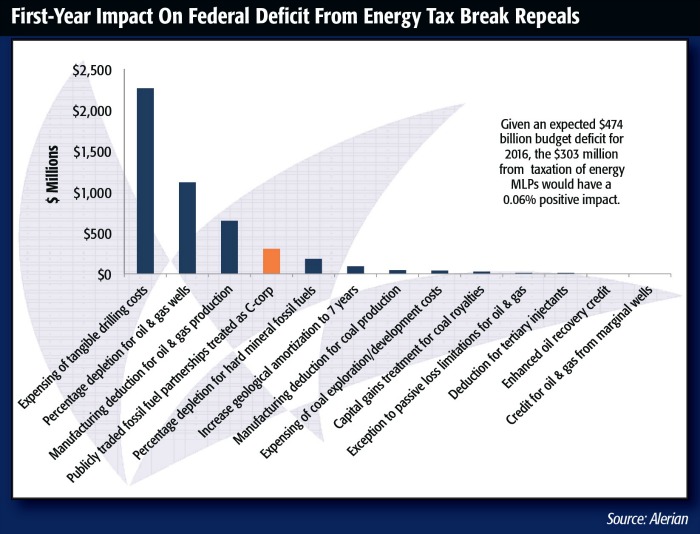

The Obama administration released its 2016 budget in February. Ever since 2009, this administration’s budget has had a long list of “fossil fuel tax preferences” to eliminate. This year, fossil fuel publicly traded partnerships (i.e., energy MLPs) are included.

Notably, MLPs would not start paying corporate taxes until 2021 when the administration estimates it would raise $303 million in the first year, and $1.7 billion through 2025. This amount pales in comparison to the national deficit, currently $18.1 trillion and also is dwarfed by the billions spent each year by MLPs on the nation’s energy infrastructure.

Each year, the president submits a budget request to Congress between the first Monday in January and the first Monday in February. This is where we are now. The budget is then submitted to the House and Senate budget committees, as well as the Congressional Budget Office, which publicly publishes an analysis in March. The House and Senate consider the budget resolutions submitted by their respective committees, and by April 15, are expected—but not required—to pass a resolution. Negotiations ensue. When there is a final budget passed by Congress, the president may either sign or veto it. Of course, this involves everything proceeding smoothly, which rarely happens.

We digress.

In the past, Congress has simply ignored the administration’s fossil fuel recommendations. A GOP-controlled Congress is unlikely to include this particular resolution simply because Obama suggested it. So, there are at least eight months before this could even potentially turn into a panic attack. Also, if the 120-odd energy MLPs with a market capitalization of $500 billion would only pay $303 million in taxes, how big of a hit would the stocks take?

Meanwhile, the other major piece of legislation involves Keystone XL Pipeline permitting. As we went to press, it had passed both houses of Congress. President Obama pledged to veto the bill based on climate change concerns. The U.S. Environmental Protection Agency issued a letter warning that Keystone XL is likely to increase greenhouse gas emissions given the current commodity price environment. The GOP is unlikely to be able to overcome the veto—four more votes in the Senate and a whole bunch in the House would be needed.

At this point, investors have discounted Keystone XL ever getting approved, so a thumbs-up from Obama would be a positive catalyst for the stock price of owner TransCanada Corp. The decision is otherwise expected to be neutral to the investment world, especially given other proposals for Canadian oil sands takeaway capacity, including Energy East, Trans Mountain, Mainline/Southern Access, Express-Platte and crude by rail.

When should you panic about Keystone XL? Probably never. But if it goes through, maybe pop open a bottle of ginger ale?

Maria Halmo and Emily Hsieh, CPA, are directors for Alerian, an independent provider of MLP and energy infrastructure market intelligence. Over $20 billion is directly tied to the Alerian Index Series. For more information, visit www.alerian.com/alerian-insights.

Recommended Reading

73-year Wildcatter Herbert Hunt, 95, Passes Away

2024-04-12 - Industry leader Herbert Hunt was instrumental in dual-lateral development, opening the North Sea to oil and gas development and discovering Libya’s Sarir Field.

Kimmeridge Fast Forwards on SilverBow with Takeover Bid

2024-03-13 - Investment firm Kimmeridge Energy Management, which first asked for additional SilverBow Resources board seats, has followed up with a buyout offer. A deal would make a nearly 1 Bcfe/d Eagle Ford pureplay.

Buffett: ‘No Interest’ in Occidental Takeover, Praises 'Hallelujah!' Shale

2024-02-27 - Berkshire Hathaway’s Warren Buffett added that the U.S. electric power situation is “ominous.”

The One Where EOG’s Stock Tanked

2024-02-23 - A rare earnings miss pushed the wildcatter’s stock down as much as 6%, while larger and smaller peers’ share prices were mostly unchanged. One analyst asked if EOG is like Narcissus.

Uinta Basin: 50% More Oil for Twice the Proppant

2024-03-06 - The higher-intensity completions are costing an average of 35% fewer dollars spent per barrel of oil equivalent of output, Crescent Energy told investors and analysts on March 5.