be some upstream companies taking to the equity market with an IPO during the next 12 months.

In 2023, multiple companies managed to get out the door, including TXO Energy and Mach Resources, while others, such as BKV Corp., had put their public plans on hold. Nevertheless, there are more companies biding their time and looking to test the market, Bodino said.

Prospective new public E&P companies should weigh their options and choose their opening carefully, given the vagaries and complexities awaiting them, the experts said.

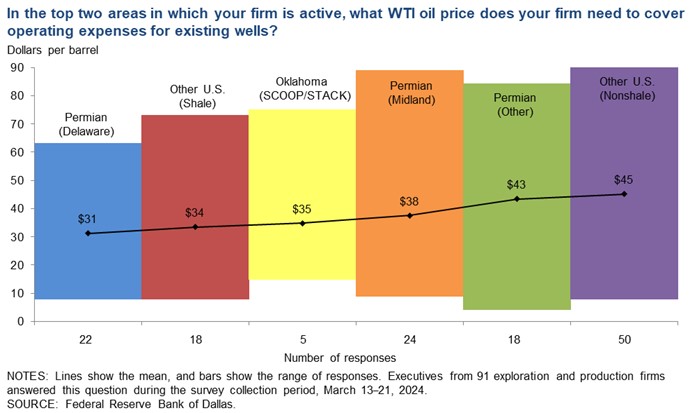

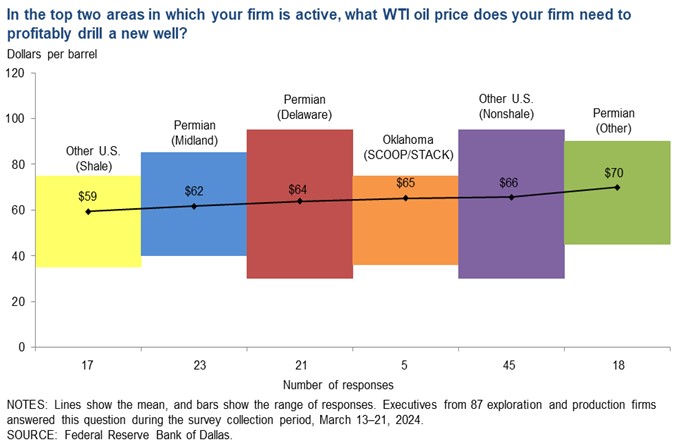

Sidebar 1: Covering costs and turning a profit

In March, when WTI prices were in the upper $70s/bbl, the Dallas Fed released its latest energy survey asking respondents to share the WTI price they need to cover operating expenses in the top two areas in which they are active. The average price was $39/bbl, up slightly from $37/bbl the prior year, but well below current WTI levels. The Delaware Basin had the lowest overall of breakeven cost of $31/bbl.

More interesting, however, is the gulf between large and small firms. Large firms (producing more than 10,000 bbl/d as of fourth-quarter 2023) require just $26/bbl to cover operating expenses for existing wells. In contrast, smaller firms (producing less than 10,000 bbl/d) require a price nearly 70% higher at $44/bbl.

Sidebar 2: Sustainability’s Sustainability

“The concept of ESG is being redefined,” said Nichols. One telling data point—natural gas has been gaining acceptance as an energy transition fuel, he noted.

Compared to a couple years ago, there is a “renewed interest” in the energy space, said O’Maley. There are even signs of pushback to ESG-driven investment strategies to divest oil and gas, he said.

“There’s less rhetoric about ESG today than there was two years ago,” said Bodino. He gives much of the credit to the upstream companies themselves for adopting ESG practices and curbing their Scope I and Scope II emissions.

The reason is simple—to be competitive in the fight to secure capital you have to address ESG. Bodino likened this shift to the Sarbanes-Oxley era in the early 2000s, where ESG has now become “a box everyone is going to ask about and need to check,” he said.

Sidebar 4: Case Study: Crescent Energy

Crescent Energy tapped the capital markets in the last 18 months to term out debt and pay down its revolving credit facility. In March, the Eagle Ford- and Uinta Basin-focused operator announced the pricing of $700 million private placement of 7.65% senior notes due 2032 to purchase the company’s outstanding 7.250% senior notes due 2026. Vinson & Elkins served as issuer’s counsel for the transaction.

Crescent Energy was formed in late 2021 through the combination of Independence Energy and Contango Oil & Gas. The company is affiliated with KKR, which owns approximately 15% of its common stock, and is helmed by David Rockecharlie, who also serves as head of KKR energy real assets business.

Crescent also tapped the high-yield market to repay amounts outstanding under its revolving credit facility. In total, Crescent raised $1 billion over the course of 2023 via four private placements of 9.250% senior notes due 2028, including two upsized offerings.

The sale of the unsecured notes, free cash flow and a modest $146 million equity raise were used to “effectively” pay for a pair of transactions Crescent undertook in the Eagle Ford for a total of $850 million, according to Fitch Ratings. The total included a $600 million acquisition of assets from Mesquite Energy, formerly known as Sanchez Energy. That deal included 75,000 acres in Dimmit and Webb counties with $700 million in PV-10 reserves.

Recommended Reading

Triangle Energy, JV Set to Drill in North Perth Basin

2024-04-18 - The Booth-1 prospect is planned to be the first well in the joint venture’s —Triangle Energy, Strike Energy and New Zealand Oil and Gas — upcoming drilling campaign.

EIG’s MidOcean Closes Purchase of 20% Stake in Peru LNG

2024-04-23 - MidOcean Energy’s deal for SK Earthon’s Peru LNG follows a March deal to purchase Tokyo Gas’ LNG interests in Australia.

Crescent Point Divests Non-core Saskatchewan Assets to Saturn Oil & Gas

2024-05-07 - Crescent Point Energy is divesting non-core assets to boost its portfolio for long-term sustainability and repay debt.

Permian Resources Adds More Delaware Basin Acreage

2024-05-07 - Permian Resources also reported its integration of Earthstone Energy’s assets is ahead of schedule and raised expected annual synergies from the deal.

Evolution Petroleum Sees Production Uplift from SCOOP/STACK Deals

2024-05-07 - Evolution Petroleum said the company added 300 gross undeveloped locations and more than a dozen DUCs.