A Comstock Resources rig operates in the Haynesville Shale. (Source: Hart Energy)

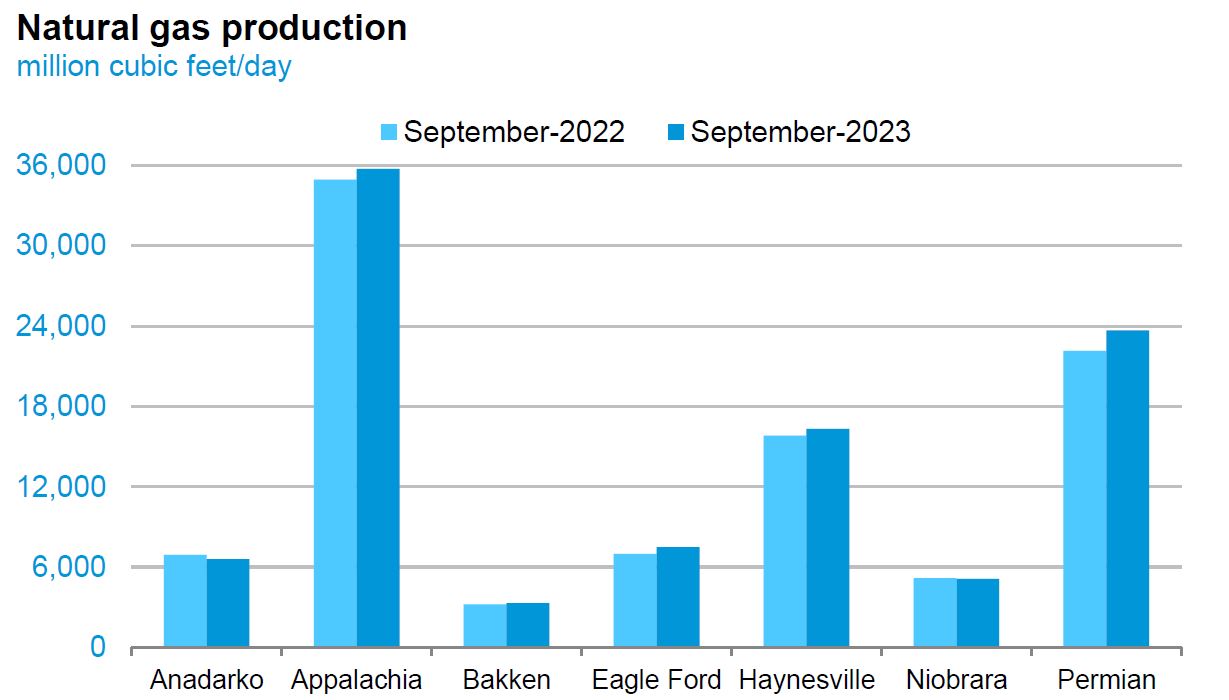

U.S. natural gas production across the Lower 48 is expected to fall again in September—by 147 MMcf/d compared to the 100 MMcf/d decrease in August.

The Haynesville Shale accounts for about 63% of next month’s anticipated drop, according to the latest outlook from the U.S. Energy Information Administration (EIA). But analysts, as well as E&P Chesapeake Energy, have spotted a potential overcount by the EIA in the number of DUCs available in the play.

And despite monthly dips in production in the Lower 48’s two dominant gas basins, production remains elevated compared with 2022. While the Haynesville (-93MMcf/d) and Appalachian Basin (-22 MMcf/d) are expected to post production declines in September, both regions continue to average far more volumes than in the first nine months of 2022.

Even as companies have laid down rigs in Haynesville, for instance, average monthly production in the play is up by 9%, or 1.37 Bcf/d, compared to the first three quarters of 2022, according to EIA data. Appalachia production is likewise up 3%, or 1.12 Bcf/d, compared to the first nine months of last year.

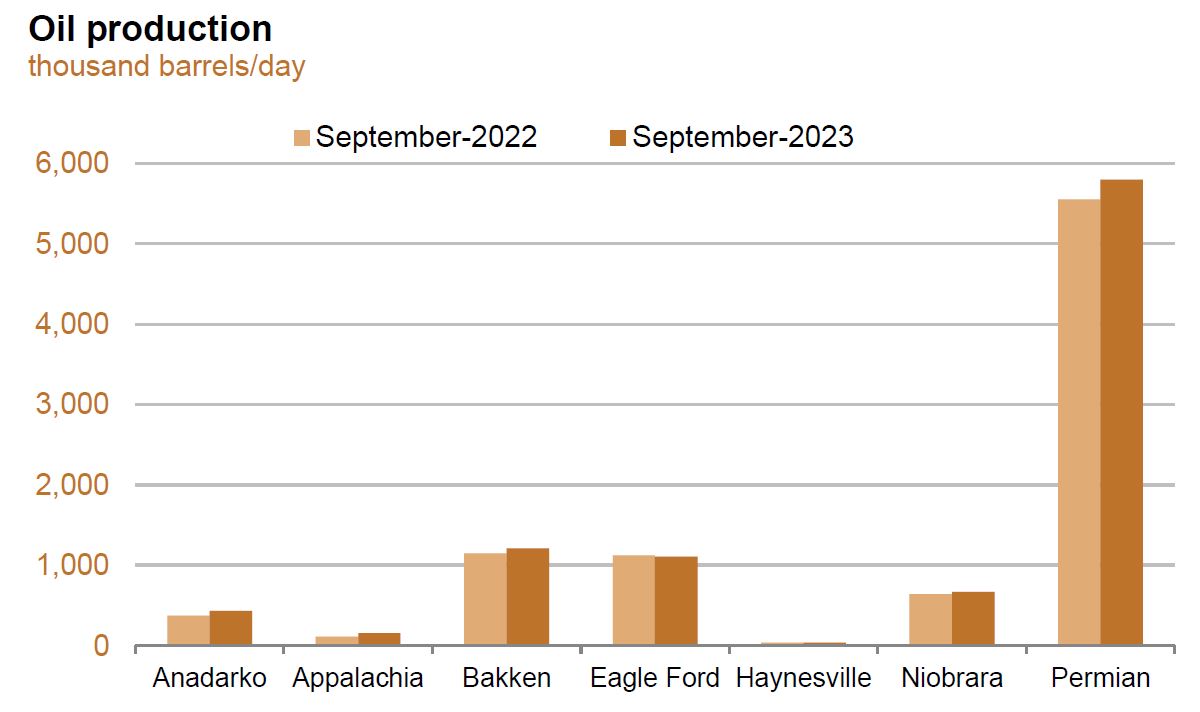

Oily plays present a more mixed state of affairs. While Permian Basin and Bakken oil production are both up compared with the first nine months of 2022, the Bakken looks to make a small rebound in oil volumes—EIA forecasts a modest 4,000 bbl/d increase in September. In the Permian, production will fall 13,000 bbl/d, according to EIA estimates. That’s after a 9,490 bbl/d drop in August. The Permian is forecasted to produce 5.79 MMbbl/d in September.

In other regions, EIA forecasts the following changes:

- Anadarko Basin oil production is expected to drop 2,000 bbl/d and its natural gas by 61 MMcf/d;

- Eagle Ford oil will fall by 11,000 bbl/d and natural gas by 41 Mcf/d; and

- the Niobrara will see oil production increase by 3,000 bbl/d with gas volumes up 12 MMcf/d.

Faux DUC dynasty?

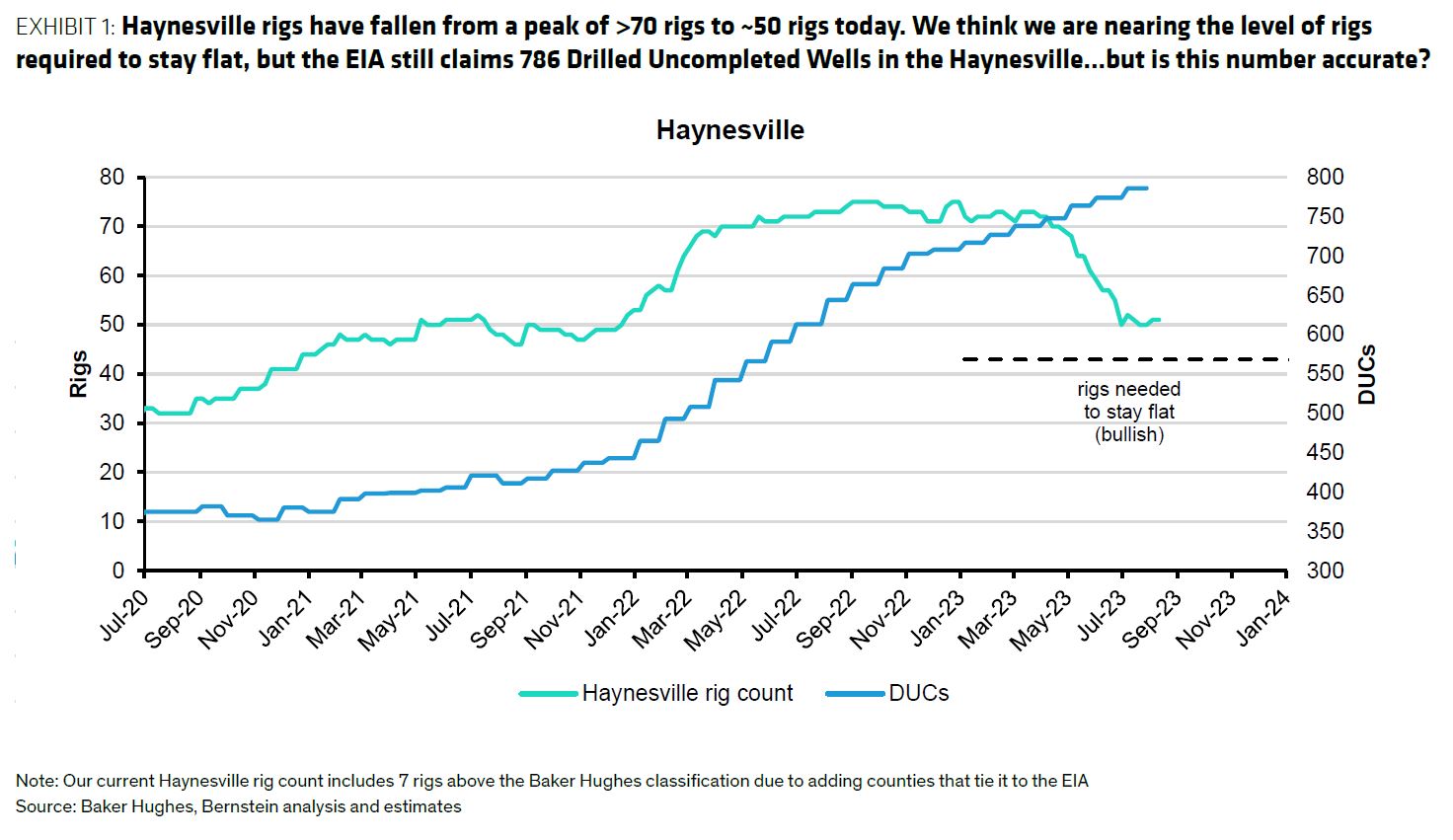

Even as the Haynesville’s production continues to moderate, its DUC inventory appears to be misleading. As of July, EIA reported that the shale play had 786 DUC wells waiting to be completed.

Or did it?

In an Aug. 18 report, Sanford C. Bernstein analyst Jean Ann Salisbury questioned how many of the Haynesville’s DUCs are “real.”

EIA’s 786 DUC number represents more wells than come have online in the Haynesville in a given year, she said.

Haynesville rigs have fallen from a peak of more than 70 rigs to about 50 rigs currently.

“We think we are nearing the level of rigs required to stay flat, but the EIA still claims 786 drilled uncompleted wells [DUCs] in the Haynesville,” Salisbury said. “But is this number accurate?”

Salisbury noted that Chesapeake and Southwestern said on recent earnings calls that the true number of viable DUCs is probably closer to 200 than 786, “obviously a big difference.”

On Chesapeake’s Aug. 2 earnings call, Chesapeake COO John Viets acknowledged “there is a lot of noise in the public data” related to DUCs.

“We would generally align in that this metric is most commonly overstated,” he said.

Viets said some of those DUCs may fall into non-core zones that can’t actually contribute, either because of mismatches in the number of units of production a rig or a frac crew is creating along with abandoned wells that may never be completed.

Using Chesapeake’s own data set and comparing it with data from public information suggests that the Haynesville’s DUC inventory is 45% of EIA’s 786 figure.

“What we see is the majority of these, roughly two-thirds, are actually sitting on pads that we’re actively drilling,” Viets said. In other words, he said those aren’t true DUCs, according to a Seeking Alpha transcript.

He painted a scenario in which three wells were completed per pad. With two frac crews in place, that would “put you into a pretty normal working inventory.”

The upshot: Viets said the Haynesville’s DUC inventories are probably somewhere closer to 150 to 200 DUCs as opposed to other published inventories, including the EIA’s.

“So again, that's just using our internal data to kind of back into maybe where the industry sits as a whole,” he said.

Salisbury said that the Haynesville, unlike oily basins, hasn’t been drawing down DUCs over the past two years but adding to them.

“This has been caused by a combination of low near-term gas prices + contango, and pipeline constraints exiting the Haynesville, which have now generally been solved,” she said.

Bernstein has two main differences with EIA assumptions. First, the DUCs being counted now were drilled prior to 2021 and are unlikely to ever be completed, accounting for about “380 of the 786 wells in the EIA dataset.”

The remaining 400 DUCs could be looked at as viable, but Salisbury posits that number is also inflated.

“However, we believe that this number is also inflated because the EIA is effectively using an old placeholder assumption for rig drill time (1.0 wells/rig/month, which seems to have slowed down to 0.9 wells/rig/month due to longer laterals),” Salisbury said. “Over time, and especially in 2022, when there was a high number of rigs, this led to an overestimate of ~100+ more wells drilled than it appears were really drilled” based on Enverus data.

“In total, this suggests around 250-300 DUCs added since 2020, which are probably viable; still bearish, but enough to be worked through within 1-2 years,” she said.

Recommended Reading

Axis Energy Deploys Fully Electric Well Service Rig

2024-03-13 - Axis Energy Services’ EPIC RIG has the ability to run on grid power for reduced emissions and increased fuel flexibility.

Betting on the Future: Chevron Technology Ventures’ Investment Strategy

2024-04-09 - After a quarter century, Chevron Technology Ventures seeks both incremental and breakthrough technologies with its early-stage investment program.