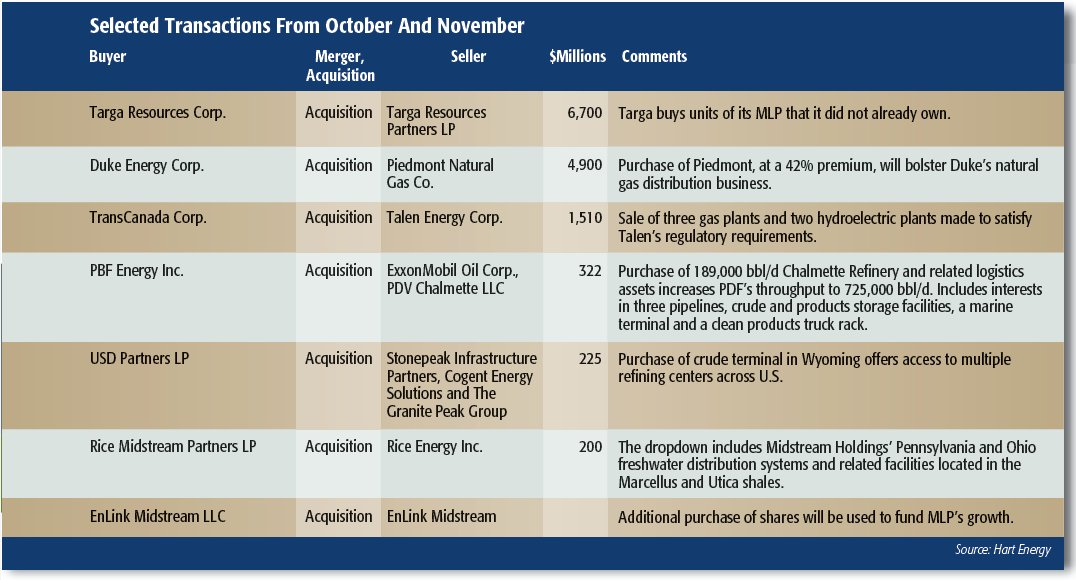

The $6.7 billion Targa Resources Corp. (TRGP) roll-up of its MLP, Targa Resources Partners LP, is a deal, not a trend. MLPs are still OK, you’re still OK.

The partnership had lost 51% of its unit price in the last 12 months, and the parent company was down 63% from its 52-week high. J.P. Morgan, admittedly cautious about the midstream operator’s outlook, welcomed the move.

“We believe a lower cost of capital, higher dividend coverage (allows for deleveraging), tax depreciation from asset step-up and a simplified corporate structure are incrementally positive for TRGP’s outlook,” the analysts wrote in their assessment of the transaction.

Not everyone was thrilled. Stifel Nicolaus lowered its rating from “buy” to “hold,” and Credit Suisse dropped its target price from $48 to $43. But Goldman Sachs raised its rating from “sell” to “neutral” and Jefferies Group reaffirmed its “buy” rating.

Sure, the combination is the third pivot to C-corp in the MLP space after Kinder Morgan Inc. and the aborted Williams Cos. move, but unique circumstances dictated these strategies.

“For certain companies of certain size with a certain history, it may be advantageous to move to a C-corp model, but generally speaking, MLP makes a lot of sense,” Brandon Blossman, managing director of Tudor, Pickering, Holt & Co. LLC, observed during Hart Energy’s recent Midstream Texas conference before the Targa deal was announced.

Peggy Connerty, equity analyst with Morningstar, urged investors to “play defense” in the MLP space as fundamentals are challenged, noting that midstream balance sheets are stretched, cash distribution coverage is tightening and cash distribution growth rates are sliding. She notes exceptions, though, including Magellan Midstream Partners LP, Spectra Energy Partners LP and Enterprise Products Partners LP.

Targa CEO Joe Bob Perkins sees the deal as helping his company rejoin the few that are thriving in the tough environment.

“This transaction is attractive for Targa’s stakeholders, with better positioning in lower commodity price environments and enhanced growth in price recovery scenarios,” he said.

Recommended Reading

CNX, Appalachia Peers Defer Completions as NatGas Prices Languish

2024-04-25 - Henry Hub blues: CNX Resources and other Appalachia producers are slashing production and deferring well completions as natural gas spot prices hover near record lows.

Chevron’s Tengiz Oil Field Operations Start Up in Kazakhstan

2024-04-25 - The final phase of Chevron’s project will produce about 260,000 bbl/d.

Rhino Taps Halliburton for Namibia Well Work

2024-04-24 - Halliburton’s deepwater integrated multi-well construction contract for a block in the Orange Basin starts later this year.

Halliburton’s Low-key M&A Strategy Remains Unchanged

2024-04-23 - Halliburton CEO Jeff Miller says expected organic growth generates more shareholder value than following consolidation trends, such as chief rival SLB’s plans to buy ChampionX.

Deepwater Roundup 2024: Americas

2024-04-23 - The final part of Hart Energy E&P’s Deepwater Roundup focuses on projects coming online in the Americas from 2023 until the end of the decade.