Fitch Solutions revised its Brent forecast to $70 per barrel (/bbl) for 2019 and $76/bbl for 2020 due to the sharp decline in prices last month amid concerns over a global economic slowdown and the lack of an improvement in prices even as supplies tighten.

The outlook for the global economy is mixed at best with a ton of questions surrounding U.S. trade. In addition to the ongoing trade war with China, the Trump Administration this week announced plans to impose tariffs on Mexican goods.

The Fitch report notes that if the U.S. secures trade agreements with China and Mexico, it would go a long way to easing concerns over the global economy and help support crude prices. On the flip side, should these issues persist it would create further stagnation for global markets, including crude.

Despite the downward trend to crude prices and the uncertainty over trade relations, Fitch anticipates an improved market in the second-half of the year. "In our view, the oil price is not currently reflective of market fundamentals. Our revised price view continues to take into account bullish factors that we believe will strengthen prices through the second half of the year," the report said.

These bullish factors include the likelihood that OPEC+ and other major producing countries manage the global oil market by rolling over the production cut deal that expires June 26. "OPEC+ will have the choice between rolling over the deal in its current form, altering the terms of the deal, or ending it entirely, floating barrels back onto the market. The latter course of action would be significantly bearish for price and in our view is very unlikely to take place," the report said.

Instead, Fitch believes that OPEC+ will free up about 400,000 barrels per day (bbl/d) of oil back to the market to limit the impacts of Iranian and Venezuelan supply deficits. According to the report, this strategy falls in line with the cartel's long history of increasing supply to match demand in order to maintain market stability.

U.S. producers will also play an important role in determining where global crude prices move in the years ahead. Fitch anticipates a little more than 9% year-over-year production growth in 2019. However, this is down about 7% from last year's year-over-year growth and the report anticipates a continued slowdown from domestic producers in the next decade.

"The concentration of output growth in the U.S. is unprecedented in recent decades. According to our forecasts, the U.S. will contribute around 50% of gross production growth in 2019 and over the five years to 2023. This creates structural vulnerabilities in the markets, should shale production disappoint," Fitch said. The company contends that U.S. production growth isn't sustainable in the long-term due to softening economic activity and higher prices at the pump.

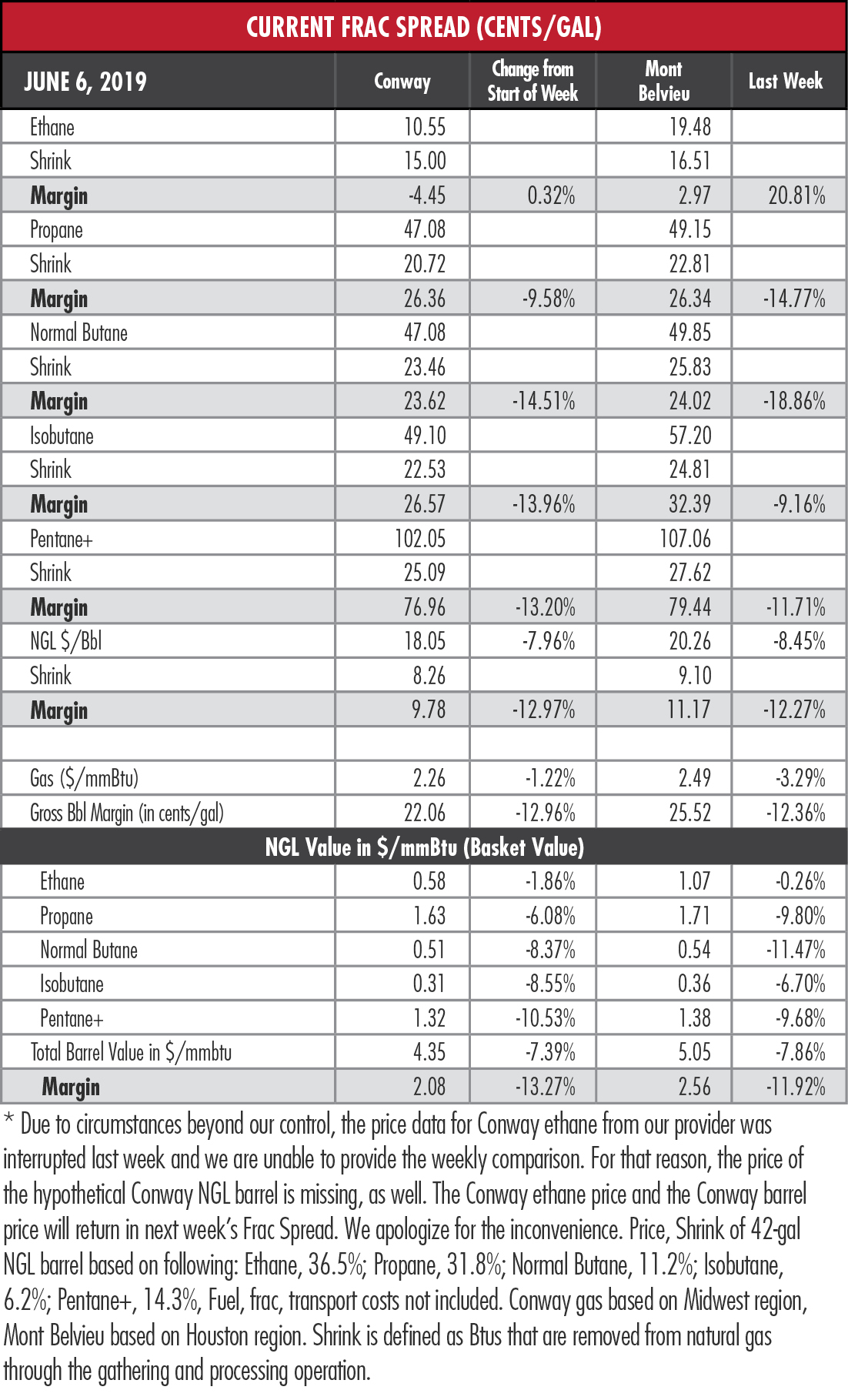

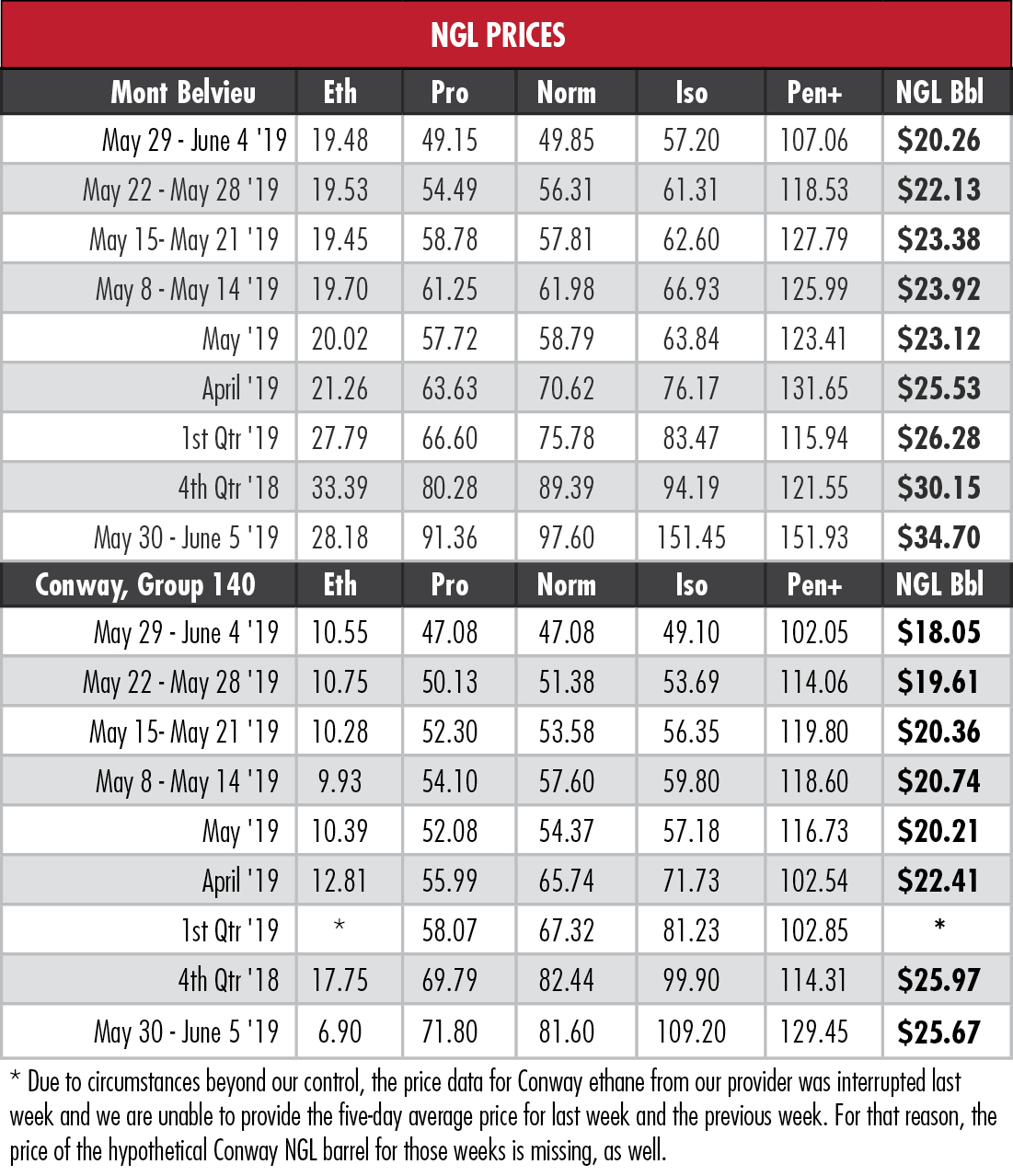

The downturn in crude prices has seen a similar downturn in NGL prices, especially heavy liquids, this past month. For example, pentanes-plus lost about 26 cents per gallon (/gal) at Mont Belvieu in the six weeks between April 24 and May 29. The loss was similar at Conway, where pentanes-plus lost 22 cents/gal over the same time frame. Isobutane lost even more value at Conway in this six-week period as it was down 23 cents/gal to 49 cents/gal after trading at 72 cents/gal at the end of April.

By comparison, light NGLs have held their values a bit better, ethane in particular has held firm since the start of April at both hubs. Mont Belvieu ethane has been trading between 19 cents/gal to 22 cents/gal since mid-March. Conway ethane has been a bit more volatile, trading between 9 cents/gal to 15 cents/gal over the same time period.

Though ethane prices are weaker compared to last year cracking capacity and demand will be increasing by 135,000 bbl/d over the next month as BASF/Total's Port Arthur, Texas ethane plant and ExxonMobil's Beaumont, Texas, ethylene facility are scheduled to complete turnarounds. The new Indorama and Lotte/Westlake ethane crackers are also expected to ramp up output in the coming weeks.

Propane prices fell at both hubs this week as a result of strong stock builds with the Mont Belvieu price moving down 10% the week of May 29 compared to the previous week. The Conway price was down 6% over the same time period.

The theoretical NGL bbl was down at both hubs with the Conway price down 8% to $18.05/bbl while the Mont Belvieu price decreased 9% to $20.26/bbl. The overall frac spread margin for the NGL bbl was down even further with a 13% decrease at Conway to $9.78/bbl while the Mont Belvieu margin fell 12% to $11.17/bbl.

The most profitable NGL to make at both hubs was pentanes-plus at 77 cents/gal at Conway and 79 cents/gal at Mont Belvieu. This was followed, in order, by isobutane at 27 cents/gal at Conway and 32 cents/gal at Mont Belvieu; butane at 24 cents/gal at both hubs; propane at 26 cents/gal at both hubs; and ethane at negative 5 cents/gal at Conway and 3 cents/gal at Mont Belvieu.

According to the U.S. Energy Information Administration (EIA), natural gas in storage for the week of May 31, 2019, was up 119 billion cubic feet to 1.987 trillion cubic feet (Tcf) from 1.867 Tcf the previous week. This is up 10% from the same time last year when it was 1.804 Tcf, but 11% off the five-year average of 2.226 Tcf.

Cooling demand should be in the normal range for this time of year as the National Weather Service’s forecast for the week anticipates normal early summer temperatures across much of the country.

Technical issues with Hart Energy’s data provider do not allow us to provide the price of ethane from Conway, Kan., for the last week of March because of a loss of pricing data for that time period. For the same reason, we cannot compare the price of the hypothetical Conway NGL barrel to the previous week. Conway ethane prices are not available for March 2019 and first-quarter 2019. We apologize for the inconvenience.

Recommended Reading

Paisie: Oil Demand to Rise 1.2 MMbbl/d in Second Half

2024-07-26 - WTI’s price is expected to stay in the low $80s/bbl.

Repsol to Implement New Share Buyback Program

2024-07-26 - Madrid-based Repsol plans to repurchase and redeem 20 million of its shares in the second half 2024, according to the company’s CEO Josu Jon Imaz.

Woodside to Emerge as Global LNG Powerhouse After Tellurian Deal

2024-07-24 - Woodside Energy's acquisition of Tellurian Inc., which struggled to push forward Driftwood LNG, could propel the company into a global liquefaction powerhouse and the sixth biggest public player in the world.

US Using More, Storing Less NatGas in Summer 2024—EIA

2024-07-24 - Gas storage levels remain high, thanks to record production levels in 2023 and a warmer-than-typical winter.

Texas LNG, EQT Sign a 2-mtpa LNG Tolling Agreement

2024-07-24 - EQT will supply natural gas to Texas LNG, a 4- million tonnes per annum LNG export terminal planned for the Port of Brownsville, Texas.