The road to inefficiency is sometimes paved with good intentions. Fossil fuel divestment has become a buzzword over the past year, as universities have come under increasing pressure from environmental groups and students to divest fossil fuel investments. The results are not always as beneficial as envisioned, however.

University endowments risk receiving lower returns on overall investments and taking losses during the divestment process. And, there are the practical and policy challenges in identifying and undertaking divestment. According to various experts, the movement to make endowments divest oil and gas assets may be well-intentioned, but in practical matters, it leaves much to be desired. There may be better ways of achieving their ends.

According to the latest National Association of College and University Business Officers (NACUBO) and Commonfund study, endowments in the U.S. total over $516 billion. For the 2014 fiscal year, they averaged a return of 15.5%, net of fees. Endowment managers are constantly on the prowl for attractive investments, and oil and gas assets and equities provide what many consider to be an appealing avenue.

Colleges have helped to fan the flames of fossil fuel divestment. According to the National Association of Scholars, 475 colleges and universities in the U.S., Canada, Australia and Europe now offer programs relating to sustainability and climate change. In the U.S. alone, there are 1,274 programs relating to sustainability offered, with at least one in every state. And partly as a result, more than 400 student-led fossil free divestment campaigns are ongoing across the U.S.

A distraction

This hullaballoo around divesting fossil fuel investments is a distraction from the real issues, according to Jeff Eshelman of the IPAA.

“It’s really mostly about grabbing headlines with no tangible impact on the environment or the climate change movement,” he said. “It’s really a distraction from gaining any sort of real discussion on climate change on college campuses.”

Much of the headline-grabbing behavior will have little effect on oil and gas companies, Eshelman believes.

“So we’ve seen these activist groups attract a lot of attention in the news media, but has their impact really been felt in the companies? The answer is no.”

The IPAA launched a website, divestmentfacts.com, to provide background on the issue of divestment, and conducted a survey of investment managers associated with universities. Few had either heard of or seriously considered divestment. But Eshelman warned that those considering divestment threaten the financial mandate of their endowments to deliver solid investment returns.

“The people who have the most to lose by the divestment campaign are not the oil and natural gas companies but rather the students who benefit from fossil fuel investments in the college endowments. Their financial aid, the upkeep, maintenance and improvements to the academic institutions and even pension funds, these are the ones who have the most to lose by the divestment movement, not the industry itself.”

The superficial is outranking substance. “In reality, it’s not gaining as much attention in the boardrooms of these universities as it is in the newsrooms,” he said.

Private equity funds for energy that take in money from endowments may not be affected by the divestment movement either. So far, the funds that have raised capital recently have been able to aggregate capital from their endowment limited partners just as they always have. Said one Houston PE manager, “So far this is not an issue for us. And what’s more, it’s not our fight to fight. If the CIO of a university endowment calls us and says he can no longer invest with us because we are in fossil fuels, what can we do?”

Another PE firm said it has fielded a few questions on the environmental and social policies of some of its portfolio companies, but it has seen its companies largely address the issue of the environment in a responsible way. It hasn’t seen a gain in momentum from the divestment movement.

Costs outweigh benefits

Divestment from oil and gas is a costly and ineffective strategy for combating climate change, according to a report written by Prof. Daniel R. Fischel and the Chicago-based consultancy Compass Lexecon.

The report looked at the potential for loss by divesting from public equities, and it delineated three main areas where doing so would generate costs. The first was simple trading costs; by declaring that you will be selling for noneconomic reasons, you will likely court unproductive bid-ask spreads, and taxes, exchange fees and commissions will follow.

The second cost of divestment, according to the report, was compliance.

“It refers to the fact that saying, ‘I’m going to divest from oil and gas stocks,’ is not so simple when you think about it,” said Todd Kendall, a senior vice president at Compass Lexecon who was heavily involved in writing the report. “What is a fossil fuel stock? It’s easy to point to a couple of big oil and gas concerns, but even there, it’s not so simple because many of those companies do a lot of work in renewables and other things you might feel like you want to support.”

Kendall added that it’s not obvious why a portfolio manager would want to make the oil and gas producers the targets as opposed to the companies that consume fossil fuels: utilities, airlines, auto manufacturers.

“It’s very, very difficult to draw the line,” he said.

Doing so would necessitate significant effort, and that effort would manifest itself in the form of higher management fees, he said.

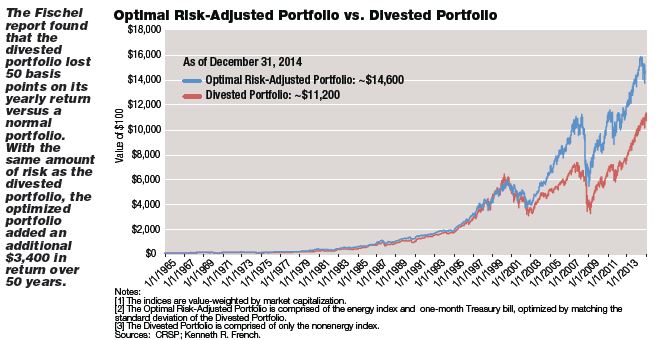

The third way divestment’s costs outweigh the benefits lies in energy’s diversification value. According to the report, the energy sector has the lowest correlation with the nine other Fama and French-defined sectors of stocks, making it a valuable diversification tool.

“Essentially, if you’re divesting from oil and gas or energy securities more generally, you’re cutting off an option for your portfolio,” Kendall said.

Kendall and Fischel quantified the potential loss incurred from divesting public energy equities. Over a 50-year period, on a risk-adjusted basis, investors risk losing 50 basis points (0.5%) in their return per year. According to the study, that loss adds up to a total portfolio shortfall of about 23% versus a nondivested portfolio.

“It’s a really substantial cost and has an important impact on these universities’ or other institutions’ ability to satisfy their institutional goals to fund student research and student scholarships, so we think that the diversification cost in addition to the trading cost and the compliance cost are something that any investor would really need to think hard about before they decided to divest.”

Results so far

So far, of the hundreds of colleges and universities in the U.S., about two dozen have decided to divest. Of the 15 for which data was available, their endowments represent about $27 billion. There are wrinkles with that amount, however. Stanford, which represents about $21 billion, has only promised to divest its coal investments. So the amount promised to the divestment movement is about $6 billion. Of those 15, the largest is the University of Washington, with an endowment valued at $2.8 billion.

Many endowments, however, have decided not to divest. Mark Warner, the senior managing director of the University of Texas Investment Management Co. (UTIMCO), said that the $36 billion in investments that his company manages for the University of Texas and Texas A&M University systems is not looking to make investment decisions on social grounds.

“We get approached from time to time by a variety of our constituents on any number of issues that I would categorize as noneconomic,” Warner said. “Our universal approach is that we are a global investor managing a globally diversified portfolio, and we don’t endeavor to address social concerns through our investing.

“The investing business is difficult enough. When one makes an initial calculation on a social basis with regard to their investing policy, where the next will lie and where to draw the line is difficult. Our view is, we have a very clear mandate. And that is to grow and manage the assets of the University of Texas and Texas A&M systems to the very best of our abilities, to preserve their purchasing power over the very long term. And that just doesn’t include a social mandate.”

On a general, look-through basis, UTIMCO has about 10% of its endowment tied up in oil and gas assets, Warner said. That amount is no accident; UTIMCO routinely performs an evaluation to make sure industry asset allocations line up with factors such as how an industry contributes to global economic activity and an industry’s market capitalization. Deciding to divest would take some time, as about 30% of the overall portfolio is tied up in private investments that would take several years to exit. Another problem surfaces when an endowment declares it’s a seller for social reasons; potential buyers adjust accordingly, resulting in an injury to the endowment’s return.

“We don’t invest along a variety of social continuums. We just can’t do it. It’s not our mandate,” Warner said.

Harvard University, the largest single private university endowment in the U.S., at about $36 billion, has said it respects the challenge of climate change but does not believe divestment is “warranted or wise.”

Harvard president Drew Faust has issued a statement pointing out that the endowment serves above all an academic mission. “The funds in the endowment have been given to us by generous benefactors over many years to advance academic aims, not to serve other purposes, however worthy,” she wrote.

She also recognized that divestment threatened to turn the university into a political actor, and that using an economic resource for social purposes “can entail serious risks to the independence of the academic enterprise. The endowment is a resource, not an instrument to impel social or political change.”

Faust worried that divesting would impair the financial mandate of the university. “Despite some assertions to the contrary, logic and experience indicate that barring investments in a major, integral sector of the global economy would—especially for a large endowment reliant on sophisticated investment techniques, pooled funds and broad diversification—come at a substantial economic cost.”

Faust echoed Eshelman’s comments about how divestment may just be a distraction, and as such, it would not impel the intended consequences. “Universities own a very small fraction of the market capitalization of fossil fuel companies. If we and others were to sell our shares, those shares would no doubt find other willing buyers. Divestment is likely to have negligible financial impact on the affected companies. And such a strategy would diminish the influence or voice we might have with this industry.” Fischel and Kendall made this point as well.

Columbia, Cornell, Brown, University of California at Berkeley, Georgetown, New York University and Notre Dame have all declined to divest their fossil fuel holdings.

Alternatives

Industry observers agree that alternatives to divestment may have more impact on addressing climate change. Eshelman thinks that an honest discussion can only be had once the divestment issue is off the table.

“I think a discussion among students and faculty about climate change and how they can address it needs to occur, but certainly by divesting from fossil fuels, there’s not going to be any impact on the environment, and it will only be hurting students on those campuses. I think there’s just a better way of going about this than risking the financial aid and really, well-being, of the higher education system.”

Kendall thinks a carbon pricing policy would make more economic sense.

“From an economic perspective, when you’re talking about climate change, you’re talking about something that’s not priced in the economy. If the price of carbon is too low, it’s because there’s this impact on climate that nobody’s taking account of. So from an economic perspective, the right way to deal with that would be, or at least a much more efficient way to deal with that would be, something like a carbon tax.”

While unpalatable for some, it may have more effect than divestment.

Recommended Reading

Marketed: Wylease AFE Asset Packages in Johnson County, Wyoming

2024-04-29 - Wylease LLC has retained EnergyNet for the sale of three Niobrara Shale AFE (authorization for expenditure) packages in Johnson County, Wyoming.

M&A Spotlight Shifts from Permian to Bakken, Marcellus

2024-04-29 - Potential deals-in-waiting include the Bakken’s Grayson Mill Energy, EQT's remaining non-operated Marcellus portfolio and some Shell and BP assets in the Haynesville, Rystad said.

Chevron CEO: Permian, D-J Basin Production Fuels US Output Growth

2024-04-29 - Chevron continued to prioritize Permian Basin investment for new production and is seeing D-J Basin growth after closing its $6.3 billion acquisition of PDC Energy last year, CEO Mike Wirth said.

E&P Highlights: April 29, 2024

2024-04-29 - Here’s a roundup of the latest E&P headlines, including a new contract award and drilling technology.

C-NLOPB Issues Call for Bids in Eastern Newfoundland

2024-04-29 - Winners of the Call for Bids No. NL24-CFB01 will be selected based on the highest total of money the bidder commits to spend on exploration of a parcel during the first six years of a nine-year license.