Publicly traded E&P Battalion Oil is being taken private by newly formed E&P Fury Resources—bucking the more common trend of public E&Ps tucking in private assets.

Although significantly fewer small- and micro-cap public E&Ps are around today than during the shale boom, a smattering remain spread around the Lower 48. Could go-private transactions become more common for smaller E&Ps with limited runway in the public markets?

Fury Resources Inc. is acquiring all of Battalion’s outstanding common shares for $9.80 per share in cash, representing a total transaction value of approximately $450 million.

The acquisition terms imply a whopping 85% premium compared to Battalion’s closing stock price of $5.28 per share as of Dec. 14. Battalion’s shares skyrocketed more than 81% to close at $9.59 per share after the deal was announced on Dec. 15.

For Battalion Oil, which was raising money to stave off a liquidity crunch and seeking strategic alternatives, a go-private transaction with Fury was “by far the best solution for them and their common equity holders,” Enverus Intelligence Research Senior Vice President Andrew Dittmar told Hart Energy.

“They didn’t really have capital to develop their asset or go out and buy new assets,” Dittmar said.

“They were a bit hamstrung as a small public company—probably not attractive to another public company buyer given a combination of the asset quality plus the capital structure that Battalion had, which was heavy on debt and preferred equity,” he said.

The Permian Basin has seen a historic amount of M&A activity in 2023, with total upstream dealmaking rising above $100 billion for the year, according to analyses by Wood Mackenzie and Enverus.

A huge chunk of that came from Exxon Mobil’s $60 billion acquisition of Pioneer Natural Resources, the largest and most significant shale oil transaction the market has seen to date.

Public E&Ps followed suit, actively buying up the most attractive private opportunities to add greater scale in the Permian. The most recent example of the trend: Occidental Petroleum’s $12 billion acquisition of Midland Basin E&P CrownRock LP.

Several other public E&Ps, including Civitas Resources, Ovintiv Inc., Vital Energy and Matador Resources, have added greater scale in the Permian through M&A with private companies this year.

A private E&P scooping up a public player is a much rarer occurrence, Dittmar said.

“The industry is consolidated to a point where most of the small publics are going to be too big for one of these go-private deals,” Dittmar said.

The most recent comparable transaction might be the $480 million acquisition of Goodrich Petroleum Corp. by Paloma Partners VI, backed by private equity firm EnCap Investments, in 2021.

RELATED: Delaware Basin E&P Battalion Oil Acquired for $450 Million

Sweetening a sour outlook

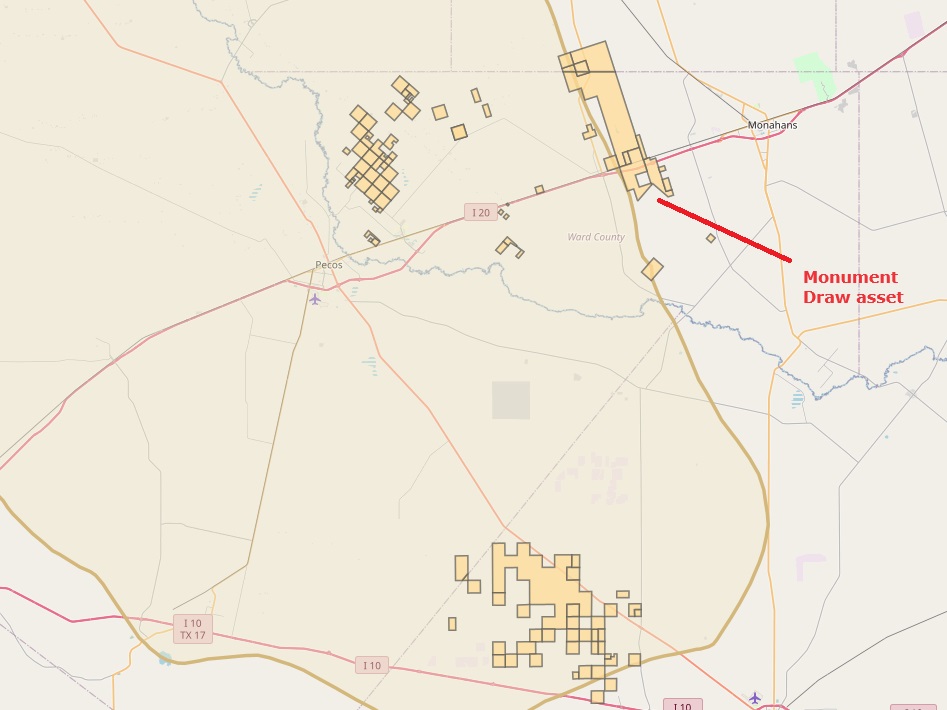

Battalion owns working interests in about 40,400 net acres in the Delaware Basin—primarily located in Pecos, Reeves, Ward and Winkler counties, Texas.

In its latest quarterly earnings, the company reported third quarter sales volumes of 12,717 boe/d.

Battalion’s main asset—called Monument Draw—sits in the eastern part of the Delaware up against the Permian’s Central Basin Platform. The company reported recommencing drilling operations in Monument Draw during the third quarter.

But Battalion has also had to manage large quantities of H2S sour gas being produced from Monument Draw.

Last year, Battalion entered into a joint venture (JV) with Caracara Services LLC to develop an acid gas treatment and carbon sequestration facility to treat sour gas volumes emerging from Monument Draw.

The acid gas injection JV project continues to go through workover operations. Additional complications were encountered with the project during the third quarter that required higher-than-expected costs, Battalion disclosed in its latest earnings report.

“Essentially because of that sour gas, Battalion has a way higher operating structure than any comparable company,” Dittmar said.

Battalion’s current forecast assumes the acid gas injection facility will be online and processing 20 MMcf/d of natural gas in the first quarter of 2024.

Developing the acid gas treatment project is expected to reduce overall gathering and related costs by 20% to 30% annually, Battalion said when announcing the project.

“Once that comes online, it should bring the operating costs more in-line with the basin average, which is going to increase the value of that asset—both the existing production and the value of the inventory,” Dittmar said.

That might have been a key consideration for Fury to move forward with a deal, he said. With sour gas treatment online, Battalion’s overall runway looks a lot sweeter.

“With the treatment facility, it’s still not going to be core Delaware—it’s still Southern Delaware, Tier 2, Tier 3,” Dittmar said. “But, it is comparable to similar quality assets in the area once you have a [treatment] facility online.”

Based on Battalion’s current operating costs, which are relatively high, Enverus estimates the production value for Battalion was worth around $300 million.

Fury is paying about $3,700 per acre, or about $1.3 million per remaining net location, to acquire Battalion.

“I think the dollar-per-location is pretty comparable to what we’ve seen for similar Southern Delaware Tier 2 or Tier 3 assets,” Dittmar said. That’s comparable to some of the deals players like Vital Energy and Callon Petroleum Corp. have inked in the Southern Delaware.

RELATED: Vital Energy Rapidly Grows in Permian with Slew of Deals

Small ball

Analysts expect the trend of upstream consolidation to continue in 2024, as the largest of the large E&Ps get even bigger in U.S. shale.

But what does the runway look like for the smallest of the small public E&Ps, which are out of favor with public investors, lack scale and are often more strapped for cash?

Selling to a private operator could be an attractive route for some smaller publics, Dittmar said.

“Right now the industry operators, private capital and M&A participants are probably a bit more bullish in how they’re willing to underwrite inventory and upside than what public markets are,” Dittmar said.

Put simply: You’re more likely to get paid for inventory locations in an M&A transaction than for public markets to credit them with value.

So, some of those small public E&Ps are exploring their options—including pursuing a sale.

The most notable example in the Permian Basin is likely HighPeak Energy, which told investors in January that it would be exploring “certain strategic alternatives to maximize shareholder value,” up to and including a potential sale.

This fall, HighPeak entered into a $1.2 billion loan credit agreement to refinance its debt in what the Midland Basin E&P said is one of the largest privately arranged financings for an independent producer. At that time, company officials declined to say whether or not HighPeak was positioning itself for a sale.

There are also several small- and micro-cap publics with positions outside of the Permian, including Evolution Petroleum, Amplify Energy and Empire Petroleum, among others.

In its third quarter earnings, Amplify Energy announced plans to pursue a complete sale of its assets in Bairoil, Wyoming; a marketing process will begin in the first quarter of 2024.

Amplify also noted that its future outlook could be affected by the company evaluating and implementing strategic alternatives.

Recommended Reading

CNOOC Discovers Over 100 Bcm of Proved Gas in South China Sea

2024-08-07 - CNOOC’s Lingshui 36-1 is the world’s first large, ultra-shallow gas field in ultra-deep water.

E&P Highlights: Sept. 9, 2024

2024-09-09 - Here’s a roundup of the latest E&P headlines, with Talos Energy announcing a new discovery and Trillion Energy achieving gas production from a revitalized field.

US Drillers Add Oil, Gas Rigs for Second Time in Three Weeks

2024-07-19 - The oil and gas rig count, an early indicator of future output, rose by two to 586 in the week to July 19, its highest since late June.

E&P Highlights: Aug. 26, 2024

2024-08-26 - Here’s a roundup of the latest E&P headlines, with Ovintiv considering selling its Uinta assets and drilling operations beginning at the Anchois project offshore Morocco.

E&P Highlights: July 1, 2024

2024-07-01 - Here’s a roundup of the latest E&P headlines, including the Israeli government approving increased gas export at the Leviathan Field and Equinor winning a FEED contract for the all-electric Fram Sør Field.

Comments

Add new comment

This conversation is moderated according to Hart Energy community rules. Please read the rules before joining the discussion. If you’re experiencing any technical problems, please contact our customer care team.